So, you're wondering what's going to happen with interest rates over the next few years? It's a big question, and I've spent a lot of time thinking about it. Based on what I'm seeing and understanding, I believe interest rates are likely to stay higher than many people have gotten used to over the past decade, probably settling in a range of 3% to 4% for a good while. We're unlikely to see those super-low rates from the 2010s again anytime soon.

Interest Rate Forecast for the Next 5 Years: 2026-2030

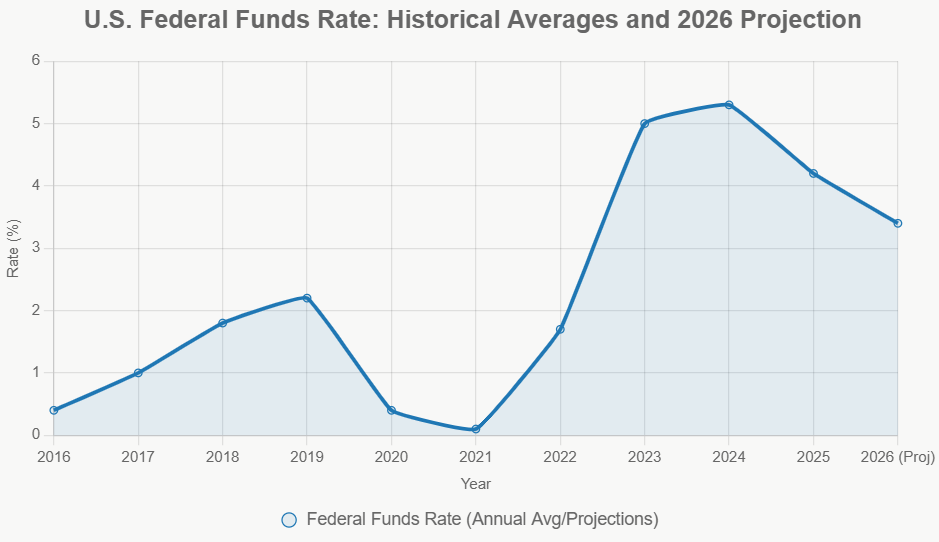

It feels like just yesterday we were talking about rates being almost zero, right? It was a pretty wild time. But things are changing, and the folks in charge of our economy, at the Federal Reserve, are also adjusting their thinking. As of mid-2026, the key interest rate they manage, called the federal funds rate, is sitting pretty between 3.50% and 3.75%. This comes after they'd been trimming rates a bit in 2025, but now there's a bit of a shift. The new leader at the Fed, Kevin Warsh, and his team seem to be leaning towards keeping rates a little higher for a bit longer.

What the Fed “Dot Plot” is Saying

Every now and then, the Federal Reserve puts out something called the “Summary of Economic Projections,” or the “dot plot.” It's basically a way for the people on the Fed's decision-making committee to show where they think interest rates will go. It's like a little map of their expectations.

Here's what the median (which means the middle number, not too high, not too low) of those projections are pointing to:

- End of 2026: Around 3.8%

- End of 2027: Around 3.6%

- End of 2028: Around 3.4%

And they think the “neutral rate” – that's the rate that neither speeds up nor slows down the economy too much – will settle around 3.1% in the long run. This is a bit of a bump up from what they were thinking earlier in 2026. It’s interesting because almost half of the Fed officials who made a prediction suggested there might even be another rate hike before the end of 2026.

What the Markets Are Thinking (and They're a Bit More Worried)

Now, the folks who trade in the financial markets, like on Wall Street, often have their own ideas, and right now, they're thinking rates might go even higher than what the Fed's “dot plot” is showing.

Based on what they're trading, it looks like they expect the rate to creep up towards 4.0% by the end of 2026 and stay around 4.1% through the middle of 2027. Then, they think it might dip a little but still hang around 4.0% from 2028 to 2030. Why are they so sure rates will stay high? They're worried that prices for things (inflation) are still a bit too high and that people are still finding jobs easily.

Here's a quick peek at what the market seems to be betting on:

- End of 2026: About 4.0%

- Mid-2027: Around 4.1%

- 2028–2030: Roughly 3.97%–4.0%

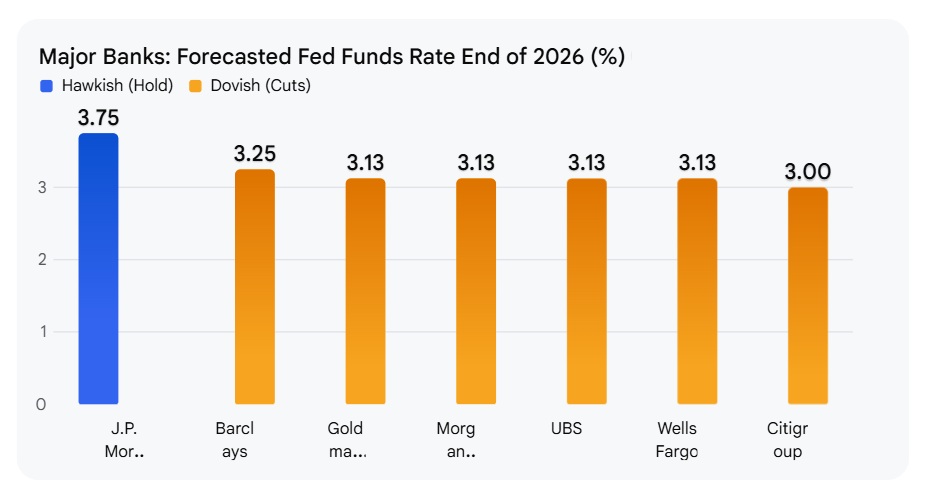

It's always good to remember that different smart people have different ideas. Some big banks, like Goldman Sachs and UBS, think the Fed will just keep rates where they are for 2026 and only start lowering them in 2027, maybe bringing them down to around 3% to 3.25%. Others, like Morningstar, think we might see cuts in both 2027 and 2028, bringing the rate down to about 2.50% to 2.75% by the end of 2028. On the other hand, Bank of America has been pretty “hawkish” (that's a term for expecting higher rates), thinking there could even be more rate hikes in 2026.

What's Pushing Interest Rates Around?

So, what's really making these interest rate predictions go up or down? A few big things are at play:

1. Inflation is Still the Boss

The biggest reason the Fed is keeping an eye on rates is inflation. That's when the prices of things go up. The Fed wants to keep inflation at about 2%. Right now, it's higher, and the Fed's own predictions show it might stay higher for longer. They thought inflation would be around 2.7% for 2026, but now they're thinking 3.6%, with the “core” inflation (which leaves out food and energy) at 3.3%.

What's making prices go up? Things like problems in other parts of the world, especially with oil prices, can really affect things. The Fed hopes inflation will calm down to 2.3% in 2027 and then hit their 2.0% target by 2028. But nobody can say for sure. If prices keep rising faster than they want, they might have to keep rates high or even raise them more.

2. The Job Market and Economy are Holding Strong

Even with higher interest rates, people are still finding jobs, and the economy is growing pretty steadily. The unemployment rate is expected to stay around 4.3% for a while. And the economy is growing at a good pace, not too hot, not too cold. This strength in the job market and economy means the Fed doesn't feel as much pressure to lower rates to help things along.

3. The “Neutral Rate” Isn't So Low Anymore

Remember how I mentioned the “neutral rate”? Well, it seems like the normal rate for the economy is higher now than it was back in the 2010s when things were super low. The Fed's idea of this neutral rate is around 3.1%. This means that to keep inflation in check, the Fed might need to keep interest rates a bit higher than “neutral” for a longer time. Think of it like this: if the natural speed limit of the economy is higher, the police (the Fed) might need to keep the speed limit signs (interest rates) a little higher too, just to make sure things don't get out of hand.

4. Government Spending and Other Stuff Matter Too

How much the government spends and borrows can also affect interest rates. Big government debts can sometimes push longer-term interest rates higher. Also, amazing new technologies like Artificial Intelligence (AI) could make the economy grow faster and maybe even push that neutral rate up more. On the flip side, if people stop spending so much or if energy prices calm down, that could give the Fed more room to lower rates.

A Year-by-Year Guess

Let's try to break down what might happen each year:

- 2026: It feels pretty likely that we'll see at least one more interest rate hike of 0.25% if inflation doesn't calm down soon. The market is definitely pricing in a good chance of this happening later in the year. However, if prices surprise us by going down faster, a hold is still possible.

- 2027: The Fed's best guess is that rates will start to tick down to around 3.6%. Many economists think the first rate cuts will happen mid-year or later, once inflation is clearly heading back towards that 2% target. But remember, the market is still thinking rates will be closer to 4%! This difference of opinion can make things a bit unpredictable.

- 2028: The Fed expects rates to continue their slow descent to about 3.4%. By this point, they think inflation will be under control, and the economy will be chugging along nicely, allowing the Fed to bring rates closer to that “neutral” level.

- 2029–2030: My gut feeling, and what the data seems to suggest, is that rates will likely settle somewhere near or a little above that 3.1% neutral rate. However, if inflation stays stubborn or if the government keeps borrowing a lot, rates might stick closer to 4%. It's highly unlikely we'll go back to those super-low rates we saw for a long time.

What Does This Mean for You?

This “higher for longer” interest rate idea means a few things for all of us:

- For your home: Mortgages will likely stay more expensive than they were in the past few years, making it harder for some people to buy a house.

- For borrowing money: Loans for cars, credit cards, and other things will also cost more.

- For saving money: On the flip side, if you have savings, you might earn more interest on your money.

- For businesses: Companies will have to pay more to borrow money for big projects. However, businesses focused on things like AI might still be investing heavily.

- For investors: Stock markets might see investors favoring companies that are doing well and aren't too deeply in debt. People investing in bonds will likely want to earn more interest for taking on the risk of lending money for longer periods.

What Could Throw a Wrench in the Works?

Things can always change, and there are risks that could push interest rates higher than expected. For example, if there's another big jump in oil prices, or if people suddenly start spending a lot more money, or if that “neutral rate” turns out to be even higher.

On the other hand, if the job market cools down a lot faster, or if prices for everything start dropping quickly, or if the government cuts back on its spending, then rates could come down faster than predicted.

My experience tells me that these predictions are just that – predictions. The Fed is really emphasizing that they'll be watching the data closely. With Chair Warsh at the helm, they've already shown they're willing to change their minds when the economic picture shifts. So, the big takeaway is to be ready for a world where interest rates are higher than they were for a while, and the super-low rate party of the last decade is likely over.

The Fed’s rate decisions can create market volatility, but turnkey rentals continue to deliver reliable cash flow and appreciation. Investors in 2026 are focusing on real estate as a hedge against uncertainty.

Norada Real Estate helps you secure turnkey properties designed for immediate income and long‑term growth—so your portfolio stays strong regardless of Fed policy shifts.

Want to Know More?

Explore these related articles for even more insights:

- J.P. Morgan Predicts No Fed Rate Cuts Before 2027 as Inflation Persists

- No Fed Rate Cut: Interest Rates Remain Unchanged in January 2026

- Fed Interest Rate Predictions for the Next 3 Years: 2026-2028

- The Fed After Jerome Powell: Who Could Drive Rate Cuts in 2026?

- Why Your Loan Payment Isn’t Budging Despite Recent Fed Rate Cut

- How Does the Recent Fed Rate Cut Impact Your Personal Finances

- How Will Today's Fed Rate Cut Impact Mortgage and Refinance Rates

- Fed Interest Rate Decision Today: Latest News and Predictions

- Fed Interest Rate Forecast for the Next 12 Months

- When is Fed's Next Meeting on Interest Rate Decision in 2025?

- Market Reactions: How Investors Should Prepare for Interest Rate Cut

- Impact of Interest Rate Cut on Mortgages, Car Loans, and Your Wallet