If you're dreaming of owning a home, or perhaps looking to refinance your current one, you'll want to pay attention to this: the 30-year fixed mortgage rate has dipped to a promising 6.03%. This isn't just a number; it's a signal that could make the idea of homeownership, or securing a better deal on your existing mortgage, much more achievable right now.

30-Year Fixed Mortgage Rate Drops to 6.03% Making it a Good Time for Buyers

As of December 21, 2025, according to Zillow's latest data, mortgage rates are not making huge jumps up or down, which actually creates a pretty stable environment for buyers and those looking to refinance. This general stability, especially with the key 30-year fixed rate settling at 6.03%, means that many folks who were on the fence might find this a really opportune time to act.

For months, we’ve been watching these rates. They’ve been influenced by a lot of things going on in the wider economy – like how the 10-year Treasury yield is doing, what people think inflation will do, and how strong our economy is overall. Even though the Federal Reserve recently made a move to cut its short-term rate, its message about a possible pause created some mixed signals for the mortgage market. But one thing is clear: rates are holding steady enough to be attractive.

Why the 6.03% 30-Year Fixed Mortgage Rate Matters for You

Think about it. When mortgage rates are higher, every dollar you borrow costs you more in interest over the life of your loan. A lower rate, like this 6.03% for a 30-year fixed mortgage, directly translates to more affordable monthly payments. This affordability can be the difference between being able to buy the home you want, or needing to settle for something less, or even putting off your buying plans altogether.

This current rate is a noticeable drop from what we saw in previous years. This improvement has already led to a 10% increase in purchase applications, as reported by Zillow. People are responding to this more favorable environment.

On the flip side, this lower rate environment has also created a bit of a housing market puzzle. Many homeowners who locked in really low rates (think under 4%) are understandably hesitant to sell. Why would they trade a super cheap mortgage for a new one at a higher rate? This reluctance is contributing to a shortage of homes for sale, which, in turn, is keeping home prices higher than some might expect. It’s a bit of a double-edged sword for the market, but for a buyer today, the lower rate is a definite plus.

Understanding Your Mortgage Options: A Quick Look

When you're thinking about a mortgage, you'll hear about different loan terms. The two big ones are the 30-year fixed and the 15-year fixed. I've helped countless people navigate these choices, and understanding the core differences is key to making the right decision for your financial life.

Here’s a simple breakdown:

| Feature | 30-Year Fixed | 15-Year Fixed |

|---|---|---|

| Loan Term | 30 years | 15 years |

| Monthly Payment | Lower (spread out over a longer time) | Higher (shorter repayment window) |

| Interest Rate | Typically a little higher | Typically lower |

| Total Interest | Much higher over the life of the loan | Much lower over the life of the loan |

| Equity Build-Up | Slower | Faster |

| Affordability | Easier for managing monthly cash flow, more budget-friendly | Requires stronger income or strict budget discipline |

| Best For | Buyers needing lower payments, more financial flexibility | Buyers focused on long-term savings, quick debt payoff |

Why a 30-Year Fixed Might Be Your Best Bet Right Now

From my experience, the 30-year fixed mortgage remains the most popular choice for a reason. At 6.03%, it offers incredible advantages:

- Lower Monthly Payments: This is the big one. A lower monthly payment makes affording a home much more realistic, especially for first-time buyers or those who want to keep more cash on hand for other expenses or investments.

- Financial Flexibility: Having that lower payment frees you up financially. You might have more room to save for retirement, pay down other debts, invest, or handle unexpected costs.

- Accessibility: For many, the lower barrier to entry in terms of monthly cost makes homeownership attainable when higher payments just wouldn't work with their budget.

A Word on the 15-Year Fixed

Honestly, the 15-year fixed mortgage, currently at 5.42%, is a fantastic option if your financial situation allows. You'll pay significantly less in total interest over the life of the loan and build equity a lot faster. This is great if your goal is to be mortgage-free as soon as possible and you can comfortably manage the higher monthly payments. However, for a lot of people, the jump in monthly cost from a 30-year to a 15-year can be too much, even with the lower interest rate.

Navigating the Risks and Trade-Offs

It's always wise to look at both sides of the coin.

- With a 30-Year Fixed: The main drawback is that you'll end up paying more in total interest over the 30 years. Also, because you're spreading your payments out, your home equity will build up at a slower pace.

- With a 15-Year Fixed: The higher monthly payments, while good for savings long-term, can put a strain on your budget in the short term. This might limit your flexibility for other important financial goals or needs.

The Rate Environment and What Experts Are Saying

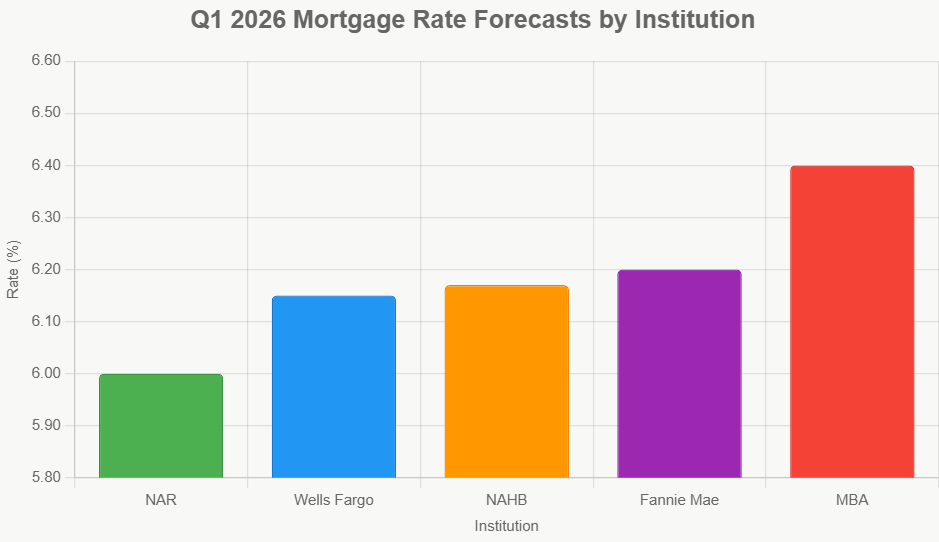

While the 30-year fixed mortgage rate at 6.03% is certainly encouraging, it's important to know that this stability isn't expected to last forever in the super-low 5% range. Most experts, including those at Zillow, anticipate that rates will likely stay above 6% for the foreseeable future. They’re predicting moderation around 6.25% to 6.50% as we move into early 2026.

This forecast suggests that while we might see small dips and rises, the extremely low rates of the past are unlikely to return soon. This makes the current moment a potentially significant window for buyers.

My Take: If You're Ready, Now Is a Great Time to Explore

As someone who's seen the housing market through various cycles, I can tell you that a 6.03% 30-year fixed mortgage rate is a compelling offer. It strikes a good balance between affordability and long-term stability.

Remember, these national averages are just that – averages. Your actual rate will depend on your credit score, the type of loan, the lender, and even your location. So, my strongest advice is always this: shop around. Talk to at least three different lenders. Compare their Good Faith Estimates. Don't just look at the advertised rate; look at the Annual Percentage Rate (APR), which includes fees, and understand all the terms.

If you've been waiting for the stars to align for homeownership, or for a more favorable refinancing option, the current mortgage rate environment is definitely worth your serious consideration. The market is offering a solid opportunity, and acting thoughtfully now could put you in a much better financial position for years to come.

VS

Two affordable rentals with solid returns: Birmingham’s steady performer vs St. Louis’s higher cap rate. Which fits YOUR investment strategy?

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Invest in Fully Managed Rentals for Smarter Wealth Building

With mortgage rates dipping to their lowest levels in months, savvy investors are seizing the opportunity to lock in financing.

By securing favorable terms now, you can also maximize immediate cash flow while positioning yourself for stronger long‑term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income while borrowing costs remain historically low.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?