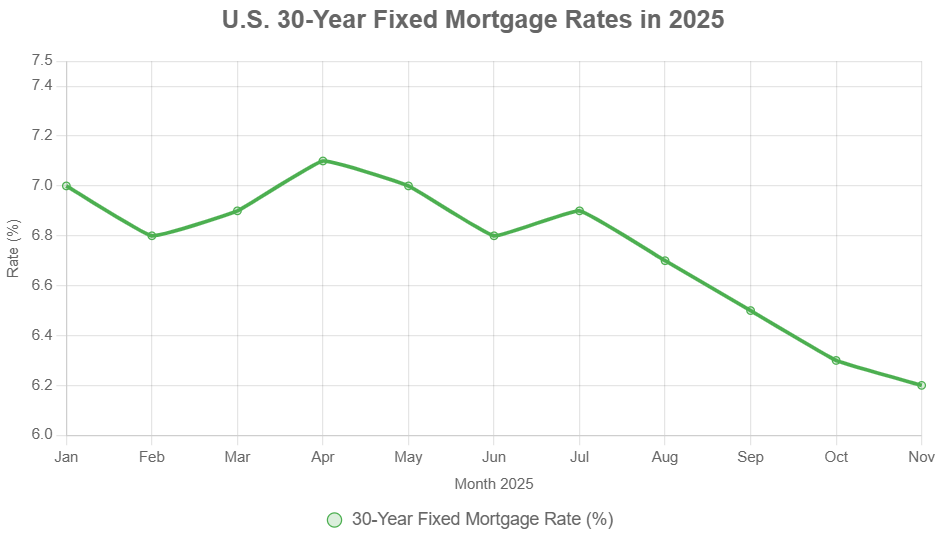

In these ever-changing economic times, owning rental properties has long been a solid way to build wealth, and right now, it's looking particularly appealing. As of late 2025, you'll notice that 30-year fixed mortgage rates have settled back down to hover around 6.2-6.3%, which is about as low as we've seen them all year, especially after they ticked above 7% earlier on.

This dip in rates is a fantastic chance for anyone thinking about becoming a landlord. It means you can lock in a more affordable loan, which leads to better cash flow from your rentals and helps you ride the wave of steady demand from people looking for homes, partly due to ongoing housing shortages and more people working remotely.

How Low Mortgage Rates Are Fueling Stronger Real Estate Returns

So, is this the perfect time to jump in? I'm here to walk you through everything—what's happening in the market, the money benefits, how to get started, where the best places to invest are, how to make sure you're getting a good return, the tax advantages, and what risks to watch out for, so you can make the best decision for yourself.

Here’s the straight-up answer: Yes, with mortgage rates near their yearly lows in late 2025, investing in rental properties presents a significantly attractive opportunity for building long-term wealth.

Why Low Mortgage Rates Are a Big Deal for Rental Property Investors

Think about it: the interest rate on your mortgage is one of the biggest costs of owning a rental property. When rates go down, the cost of borrowing money goes down too, which directly affects how much money you make from your investment. All through 2025, we've seen rates ease up a bit from their higher points, thanks to things like inflation cooling down and signals from the Federal Reserve.

Right now, the average 30-year fixed mortgage rate is sitting pretty around 6.22%, according to Freddie Mac's weekly survey. Even for investment properties, which usually have rates about 0.5% to 1% higher than for your primary home, this is still a huge improvement from the 7%+ you might have seen mid-year. This stability near the year's lows means you're borrowing money at a much cheaper rate.

This is where leverage comes into play. That’s a fancy term for using borrowed money to increase your potential return. When debt is cheaper, you can finance more of the property's cost. This means the money you put in (your down payment) can potentially generate a much bigger return. Let’s look at a quick example: Say you’re buying a $300,000 property and putting down 20% ($60,000).

If your mortgage rate drops from 7% to 6.25%, your monthly payment on that loan will be about $150 less. That extra $150 each month could be used for property upkeep, saved for emergencies, or just add to your profit. Historically, when rates have been this low, we’ve seen a real boom in rental property investments, much like what happened after 2020 when rates dipped below 3%.

To give you a visual, here’s how mortgage rates have been trending in 2025:

This downward trend really suggests that if the economy keeps improving, rates might even soften further, making 2025 an excellent year to start investing in rental properties.

Putting Your Money to Work: Key Benefits of Renting in a Low-Rate Era

Investing in rental properties is more than just collecting rent checks. It’s about building long-term wealth, creating a stream of income that can grow over time, and having an asset that often holds its value, even when other investments get shaky. Low mortgage rates make these benefits even stronger:

- Better Cash Flow: When your monthly interest payment is lower, more of the rent you collect stays in your pocket as profit. For example, on a $250,000 loan, the difference between a 7% and a 6.25% rate can save you over $1,800 a year. That’s money that directly boosts your Net Operating Income (NOI).

- Leverage and Growth: Affordable loans allow you to buy more properties sooner. This diversifies your investment (if one property has a problem, others can cover it) and lets you grow your wealth faster through rent and property appreciation.

- An Inflation Buffer: Rents typically go up over time, often keeping pace with or even beating inflation. If you have a fixed-rate mortgage, your biggest loan payment stays the same. This means your rental income grows faster than your primary expense, a concept known as positive leverage.

- Long-Term Appreciation: Real estate, especially in growing areas, tends to increase in value over time. We often see annual increases of 3-5%, which can turn your initial investment into a much larger amount of equity over a decade or more.

Compared to something like stocks or bonds, rental properties are a tangible asset. You can see them, touch them, and have more control over them. Plus, there are significant tax breaks. Now, it does take more work than just clicking a buy button on a stock, but for many of us, the rewards are well worth it. In 2025, with many people still working remotely and seeking out different living situations, vacancy rates are generally low, around 6-7% nationally, meaning your properties are likely to be occupied.

First Steps: A Simple Guide to Becoming a Landlord

Getting started in rental property investing might seem daunting, but when mortgage rates are friendly, it makes the initial hurdle feel much lower. Here’s how I usually advise people to begin:

- Get Your Finances in Order: For investment properties, lenders usually want to see around a 20-25% down payment, plus you should have enough saved to cover 3-6 months of expenses (like mortgage, taxes, insurance) for each property. A credit score of 700 or higher will help you get the best rates, often closer to 6.75% for non-owner-occupied loans.

- Decide on the Type of Property: If you’re new to this, a single-family home is often the easiest to manage. If you want to maximize your income on each dollar invested, look at multifamily properties like duplexes or triplexes.

- Line Up Your Financing: Don't just go with the first lender you talk to. Shop around for banks or mortgage brokers that specialize in investment property loans. While FHA loans can be a good option for owner-occupied properties with lower down payments, they usually have limits on units and aren't ideal for pure investment. Conventional loans offer more flexibility.

- Do Your Homework: Before buying, hire a professional inspector to check for any hidden problems. Use online tools like Zillow or Redfin to see what similar homes have sold for, and use sites like Rentometer to get a good idea of what you can realistically charge for rent in the area.

- Figure Out Management: You can manage the property yourself, which saves money but takes time. Or, you can hire a property management company. They typically charge 8-10% of the monthly rent but handle everything from finding tenants to dealing with repairs.

My advice? Start small. Maybe it's a modest home in a stable neighborhood for around $200,000. That allows you to learn the ropes without betting the farm.

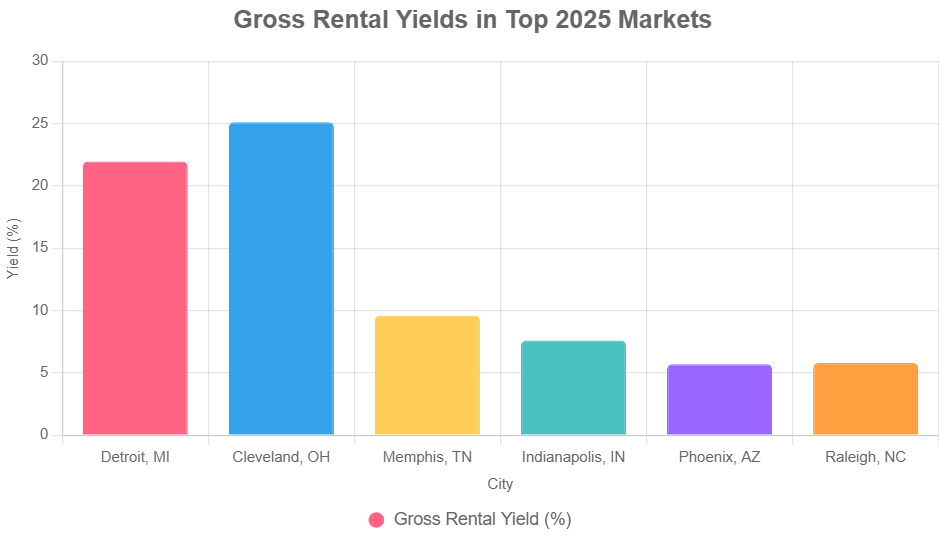

Prime Locations: Where to Invest for the Best Returns in 2025

Location, location, location – it’s the oldest saying in real estate for a reason. But where should you look? Right now, cities in the Sun Belt are really popular because lots of people are moving there for jobs and a lower cost of living. On the flip side, many cities in the Midwest offer fantastic rental yields because property prices are lower, but demand is steady. I'd suggest being a bit cautious about areas that have seen a lot of new construction, as those markets can get crowded. Instead, focus on places with balanced growth.

Here's a look at some top U.S. markets that are currently showing strong potential for rental properties in 2025, considering things like how much rent you can earn compared to the property price (gross rental yield), potential for the property's value to go up (appreciation), and how long it typically takes to find a tenant (vacancy rate):

| City/State | Avg. Home Price | Avg. Monthly Rent | Gross Yield (%) | Annual Appreciation (%) | Vacancy Rate (%) | Key Driver |

|---|---|---|---|---|---|---|

| Detroit, MI | $71,500 | $1,308 | 21.95 | 4.5 | 5.2 | Industrial revival, low costs |

| Cleveland, OH | $85,000 | $1,200 | 25.1 | 3.8 | 6.0 | Affordable Midwest entry |

| Memphis, TN | $150,000 | $1,200 | 9.6 | 5.2 | 4.8 | Logistics boom, cash flow |

| Indianapolis, IN | $220,000 | $1,400 | 7.6 | 4.0 | 5.5 | Hybrid growth, job market |

| Phoenix, AZ | $380,000 | $1,800 | 5.7 | 6.1 | 6.2 | Sunbelt migration |

| Raleigh, NC | $350,000 | $1,700 | 5.8 | 5.5 | 4.9 | Tech hub expansion |

Data from various market analyses; gross yield calculated as (annual rent / home price) x 100.

To help you see how these cities stack up on rental income potential

If you're after strong monthly cash flow, cities like Detroit and Cleveland are looking very good. If you're more focused on the property value increasing over time, places like Phoenix and Raleigh might be a better fit.

Doing the Math: How to Figure Out Your Rental Property ROI

Before you hand over any money, it’s crucial to understand your potential Return on Investment (ROI). This tells you how profitable your investment is. Here are the key numbers I always look at:

- Cash-on-Cash Return: This is probably the most important for rental properties. It’s your annual pre-tax cash flow divided by the total cash you invested (down payment, closing costs, initial repairs).

- Formula: (Annual Pre-Tax Cash Flow / Total Cash Invested) x 100.

- Example: If you made $15,000 in profit and put down $100,000 total, your cash-on-cash return is 15%.

- Capitalization Rate (Cap Rate): This helps you compare different properties, regardless of how you finance them. It’s your Net Operating Income (NOI – income after operating expenses but before mortgage payments) divided by the property’s value.

- Formula: (Net Operating Income / Property Value) x 100.

- Example: On a $200,000 property with an NOI of $12,000, the cap rate is 6%.

- Overall ROI: This considers both the cash flow you received and any profit when you sell the property.

- Formula: (Total Profit from Property – Initial Investment) / Initial Investment x 100.

Let’s crunch some numbers for a hypothetical $250,000 duplex in Indianapolis.

- Assume a 20% down payment ($50,000) plus $5,000 in closing costs, for a total cash invested of $55,000.

- Let's say you rent it for $2,000 per month, but after accounting for vacancies, maintenance, property taxes, and insurance, your actual rent collected after expenses (but before mortgage) is closer to $1,400/month, assuming mortgage payments with a 6.5% rate.

- This gives you an annual cash flow of $1,400 x 12 = $16,800.

- If the property appreciates by 4% in the first year, that’s an additional $10,000 in value.

- So, in year one, you've received $16,800 in cash flow and gained $10,000 in equity. Your total return relative to your $55,000 investment is quite high. This calculation shows the power of well-chosen investments.

There are great online calculators, like those on BiggerPockets, that can help you figure this out more precisely. Generally, I look for a cash-on-cash return of at least 8-12% on a rental property, especially in today's market. Those lower mortgage rates really help boost this number by reducing your debt service.

Tax Sweeteners: How Landlords Save Money on Taxes

One of the biggest draws of owning rental properties is the tax advantages. The U.S. tax code is pretty friendly to landlords. Here are some of the best deductions you can take:

- Mortgage Interest Deduction: You can usually deduct the full amount of interest you pay on your investment property's mortgage. This is often your largest deduction.

- Depreciation: This is a powerful, non-cash deduction. The IRS allows you to deduct a portion of the property's value (excluding land) over its useful life. For residential properties, this is typically 3.636% per year for 27.5 years. It reduces your taxable income without you having to spend more money.

- Operating Expenses: Pretty much every cost associated with running your rental property is deductible. Think repairs, maintenance, property insurance, property taxes, property management fees, travel to the property, and even supplies.

- 1031 Exchanges: This is a strategic way to grow your portfolio. If you sell an investment property, you can defer paying capital gains taxes by reinvesting the profit into a “like-kind” property.

- No Social Security/Medicare Taxes: Unlike regular wages where you pay these payroll taxes, rental income is generally exempt from them. This can save you a significant amount.

Seriously, talking to a Certified Public Accountant (CPA) who specializes in real estate is one of the smartest moves you can make. These deductions can often lower your effective tax rate by 20-30%.

Watching Out for Pitfalls: Risks and How to Protect Yourself

Like any investment, owning rental properties isn't without its risks. It’s important to be aware of potential problems and have a plan to deal with them.

- Vacancy and Tenant Problems: The biggest risk is having a property sit empty for too long, meaning no income but still having to pay bills. Another issue is tenants who don't pay rent or damage the property. To guard against this, be very thorough in screening tenants – check credit, background, and references – and price your rent competitively, perhaps 5-10% below market to attract good renters quickly.

- Rising Expenses: While rents tend to go up, so do costs. Maintenance and repair costs can creep up (a general rule is to budget 1-2% of the property value annually for upkeep). Property taxes and insurance can also increase, sometimes by 10-15% in certain areas. Always budget conservatively; I often advise clients to expect expenses to be around 50% of their gross rental income.

- Market Changes: Economic downturns or sudden interest rate hikes (though unlikely right now) could slow down property appreciation or even lead to value decreases. New local regulations, like rent control laws, can also impact your profitability.

- Liquidity Issues: Real estate isn't like stocks; you can't sell it instantly. If you need cash fast, especially during a down market, you might have to sell at a loss. This is why diversification and having cash reserves are so important.

My best advice for weathering any storm? Diversify your investments. Don't put all your eggs in one basket. If possible, aim to own 3-5 properties in different areas or even different types of property. Make sure you have adequate insurance for everything, and always, always maintain a healthy cash reserve – having 6 months of operating expenses set aside is a good target. Even with these risks, the strong demand for rentals, with rents increasing 3-4% year-over-year in many areas, still makes it a favorable market.

The Takeaway: Timing is Everything, But Be Smart About It

Right now, with mortgage rates sitting at their 2025 lows, buying rental properties offers a really compelling mix of generating income, growing your wealth over time, and having a solid, tangible asset. It can be a much more stable option than riding the rollercoaster of the stock market.

The key to success, however, always comes down to doing your research, picking the right location, and being smart and careful with your money. Whether you're drawn to the high yields in places like Detroit or the growth potential in Raleigh, make sure you educate yourself and have a solid plan in place before you make a move. Real estate has always been an investment that rewards those who are prepared, and in this current market window, the prepared investor has a fantastic opportunity to really thrive.

As Mortgage Rates Drop, Investors Are Locking in Long-Term Gains

With rates near their lowest point in a year, investors are seizing the moment to finance rental properties that deliver strong monthly cash flow and long-term appreciation.

Norada Real Estate helps you capitalize on this window with fully managed turnkey rentals in stable, high-demand markets—so you can build wealth while borrowing costs stay favorable.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Recommended Read:

- Is Turnkey Real Estate Profitable in a High-Interest Rate Environment?

- Why Turnkey Real Estate Still Beats Today's High Mortgage Rate Climate

- Best Places to Invest in Single-Family Rental Properties in 2025

- Why Real Estate Can Thrive During Tariffs Led Economic Uncertainty

- Rise of AI-Powered Hyperlocal Real Estate Marketing in 2025

- Real Estate Forecast Next 5 Years: Top 5 Predictions for Future

- 5 Hottest Real Estate Markets for Buyers & Investors in 2025

- Will Real Estate Rebound in 2025: Top Predictions by Experts

- Recession in Real Estate: Smart Ways to Profit in a Down Market

- Will There Be a Real Estate Recession in 2025: A Forecast

- Will the Housing Market Crash Due to Looming Recession in 2025?

- 4 States Facing the Major Housing Market Crash or Correction

- New Tariffs Could Trigger Housing Market Slowdown in 2025

- Real Estate Forecast Next 10 Years: Will Prices Skyrocket?