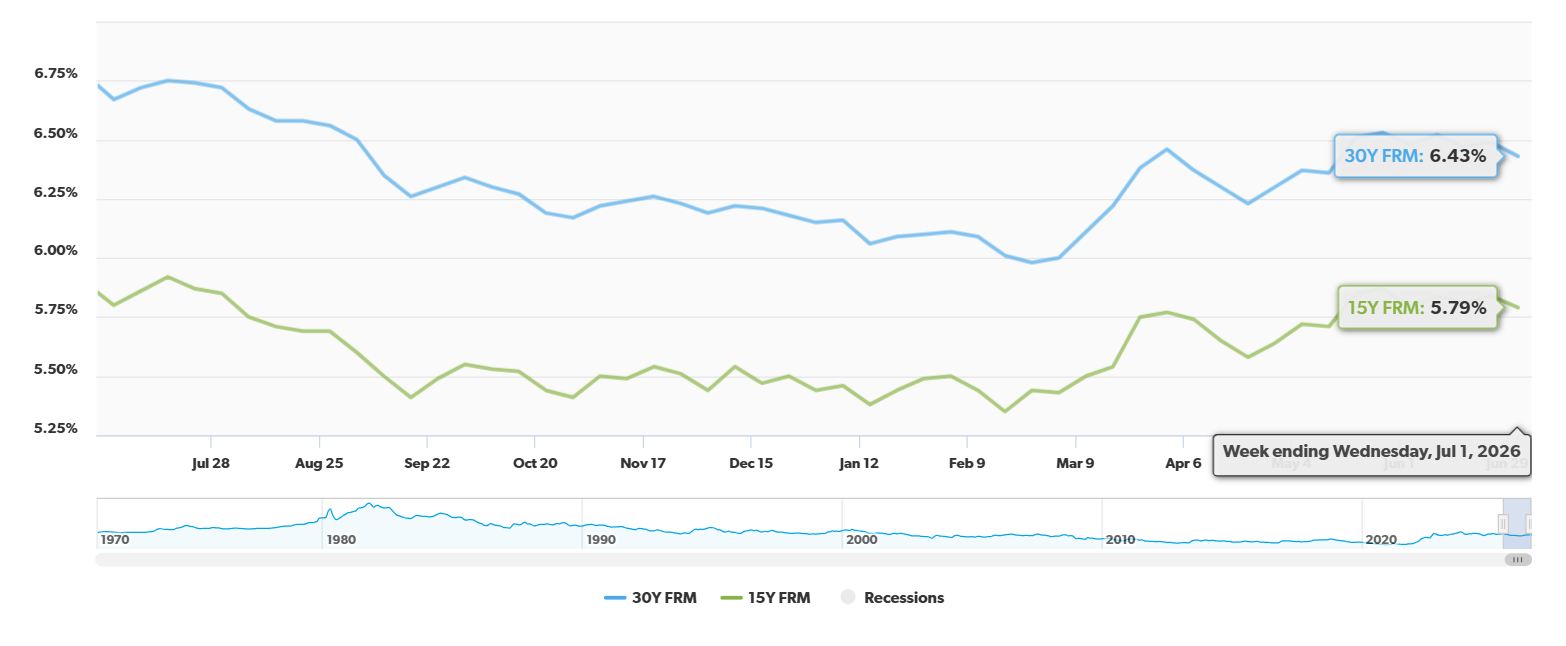

The average 30-year fixed-rate mortgage has dipped by a noticeable 24 basis points compared to this time last year, settling in at 6.43%. This is fantastic news for anyone dreaming of homeownership, as it marks the lowest borrowing cost we've seen in seven weeks. As someone who's watched the housing market for a while, I can tell you that even small drops like this can make a big difference in what people can afford. This isn't just a blip; it's a sign that things might be getting a little more manageable for folks looking to buy a home.

30-Year Fixed Mortgage Rate Drops by 24 Basis Points Year-Over-Year

What This Drop Really Means for You

Let's break down what this 24 basis point drop year-over-year actually means. Think of it this way: a basis point is just one-hundredth of a percent. So, a 24 basis point drop means borrowing is about 0.24% cheaper than it was a year ago. While that might not sound huge, when you're talking about hundreds of thousands of dollars over 30 years, it adds up!

This decrease brings the average rate down from 6.67% a year ago to the current 6.43%. It's a welcome change, especially considering how much home prices have been. Freddie Mac, a big name in the mortgage world, tracks these rates closely through their Primary Mortgage Market Survey, and their latest numbers confirm this trend.

A Look at the Weekly and Monthly Picture

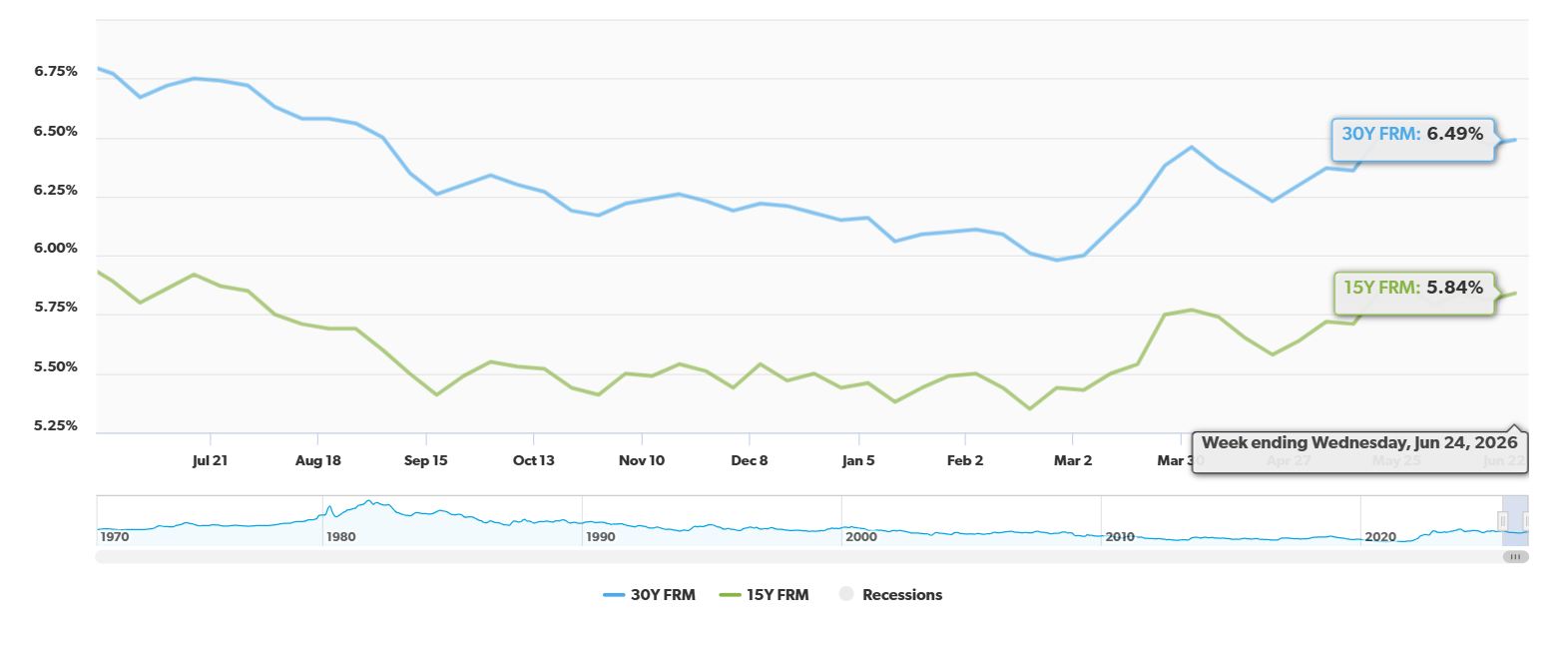

It's not just about the year-over-year change. Looking at the week-to-week movement is also encouraging. The average rate for a 30-year fixed mortgage dropped by 6 basis points (0.06%) just this past week, going from 6.49% to the current 6.43%.

And when we zoom out even further and look at the past month, we see a period of relative stability. Rates have been hovering pretty consistently in the mid-6% range since late May. This predictability is gold for buyers and sellers alike, as it allows for more confident planning. The current 6.43% is the lowest we've seen since mid-May, making it a seven-week low.

Freddie Mac's Latest Survey Data

Here's a quick snapshot from Freddie Mac's Primary Mortgage Market Survey as of July 2, 2026:

| Mortgage Type | Current Rate | 1-Week Change | 1-Year Change | Monthly Avg. | 52-Week Avg. | 52-Week Range |

|---|---|---|---|---|---|---|

| 30-Yr FRM | 6.43% | -0.06% | -0.24% | 6.48% | 6.33% | 5.98% – 6.75% |

| 15-Yr FRM | 5.79% | -0.05% | -0.01% | 5.82% | 5.61% | 5.35% – 5.92% |

(Source: Freddie Mac Primary Mortgage Market Survey)

As you can see, the 15-year fixed-rate mortgage also saw a slight dip this week, dropping by 5 basis points. While the year-over-year change for the 15-year is tiny (-0.01%), the 30-year fixed-rate mortgage is clearly leading the charge in providing more affordable long-term borrowing.

How This Impacts the Market and Your Wallet

So, what does this mean for the real estate market?

- Boost to Buyer Purchasing Power: This is the most exciting part for buyers. Lower interest rates mean your monthly mortgage payment goes down, or you can afford a bigger loan for the same monthly payment. This can open doors to more homes in your desired neighborhoods. For example, a lower rate could mean saving hundreds of dollars a month, which adds up to thousands over the life of the loan.

- Seller Pricing Adjustments: We're seeing sellers getting smarter. Instead of listing homes at sky-high prices and then having to slash them later, many are adjusting their expectations before listing. In June, home listing prices actually fell by 2.5%. This shows sellers are more in tune with what buyers can realistically afford in the current rate environment.

- Inventory Changes: While these rate drops are modest, they've been enough to slowly help things along. We're seeing more signed contracts and a bit more housing inventory compared to last year when the market felt incredibly tight. This is a good sign for a healthier balance between buyers and sellers.

From my perspective, this is a sign of a market finding its footing. It's not a massive boom, but it's a steady improvement that benefits those looking to make a move.

What's Driving These Mortgage Rate Fluctuations?

It's always helpful to understand why mortgage rates move. They don't just change randomly!

- 10-Year Treasury Yields: Think of the 10-year Treasury yield as the weather forecast for mortgage rates. Mortgage rates tend to closely follow the ups and downs of this benchmark. When Treasury yields go up, mortgage rates usually follow, and vice versa.

- Federal Reserve Influence: The Fed doesn't directly set mortgage rates, but their actions have a big ripple effect. When the Fed adjusts its short-term interest rates, it influences investor sentiment and the bond market, which in turn affects Treasury yields and, ultimately, mortgage rates.

- Economic Uncertainty: We're still in a world with plenty of economic questions. Things like lingering inflation worries and global events can make investors nervous. This uncertainty often leads to rates settling in the mid-6% range, as investors seek a balance between risk and return.

As a keen observer of these trends, I see these factors creating a dynamic environment. While rates have dropped, the underlying economic currents mean we're unlikely to see them plummet to historic lows anytime soon.

My Take on the Current Market

As someone who's navigated many housing cycles, I find this current situation quite encouraging. The 24 basis point year-over-year drop in the 30-year fixed mortgage rate is a concrete piece of good news. It signals a market that's becoming more accessible without going into overdrive. The stability in the mid-6% range over the past month provides a much-needed sense of predictability for buyers.

Sellers are adapting, which is crucial for a balanced market. They’re starting to understand that pricing strategically from the outset is a better approach than the old game of overpricing and then drastically reducing. This shift benefits everyone by making the process smoother and more realistic.

While we can't predict the future with certainty, the current trend suggests that for those who have been waiting on the sidelines, now might be a good time to seriously re-evaluate their homebuying plans. The slightly lower borrowing costs, combined with sellers who are becoming more flexible, could create a favorable window of opportunity.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?