The Federal Reserve has once again decided to keep interest rates exactly where they are, marking the third consecutive meeting without a change. This decision, landing in the target range of 3.50%–3.75%, signals a cautious approach by the central bank as it navigates a complex economic environment.

Fed Holds Rates Steady as Historic Dissent Shapes the Decision

A Dive into the Fed's Latest Decision

Let's be honest, when the Federal Reserve decides to hold steady, it’s not just a small news blip. It’s a major statement about where they see the economy heading and what they think needs to be done. This time around, the Fed’s decision to keep interest rates unchanged for the third time in a row has certainly raised eyebrows, and for good reason. It wasn't a unanimous decision, and that tells us a lot about the internal debates happening at the highest levels of our financial system.

The Unsettling Divide: Historic Dissent Among Governors

What really stood out in this latest meeting was the significant disagreement among the Fed's governors. The vote was 8–4, which, as the data points out, is the most divided the Federal Open Market Committee (FOMC) has been since way back in 1992. This isn't just a few people disagreeing; this is a substantial chunk of the key decision-makers having very different ideas about the best path forward.

On one side, we had Governor Stephen Miran, who felt strongly enough to vote for a 25-basis-point cut. His reasoning was to give a boost to a labor market that he believes is starting to soften. In his view, proactive measures are needed to prevent job losses before they really take hold. I understand his perspective; sometimes, you need to act before the problem becomes undeniable.

However, three other governors – Beth Hammack, Neel Kashkari, and Lorie Logan – while agreeing with the decision to hold rates steady for now, took issue with the “easing bias” in the Fed’s statements. This “easing bias” is essentially language that hints at future rate cuts. These governors are concerned that this kind of talk could be misinterpreted or, worse, might encourage risky behavior in markets when inflation is still a very real threat. Their concern is that signaling future cuts too strongly, when inflation is still elevated, could reignite price pressures.

Why the Hesitation? Inflation and Global Storm Clouds

So, what's driving this cautious stance and the internal debate? The committee cited two main factors: “elevated” inflation and heightened economic uncertainty.

- Inflation: We're still looking at inflation numbers that the Fed considers too high. The data suggests it's hovering around 3.3%. While this might be lower than its peak, it's still a significant distance from the Fed's 2% target. Persistently high inflation erodes purchasing power for everyday people and can make long-term planning incredibly difficult for businesses.

- Global Uncertainty: The ongoing war with Iran is casting a long shadow. This conflict has, understandably, driven up global energy prices. When oil and gas get more expensive, it impacts everything from the cost of filling up your car to the price of goods being transported. This added layer of uncertainty makes it very tricky for the Fed to make confident predictions about the future economic trajectory. It's like trying to steer a ship through fog – you have to go slow and be prepared for anything.

A Leadership Shift in the Air, But Not Quite Yet

This meeting also carried a particular significance because it was widely expected to be Jerome Powell’s last as Fed Chair. His term was set to expire on May 15, 2026. However, in a surprising turn of events, Powell announced that he will remain on the Fed's Board of Governors until his separate term ends in 2028. He cited ongoing legal challenges as the reason for his continued presence. This is an interesting development, as it means his experience and guidance will remain with the Fed, even if not in the top chair.

Meanwhile, the wheels of succession were turning. Kevin Warsh, who has been tapped as Powell's anticipated successor, saw his nomination cleared by a Senate committee on the very same day as the Fed's decision. This suggests that a transition in leadership, at least to the Chair position, is still on the horizon.

My Take: A Measured Approach in Turbulent Times

From where I stand, this decision reflects a Federal Reserve that's prioritizing stability and a clear-eyed view of the risks. My own experience in following economic trends tells me that rushing into rate cuts, especially when inflation is still a specter and global events are so volatile, can be a very dangerous game.

The dissent, while notable, actually highlights the complexity of the situation. It shows that responsible policymakers are wrestling with these tough choices. Governor Miran’s concern for the labor market is valid, but the governors who voiced concerns about the “easing bias” are also right to be vigilant about inflation.

It seems the Fed is adopting a “wait and see” approach, which, in these uncertain times, is often the most prudent course of action. They need more data, a clearer picture of how the global situation is evolving, and more confidence that inflation is truly on a downward path before they start lowering interest rates. It's about making sure that when they do decide to cut rates, it's a well-timed move that supports sustainable growth, not one that inadvertently fuels more price hikes.

The fact that Powell is staying on the board is also interesting. His deep institutional knowledge could be invaluable as the Fed navigates these complex issues and as Warsh prepares to take the helm. It suggests a commitment to continuity and expertise during a sensitive period.

Ultimately, this decision underscores that the path to economic recovery and stability isn't always a straight line. It involves careful analysis, robust debate, and a willingness to adapt to changing circumstances. For now, the Fed is holding its ground, and I believe that’s a signal of their commitment to getting inflation under control and ensuring a healthy economy for the long run.

The Fed’s rate decisions can create market volatility, but turnkey rentals continue to deliver reliable cash flow and appreciation. Investors in 2026 are focusing on real estate as a hedge against uncertainty.

Norada Real Estate helps you secure turnkey properties designed for immediate income and long‑term growth—so your portfolio stays strong regardless of Fed policy shifts.

Want to Know More?

Explore these related articles for even more insights:

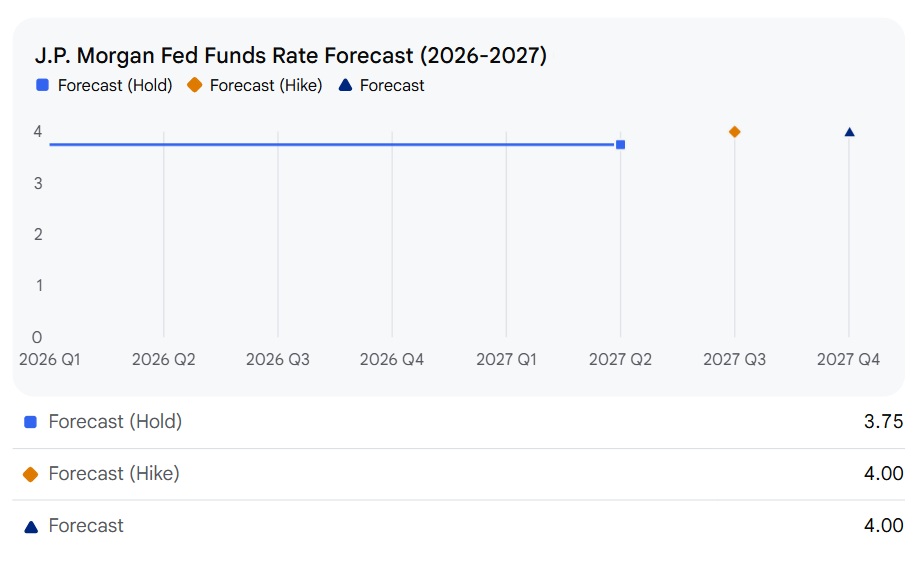

- J.P. Morgan Predicts No Fed Rate Cuts Before 2027 as Inflation Persists

- No Fed Rate Cut: Interest Rates Remain Unchanged in January 2026

- Fed Interest Rate Predictions for the Next 3 Years: 2026-2028

- The Fed After Jerome Powell: Who Could Drive Rate Cuts in 2026?

- Why Your Loan Payment Isn’t Budging Despite Recent Fed Rate Cut

- How Does the Recent Fed Rate Cut Impact Your Personal Finances

- How Will Today's Fed Rate Cut Impact Mortgage and Refinance Rates

- Fed Interest Rate Decision Today: Latest News and Predictions

- Fed Interest Rate Forecast for the Next 12 Months

- When is Fed's Next Meeting on Interest Rate Decision in 2025?

- Market Reactions: How Investors Should Prepare for Interest Rate Cut

- Impact of Interest Rate Cut on Mortgages, Car Loans, and Your Wallet