Let's talk about the future of the U.S. economy. It's a topic that touches all of us, from the prices at the grocery store to the job market and our retirement savings. As I look ahead to 2026 and 2027, the picture is one of steady, albeit measured, growth, with inflation gradually calming down and a strong job market holding steady. It’s not a crystal-clear path, mind you, but the overall trend appears to be heading towards a “soft landing” – a way for the economy to cool down without crashing.

Economic Forecast for 2026 and 2027: GDP, Inflation, Jobs & Key Risks

The Big Picture: Growth on the Horizon

Right now, in mid-2026, the U.S. economy is showing a surprising amount of toughness. Sure, we've had some bumps, like that temporary government shutdown that slowed things down at the end of 2025. But overall, real GDP is chugging along at a healthy pace. Many smart folks – from the Federal Reserve and the Congressional Budget Office to big financial institutions like Deloitte and S&P Global Ratings – are all pointing towards continued, steady growth through 2027.

What's driving this optimism? A few key things.

- AI Power: Businesses are investing heavily in Artificial Intelligence. Think about how companies are using AI to become more efficient, develop new products, and improve services. This “AI-driven business investment” is a big tailwind.

- Government Support: Some tax and spending measures passed in 2025 are still giving the economy a boost. These acts, sometimes called the “One Big Beautiful Bill Act” or similar, are helping to put more money into people's pockets and encourage businesses to spend.

- You and Me: Consumer spending remains strong. Even with some economic pressures, people are still buying goods and services, which is the engine of our economy.

However, it's not all smooth sailing. We're still dealing with:

- Trade Hurdles: Persistent tariffs (taxes on imported goods) can make things more expensive.

- Energy Woes: Elevated energy costs, especially with tensions in the Middle East, can impact everything from gas prices to shipping costs.

- Immigration Shifts: Changes in immigration can affect the size of our workforce.

- Big Budgets: Large government deficits mean more debt, which can have long-term consequences.

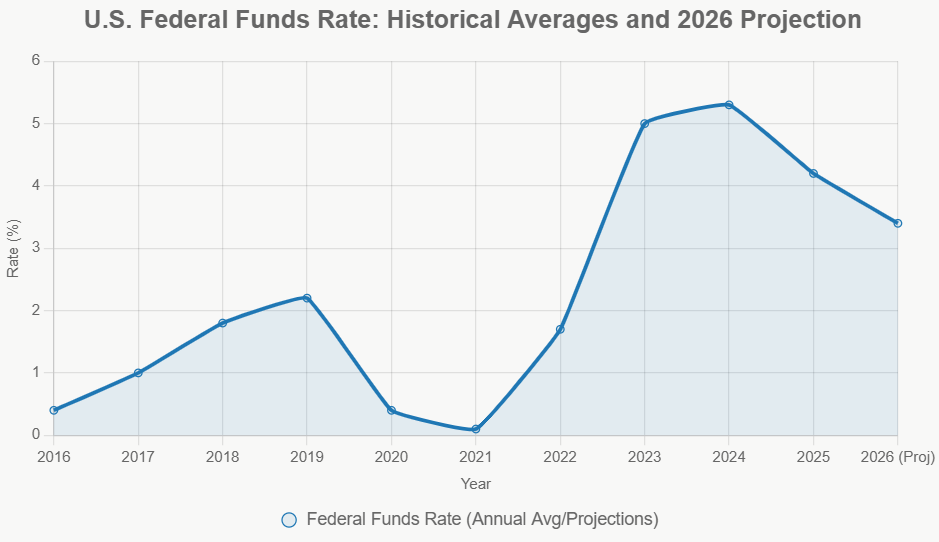

So, while most experts predict growth around 2.2% to 2.5% for 2026, and a slight moderation to 1.8% to 2.3% in 2027, it's important to remember these are averages. The journey might have its ups and downs.

Inflation: Cooling Down, But Still a Watcher

Inflation has been a hot topic, and for good reason. It’s the reason why your grocery bill seems to creep up faster each week. While recent energy price spikes, likely due to global events, have pushed inflation up a bit recently, the trend is expected to be downwards.

- The Federal Reserve is projecting PCE inflation around 2.7% in 2026, moving towards 2.2% in 2027.

- Many other forecasters see a similar pattern, with temporary bumps from energy and tariffs fading as we move through 2026 and into 2027.

The big hope is that inflation will eventually settle down close to the Fed's target of 2%. This will make our money go further and provide more predictability for everyone.

The Job Market: Steady as She Goes

One of the most reassuring signs is the strength of the labor market. The unemployment rate is expected to stay relatively low, hovering around 4.3% to 4.4% in 2026 and possibly dipping slightly to 4.2% to 4.3% in 2027.

What does this mean in plain English?

- Jobs are still being created: While the pace of job creation might slow down a bit from the frenzy of earlier years, companies are still hiring. We're looking at monthly payroll gains that are positive but moderating.

- Finding a job is still possible: For most people looking for work, the odds are still in their favor.

- Wages are growing: We're seeing wage growth that generally keeps pace with how much we produce as a country. This helps your paycheck keep up with the cost of living, without necessarily pushing inflation higher.

It seems we're entering a phase where companies are hiring and firing less, creating a more stable job market.

Monetary Policy: The Fed's Watchful Eye

The Federal Reserve plays a crucial role in managing the economy. They have tools, like interest rates, to either cool things down or stimulate growth. Given the current forecast of moderating growth and cooling inflation, the Fed is expected to be patient.

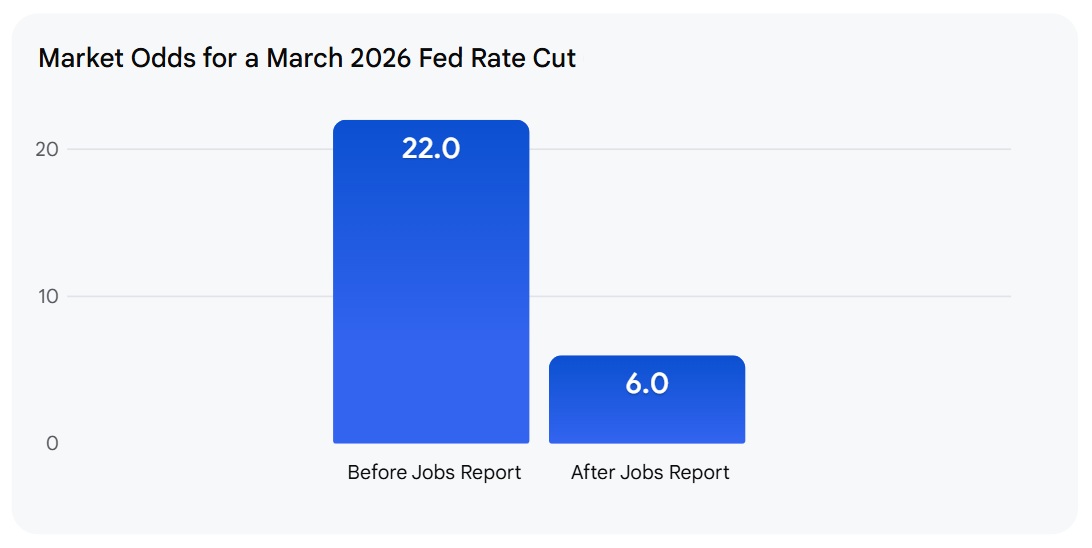

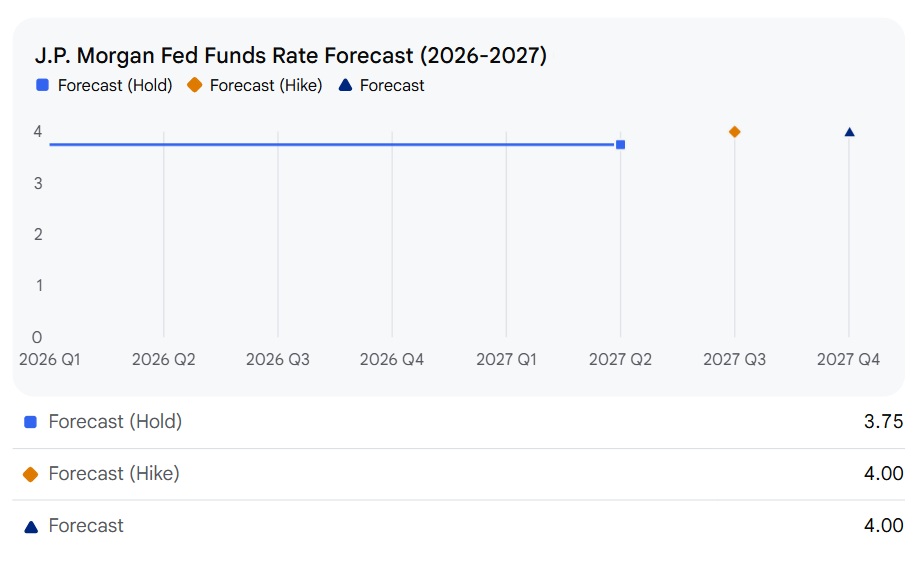

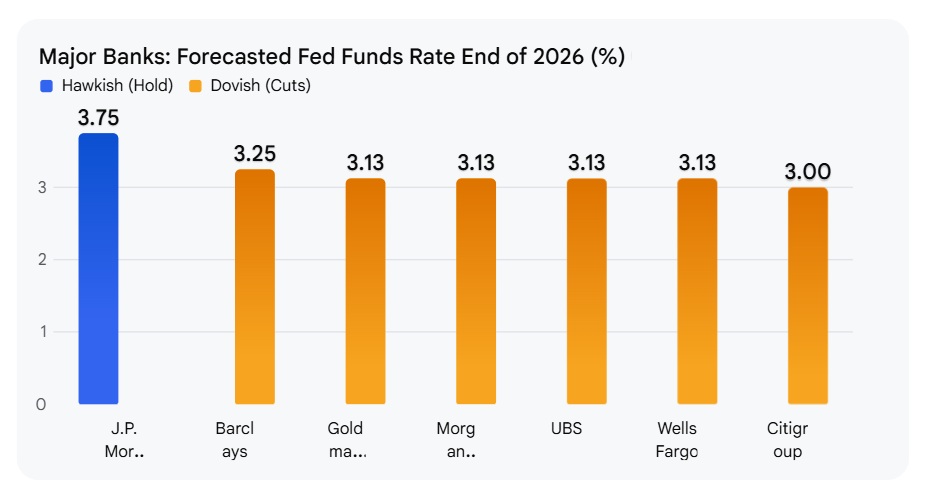

- Most forecasts suggest the federal funds rate (the benchmark interest rate) will likely stay put for much of 2026, with any potential rate cuts possibly delayed until 2027.

- This means that things like mortgage rates might stay around 6.0% to 6.3% for a while. While this can make buying a home a bit more challenging, it's a far cry from the rapid rate hikes we saw previously.

It's like the Fed is carefully watching the economic thermostat, making small adjustments rather than big, drastic moves.

Consumer Spending and Housing: Holding Steady

As I mentioned, consumer spending is a rock for the economy. We expect real consumer spending growth to slow to around 1.8% to 2.8% in 2026, which is a bit slower than in 2025, but still healthy. Those tax cuts and a strong stock market (partly fueled by AI enthusiasm) are providing a cushion, especially for those with higher incomes.

The housing market is also showing signs of stability.

- Home prices are expected to rise modestly, perhaps between 0% and 3.2% in 2026.

- Home sales might pick up slightly as more houses become available.

- With mortgage rates still a bit elevated, affordability remains a key challenge, but we're not anticipating a housing crash. It looks more like a balanced market than a boom or bust scenario.

Business Investment: The AI Effect

This is where things get really interesting. The buzz around AI isn't just talk; it's translating into real investment. Businesses, especially big tech companies (hyperscalers), are pouring money into AI-related infrastructure. This is expected to be a major driver of business investment, potentially leading to growth of 3.4% to 6% in 2026. Sectors like manufacturing and technology are poised to benefit.

Risks to Watch Out For

No economic forecast is complete without talking about what could go wrong. The risks are definitely leaning towards the downside:

- Geopolitical Tensions: Any escalation in conflicts, particularly in the Middle East, could send energy prices soaring again and reignite inflation.

- Trade Wars: Increased tariffs or new trade disputes could further disrupt supply chains and raise costs.

- AI Bust: While AI is a huge driver now, a sudden slowdown in investment or a failure to deliver on promised productivity gains could have a negative impact. Some scenarios even predict a recession if this happens.

- Debt Pile-Up: The growing national debt and rising interest payments are a long-term concern that could put pressure on future spending.

On the flip side, there are also potential upsides:

- Faster AI Progress: If AI delivers even bigger productivity boosts than expected, it could accelerate growth.

- Peaceful Resolution of Conflicts: A quick end to global tensions could lower energy prices and boost confidence.

- More Immigration: An increase in immigration could help expand the labor force.

A Look Ahead: A “Soft Landing” Seems Likely

Overall, my read on the U.S. economic forecast for 2026 and 2027 is one of cautious optimism. The economy seems to be on track for a “soft landing,” meaning it will slow down enough to bring inflation under control without tipping into a full-blown recession. However, it's crucial to remember that the path ahead is not perfectly predictable. Global events and policy decisions will play a significant role in shaping the actual outcome. For all of us, it means preparing for a world where interest rates might stay higher for longer and being ready for the occasional economic turbulence.

With GDP growth forecasts, inflation trends, and job market shifts shaping the economy, investors who act now can safeguard wealth and capture opportunities before risks intensify.

Norada Real Estate helps investors align with turnkey rental properties—delivering steady cash flow, appreciation, and long‑term ROI even in uncertain economic cycles.

Read More:

- Rising US-Venezuela Tensions Add Uncertainty to the 2026 Economic Outlook

- US-Iran War: A New Threat to America's Shaky Economy

- Bond Market Today and Outlook for 2025 by Morgan Stanley

- Goldman Sachs Significantly Raises Recession Probability by 35%

- 2008 Crash Forecaster Warns of DOGE Triggering Economic Downturn

- Stock Market Predictions 2025: Will the Bull Run Continue?

- Echoes of 1987: Is Today’s Stock Market Crash Leading to a Recession?

- Is the Bull Market Over? What History Says About the Stock Market Crash

- Wall Street Bear Predicts a Historic Stock Market Crash Like 1929

- Economist Predicts Stock Market Crash Worse Than 2008 Crisis

- Next Stock Market Crash Prediction: Is a Crash Coming Soon?

- Stock Market Crash: 30% Correction Predicted by Top Forecaster