The Federal Reserve's big meeting kicked off, with all eyes on what they'll do with interest rates. While the official announcement isn't until today at 2 p.m. ET, the smart money says they're likely to make a cut, probably by a quarter of a percent. This could be a big moment for the economy as we head into the new year.

It feels like we’re constantly checking the economic weather, and this Fed meeting is like the barometer that tells us if things are likely to get warmer or cooler. As I look at the situation, I'm reminded of how complex these decisions are. It's not just about one number; it's about balancing a lot of different forces.

Fed Interest Rate Decision Today: Latest News and Predictions

The Two-Day Showdown: What's Happening Now?

So, what’s actually going on? The Federal Open Market Committee (FOMC), the group that actually makes these decisions, started their two-day meeting yesterday, December 9th. They’re digging into all the latest economic reports, talking through the potential impacts of different actions, and trying to figure out the best path forward. The real news, the actual interest rate decision, will be revealed tomorrow, December 10th, at precisely 2:00 p.m. Eastern Time. After that, we'll get to hear directly from Fed Chair Jerome Powell himself, which is always a crucial part of understanding their thinking.

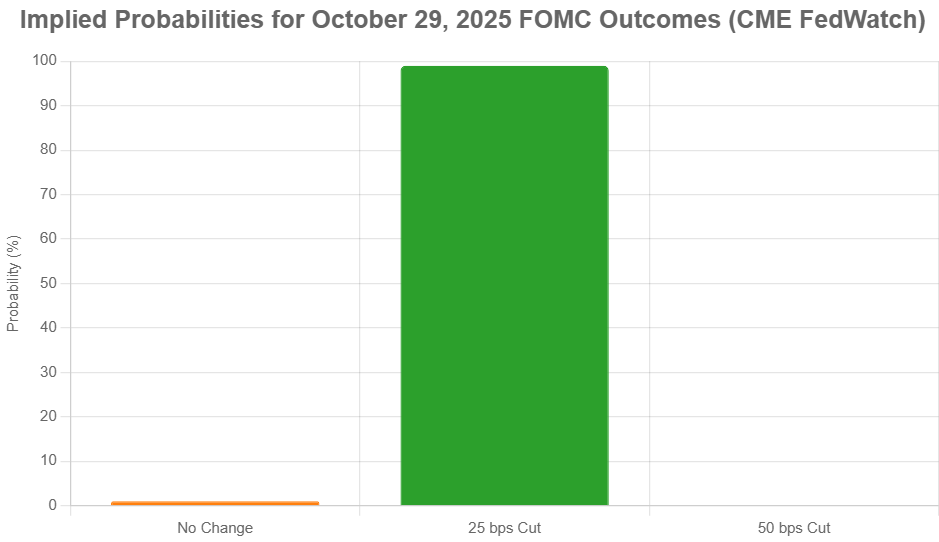

The Near-Certainty: A Rate Cut is Likely

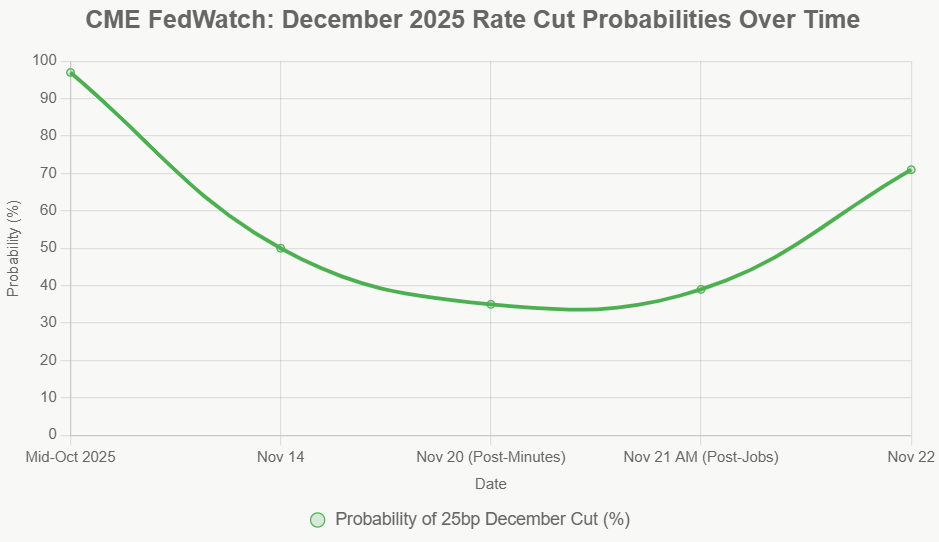

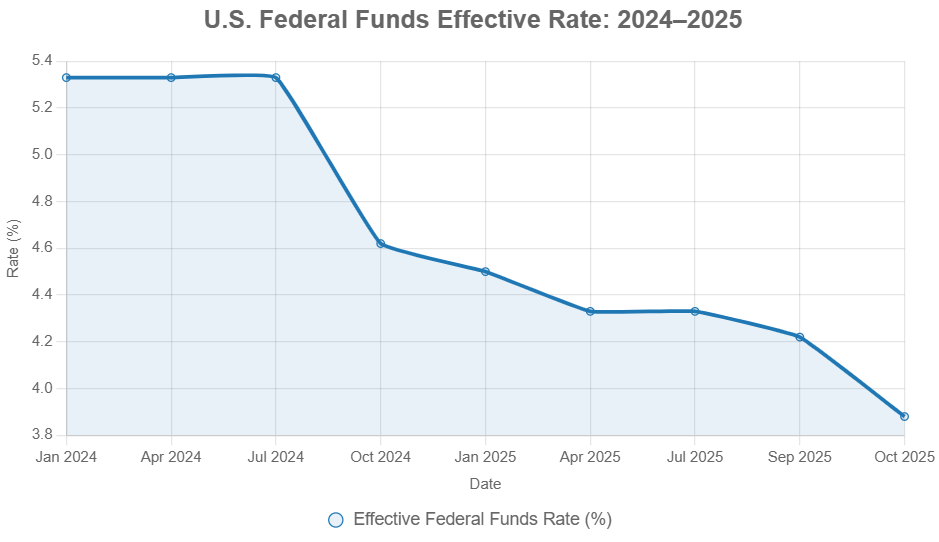

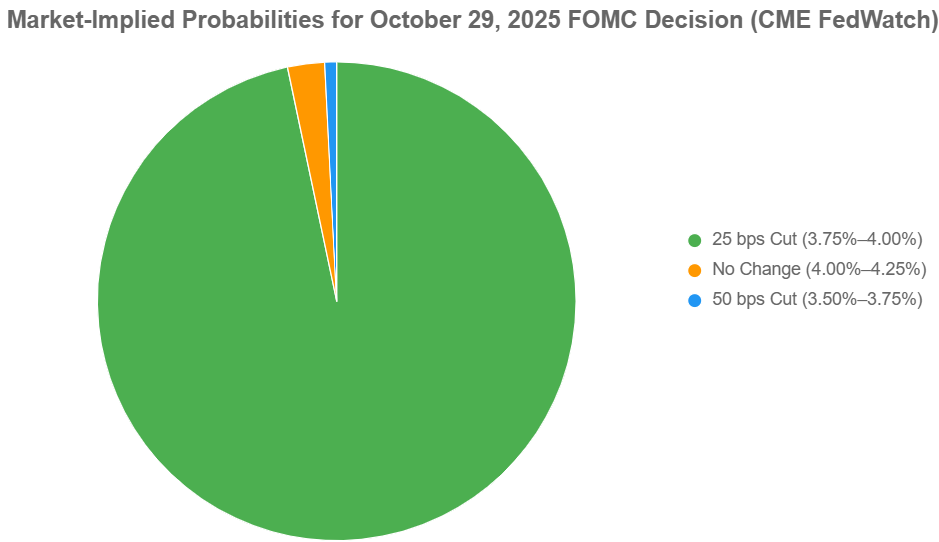

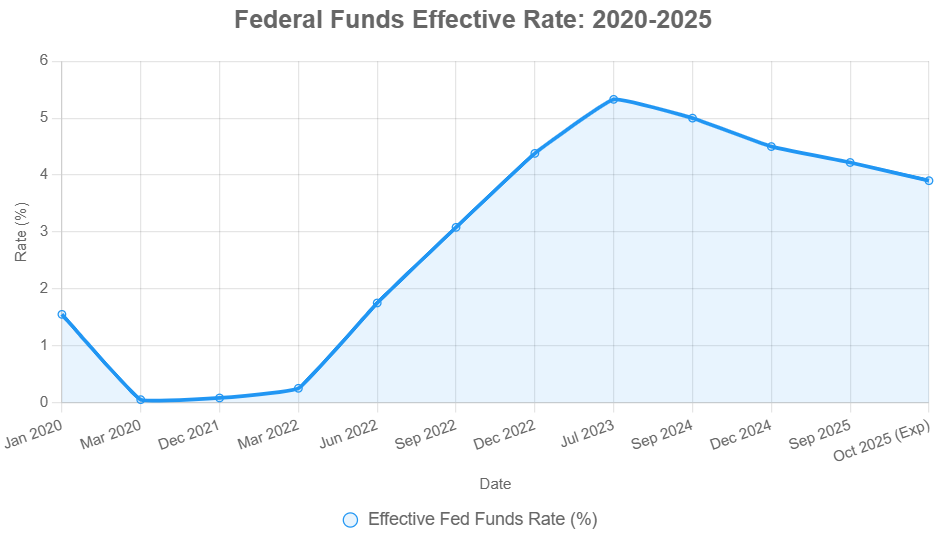

Let's cut to the chase: the financial world is pretty much convinced a rate cut is on the way. If you look at the trading floors and the financial news, you’ll see that they’re assigning a nearly 90% chance to the Fed lowering its benchmark interest rate by 25 basis points. That translates to 0.25%. If this happens, it will be the third time this year the Fed has decided to lower rates, trying to keep the economy from slowing down too much. This would bring the target range for interest rates down to between 3.5% and 3.75%.

The Unexpected Twist: A Divided Fed

Here’s where things get really interesting, and honestly, a little unusual. It looks like there’s a significant disagreement among the people making these decisions at the Fed. Usually, there’s a more unified front. This time, however, some officials are worried about inflation still being a bit too high, while others are more focused on the fact that the job market seems to be cooling down.

This division makes me think about how hard it is to get everyone on the same page, even when they're all brilliant economists. They're looking at the same economic data, but they're drawing different conclusions about what it means and what the biggest risk actually is. Because of this, I’m expecting to see some “dissenting votes” – meaning some Fed officials will disagree with the majority decision. This is something we haven’t seen much of in recent years, so it’s a big deal.

The Doves' Argument: Give the Economy a Boost!

On one side, you have the “doves.” Their main concern is keeping the economy growing and making sure people can find jobs. They believe that even with the recent rate cuts, the current interest rate is still making it a bit too hard for businesses to borrow money and expand. Their thinking goes something like this:

- The Job Market is Softening: They're pointing to signs that the number of jobs available is shrinking and the unemployment rate has ticked up a little. Recent private reports even suggest some job losses in November. To them, this is a clear signal that the economy needs a bit of help.

- Rate Cuts as Insurance: They see cutting rates as a way to protect the economy from a more serious slowdown. It's like buying insurance – you hope you don't need it, but it's good to have if things go south.

- Inflation is Temporary: They might be looking at recent small increases in inflation and thinking it's just a temporary blip, perhaps caused by things like trade policies that are expected to fade.

Some pretty influential people, like John Williams from the New York Fed and Governor Christopher Waller, have hinted that they're open to further rate adjustments. And get this, Governor Stephen Miran is even thought to favor cutting rates by a larger amount, a full 0.50%!

The Hawks' Caution: Don't Fuel Inflation!

Then you have the “hawks.” These are the folks who are really focused on keeping prices stable and making sure inflation doesn't creep back up. They worry that if the Fed cuts rates too much, it could actually make inflation worse. Their points are:

- Inflation is Still a Worry: They believe current interest rates might not be strong enough to keep inflation in check. Cutting them further could be risky.

- Demand is Still Strong: Even with all the talk of a slowdown, they see demand for things like services still being pretty healthy, which can keep some prices from falling.

- Data Uncertainty: Here's a big one – the government shutdown messed things up. Key reports about jobs and inflation for November won't be out until after this Fed meeting. This makes it really hard for the Fed to get a clear picture of what's truly happening. Because of this lack of clear, up-to-date information, they’re arguing for a more cautious approach.

We’re hearing that officials like Susan Collins of the Boston Fed are concerned about inflation sticking around, and Jeffrey Schmid of the Kansas City Fed and Alberto Musalem of the St. Louis Fed might be leaning towards keeping rates where they are.

Powell's Balancing Act: The “Hawkish Cut”

So, how does Fed Chair Jerome Powell navigate this split? It’s a tough job, and my guess is we'll see what’s called a “hawkish cut.” This means they’ll likely go ahead with the expected 0.25% rate cut – that’s what the markets are betting on. But, and this is the important part, they’ll probably signal that this doesn't mean they're going to keep cutting rates automatically. They’ll likely want to pause and see how this cut affects the economy before making any further moves. It’s about giving themselves breathing room and being ready to change course if needed.

What to Look For Tomorrow: The Official Word

When the announcement comes out tomorrow afternoon, here’s what I’ll be paying close attention to:

- The Policy Statement (2:00 p.m. ET): This is the official written explanation of the Fed’s decision. The wording here is super important. How do they describe the economy? What’s their outlook? Any subtle changes in language can tell us a lot.

- Chair Powell's Press Conference (2:30 p.m. ET): This is where Chair Powell will explain the decision in more detail and answer questions. His tone and his answers will give us crucial insights into the Fed’s thinking and their future plans.

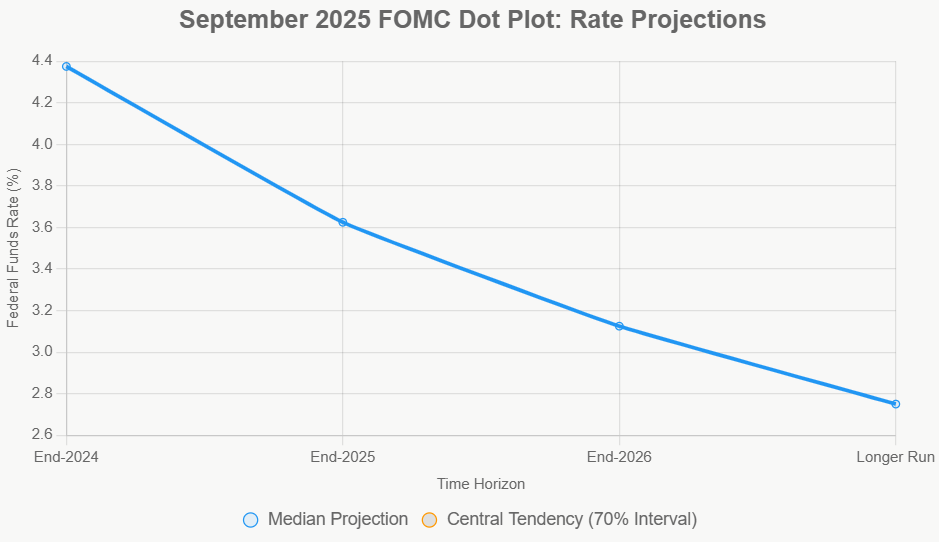

- Summary of Economic Projections (SEP): This document is a goldmine. It shows what each Fed official thinks will happen with the economy and where they see interest rates going in the coming years. This will really show us how divided the Fed is on the long-term path for interest rates in 2026 and beyond.

My Take: A Time for Careful Observation

From where I stand, this meeting is critical. The Fed is trying to steer a ship through some uncertain waters. The delayed economic data means they have to make decisions with incomplete information, which is never ideal. The split among officials highlights the real debates happening about the economy’s future.

I personally think a modest rate cut is likely the right move to support the labor market, but the communication tomorrow will be key. If they can strike a balance – cutting rates while reassuring everyone that they’re still vigilant about inflation and ready to pause if needed – that would be a big win. However, if the dissent is loud and the messaging is unclear, it could lead to more market volatility. We’ll just have to wait and see how it all unfolds.

Invest in Real Estate While Rates Are Dropping — Build Wealth

If the Federal Reserve moves forward with another rate cut in December, investors could gain a valuable window to secure more favorable financing terms and scale their portfolios ahead of renewed buyer demand.

Lower borrowing costs would boost cash flow and enhance overall returns, especially for those positioned to act quickly

Work with Norada Real Estate to find turnkey, income-generating properties in stable markets—so you can capitalize on this easing cycle and grow your wealth confidently.

NEW TURNKEY DEALS JUST ADDED!

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Want to Know More?

Explore these related articles for even more insights:

- Fed Meeting Today is Poised to Deliver the Third Interest Rate Cut of 2025

- Fed Interest Rate Predictions Signal 70% Chance of December 2025 Cut

- Fed Meeting Minutes Expose Divide: Why December Rate Cut Odds Are Fading Fast

- Fed Interest Rate Predictions for the December 2025 Policy Meeting

- Fed Signals Growing Reluctance to Interest Rate Cut in December 2025

- Fed Cuts Interest Rate Today for the Second Time in 2025

- Fed Interest Rate Forecast Q4 2025: Target Range Could Hit 3.50%–3.75%

- Fed Interest Rate Forecast for the Next 12 Months

- Interest Rate Predictions for the Next 3 Years: 2025, 2026, 2027

- When is Fed's Next Meeting on Interest Rate Decision in 2025?

- Interest Rate Predictions for the Next 10 Years: 2025-2035

- Interest Rate Predictions for 2025 by JP Morgan Strategists

- Interest Rate Predictions for Next 2 Years: Expert Forecast

- Market Reactions: How Investors Should Prepare for Interest Rate Cut

- Impact of Interest Rate Cut on Mortgages, Car Loans, and Your Wallet