Let's talk about what's on a lot of our minds: where are those Federal Reserve interest rates headed in the next few years? The short answer is that after some cuts this year, they're expected to inch down slowly but surely, settling somewhere around 3% by the time 2028 rolls around. This gradual move is all about getting inflation under control while keeping folks employed.

It feels like just yesterday the Federal Reserve was hiking interest rates to tame that beastly inflation. Now, things are shifting. As of January 2026, the federal funds rate is sitting between 3.50% and 3.75%, and the Fed has already made a few cuts in late 2025. This tells me they're feeling more confident about the economy and are willing to loosen the reins a bit. But don't expect a dramatic plunge – it's going to be more of a slow, steady walk down the hill.

Fed Interest Rate Predictions for the Next 3 Years: 2026-2028

Official Projections for 2026-2028

The folks at the Federal Open Market Committee (FOMC) actually put out their best guesses, and it's called the Summary of Economic Projections. It's pretty interesting to see what they're thinking. Based on what they projected in December 2025, here’s a rough idea of where they see rates going:

| Year-End | Projected Fed Funds Rate |

|---|---|

| 2026 | Around 3.4% |

| 2027 | Around 3.1% |

| 2028 | Around 3.1% |

You can see from this table that they're not planning a big rush of rate cuts. It looks like maybe just one quarter-point cut in 2026, followed by two more in 2027. Then, by 2028, rates should be close to what they call the “neutral rate”—that's the sweet spot where the Fed’s actions aren't really pushing the economy in either direction, they're just letting it grow naturally.

What's Driving the Fed's Decisions? My Take.

It’s not magic; it's all about the economy. Several big pieces are influencing these rate predictions.

The Inflation Puzzle

The Fed's main job is to keep prices stable. They're projecting that inflation, which has been a headache, will slowly but surely get back down to their 2% target by 2027. They expect prices to cool from 2.5% at the end of 2026 down to 2.1% in 2027, and finally hit that 2% mark in 2028. They mentioned that some of the recent price bumps were due to things like tariffs, but those effects should fade. Personally, I’m watching closely to see if these inflation pressures truly disappear or if they’re more stubborn than anticipated.

The Job Market Story

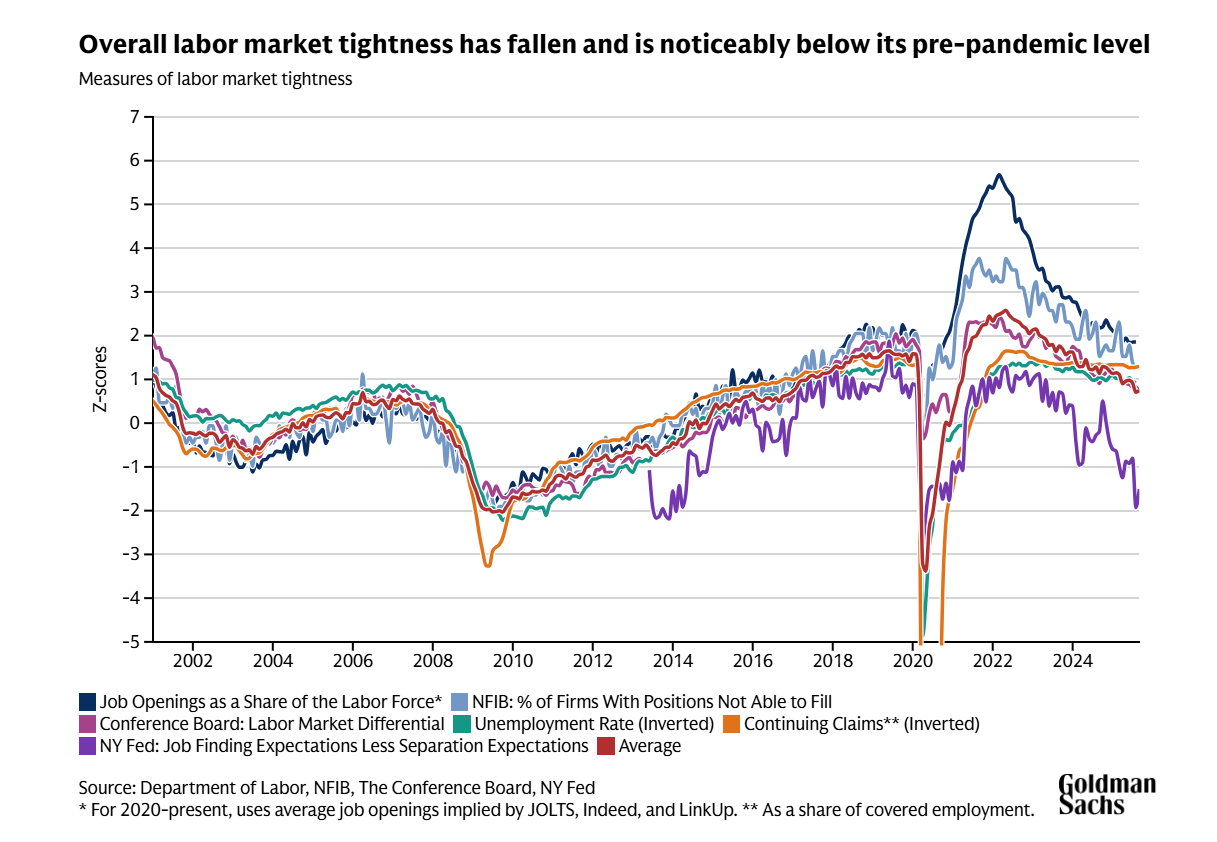

The job market is another huge piece of the puzzle. Lately, we've seen unemployment tick up a bit, and jobs aren't being created as fast as they used to. The Fed is predicting the unemployment rate will peak around 4.5% in late 2025 and then slowly drop back down to about 4.2% by 2027 and stay there. I’ve noticed too that the Fed officials themselves seem more worried about job losses right now than about inflation getting out of hand. That shift in focus is important.

How's the Economy Doing?

On a brighter note, the Fed has actually bumped up its predictions for how much the economy will grow (that’s GDP). They now think it will grow by 2.3% in 2026, which is a nice jump from what they thought back in September. Then, growth will probably slow down a bit to around 2% in the following years. This tells me they believe the economy can keep chugging along without getting too hot and causing new inflation problems. It’s a delicate dance.

Not Everyone Agrees: Divergent Views and Uncertainty

Now, here’s where it gets really interesting to me. Not all the Fed officials are singing the same tune! In that December 2025 meeting, there were a few dissenting votes, which is pretty rare. It means there’s a good amount of disagreement about what the right interest rate should be.

The “dot plot” shows individual opinions, and for 2026, these range all the way from 2.1% to 3.9%. That’s a pretty wide spread! Some smart people, like those at Morningstar, think rates could drop even lower, maybe to 2.25%-2.50% by 2027, but only if the economy really slows down. On the flip side, J.P. Morgan thinks the Fed might just keep rates where they are through 2026 and maybe even raise them a little after that. This shows there's no crystal-clear path.

What This Means for Your Mortgage and Homeownership Dreams

Interest rates have a big impact on housing, like it or not! While the Fed controls the short-term rates, what we pay for mortgages, especially fixed-rate ones, is more tied to those 10-year Treasury yields. These yields are influenced by all sorts of bigger economic stuff and even what’s happening in the world.

If the Fed cuts rates as they're predicting, it will directly affect things like those adjustable-rate mortgages that are tied to short-term rates. For fixed-rate mortgages, the relationship is a bit more indirect. Morningstar is predicting that 30-year mortgage rates could dip to around 5.00% by 2028, down from a 6.70% average in 2024. That's a significant drop!

Generally, when interest rates go down, it means there’s more money flowing around in the financial system. This can make it cheaper for people buying and developing real estate, which can boost property values. But again, how much of a difference this makes depends on how quickly and how much those rates actually decrease.

The Risks That Could Throw a Wrench in the Plan

Of course, predictions are just predictions. The Fed has tough choices to make, and there are risks. Some worry that inflation might not come down as fast as they hope, while others are concerned about too many people losing their jobs.

Here's a table to help visualize the range of possibilities for the federal funds rate in 2026, based on the Fed’s own projections:

| Fed Projection Range (2026) |

|---|

| Lower Bound: 2.9% |

| Upper Bound: 3.6% |

This wide range shows the uncertainty even within the Fed. Plus, history teaches us that forecasts aren't always spot on. Based on past data, there's a pretty good chance that the actual rates in 2026 could be around 1.4 percentage points higher or lower than what the Fed is predicting. By 2028, that range could be even wider. And let’s not forget about the unexpected – a new economic crisis, a big government spending change, or something happening internationally could totally change the game.

So, What's This All Mean for You and Your Money?

The slow and steady approach to rate cuts through 2028 means we're likely heading towards a period of pretty stable monetary policy. For you and me, this could mean a little bit of relief on things like credit card interest or adjustable-rate mortgages. But don't expect a return to those super-low rates we saw a few years back. Borrowing money will likely remain more expensive.

For investors, the Fed’s careful approach signals confidence that they can steer the economy towards a “soft landing”—meaning they can lower inflation without causing a big recession. When rates eventually settle around 3% by 2027-2028, it means the Fed will have found that neutral ground again.

Ultimately, what the Fed does will depend on how inflation, jobs, and the economy as a whole play out. They’ll be watching closely and adjusting their plans as needed, just like they always do.

Capitalize on Easing Fed Rates with Strategic Real Estate Investments

As the Federal Reserve signals a gradual path toward lower rates—projected to reach around 3.1% by 2028—now is the time to position yourself for long-term real estate gains.

Work with Norada Real Estate to lock in opportunities in high-performing markets that thrive as borrowing costs ease—boosting your cash flow and wealth-building potential.

HOT PROPERTIES LISTED NOW!

Speak with a seasoned Norada investment counselor today (No Obligation):

(800) 611-3060

Want to Know More About Interest Rates?

Explore these related articles for even more insights:

- Fed Interest Rate Predictions Over the Next 12 Months

- Fed Interest Rate Predictions for Q4 2025: October to December

- Fed Interest Rate Predictions from JP Morgan for 2025 and 2026

- Federal Reserve Cuts Interest Rate by 0.25%: Two More Cuts Expected in 2025

- Market Reactions: How Investors Should Prepare for Interest Rate Cut

- Interest Rate Predictions for the Next 10 Years: 2025-2035

- When is Fed's Next Meeting on Interest Rate Decision in 2025?

- Interest Rate Predictions for Next 2 Years: Expert Forecast

- Interest Rate Predictions for 2025 and 2026 by NAR Chief

- Impact of Interest Rate Cut on Mortgages, Car Loans, and Your Wallet

- Interest Rate Forecast for Next 5 Years: Mortgages and Savings