It’s February 18, 2026, and if you’re a homeowner thinking about refinancing, I’ve got some potentially good news for you. The national average 30-year fixed refinance rate has dipped by a noticeable 12 basis points, bringing it down to 6.36%. This little swing might not sound like much on paper, but when you’re talking about home loans, it can add up to significant savings over the life of your mortgage.

As of today, February 18, 2026, the national average 30-year fixed refinance rate is sitting pretty at 6.36%. This is a welcome change from the 6.48% we saw just last week. This information comes straight from Zillow, a source I’ve come to trust for keeping a pulse on the housing market.

Mortgage Rates Today, February 18, 2026: 30-Year Refinance Rate Drops by 12 Basis Points

Let’s take a quick look at what the other refinance options are doing:

| Mortgage Product | Rate (February 18, 2026) | Change from Last Week |

|---|---|---|

| 30-Year Fixed Refi | 6.36% | -12 basis points |

| 15-Year Fixed Refi | 5.42% | Stable |

| 5-Year ARM Refi | 6.84% | Stable |

Why This Rate Drop Matters to You

Seeing that 30-year fixed refinance rate move down isn't just a number; it’s a signal. In my experience, these kinds of shifts, even if they seem small, can be the catalyst for a lot of homeowners to finally pull the trigger on refinancing.

- The 30-Year Stability: At 6.36%, this is still the bedrock for many homeowners looking for long-term predictability. Locking in a slightly lower rate here means a lower monthly payment for the next three decades, which is a big deal, especially if you plan to stay in your home for a while.

- The 15-Year Advantage: The 15-year fixed refinance rate is holding steady at 5.42%. This is a fantastic option if you can swing the higher monthly payments. You build equity twice as fast and save a ton on interest over the loan’s life. It’s a commitment, for sure, but the financial rewards are substantial.

- Adjustable Rates – A Word of Caution: The 5-year ARM refinance rate at 6.84% is still quite a bit higher than the fixed rates. This tells me that lenders are pricing in the risk associated with rates potentially going up in the future. While ARMs can be attractive if you plan to move or refinance again before the fixed period ends, right now, the stability of a fixed rate seems to be the more sensible choice for most.

Digging Deeper: What's Driving These Numbers?

You don’t just wake up and have mortgage rates change without a reason. A few key things are nudging these numbers around, and it’s worth understanding them to see where we might be headed.

One of the biggest pieces of news is that a significant number of homeowners are now in a prime position to refinance. Zillow’s data suggests that nearly 5 million homeowners are currently “in the money,” meaning they can likely get a better deal by refinancing than what they're paying now. This has been a jump of about 20% in eligible borrowers since the start of January, thanks to rates inching closer to that 6% mark. It's a great sign that the market is becoming more accessible to people.

What’s causing this shift? Well, a couple of major economic forces are at play. First, we’ve seen a recent dip in 10-year Treasury yields. When Treasury yields go down, it generally makes it cheaper for lenders to borrow money, and they pass those savings on in the form of lower mortgage rates. Think of it like wholesale prices for money dropping.

On top of that, there’s been a bit of wobble in the stock market. When stocks get a bit shaky, investors often move their money into safer assets, like government bonds, which can also push Treasury yields lower. It’s a classic “flight to safety” scenario.

Adding a bit more pressure downwards on mortgage rates is a federal directive. Fannie Mae and Freddie Mac, which are government-sponsored enterprises that play a big role in the mortgage market, have been directed to purchase $200 billion in mortgage-backed securities. This essentially injects more money into the mortgage market, making it easier for lenders to offer lower rates. It’s a deliberate move to keep borrowing costs down.

The Federal Reserve and Inflation: Keeping an Eye on Things

Now, let’s talk about the big boss: the Federal Reserve. They are super important because their decisions on interest rates ripple through the entire economy. The Fed held its interest rates steady at their meeting on January 28th. This was a pause after a series of rate cuts, and they're watching inflation closely. Right now, inflation is sitting at 2.7%. They need to make sure it's heading towards their target before they start cutting rates aggressively again.

The next big meeting for the Federal Open Market Committee (FOMC) is scheduled for March 17–18, 2026. This meeting is crucial because whatever they decide there will likely set the tone for major interest rate movements for the rest of the year. We’re all watching to see if they’ll continue pausing or start another round of cuts.

Looking Ahead: 2026 Forecasts

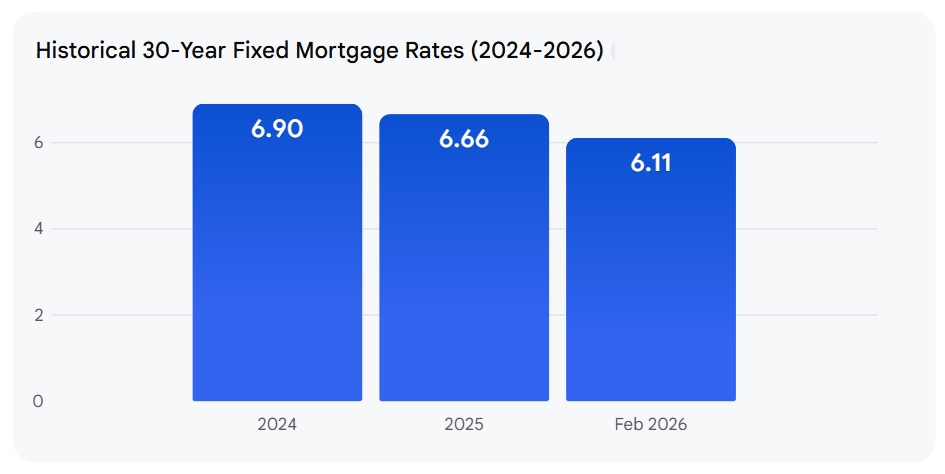

So, what does all this mean for the rest of 2026? The smart money, including folks at Fannie Mae, are predicting that mortgage rates will likely stay around the 6.0% mark for the remainder of the year. That’s pretty stable, and a good neighborhood to be in if you're looking to refinance.

And if you want to get even more specific, some big names like Morgan Stanley are forecasting that rates could even end the year at a low of 5.75%. This is optimistic, of course, and relies on the Fed continuing to manage inflation successfully.

The Economic Picture: A Balanced Act

The fact that we’re seeing mortgage rates ease back a bit, driven by lower Treasury yields and a more controlled inflation outlook, suggests a certain level of confidence in the broader economy. Lenders aren’t panicked; they’re adjusting cautiously. They’re offering these slightly better rates because the underlying conditions support it, but they’re also not doing anything that would inject unnecessary volatility into the market. It’s a delicate balance they’re trying to strike.

What This Means for You, the Homeowner

So, how do you, as a homeowner, use this information?

- Considering a Refi? Now's the Time to Check: That 12 basis point drop in the 30-year fixed rate might seem like a small number, but when you do the math on your loan amount, it can translate into some serious monthly savings. If you’ve got a larger mortgage, these savings could be hundreds of dollars a month. Don’t just assume it’s not worth it; run the numbers!

- Short-Term Savings vs. Long-Term Goals: The 15-year fixed rate holding steady means it’s still an excellent option for those who want to pay off their home sooner and save big on interest in the long run. If you can handle the higher monthly payments, this is often the smartest financial move you can make.

- ARM Logic: The fact that ARM rates are still higher than fixed rates is a clear signal. It’s telling you that taking on the uncertain future of adjustable rates comes at a premium right now. Weigh the risks very carefully if you’re even thinking about an ARM. For most people, the peace of mind from a fixed rate is worth it.

The Bottom Line on Today’s Refinance Rates

To wrap it all up, mortgage refinance rates on this February 18, 2026, are giving homeowners a bit of a breather. The headline today is that the 30-year fixed refinance rate has dropped to 6.36%. While it’s not a dramatic plunge, it’s a definite movement in your favor. This stability in the fixed-rate options, contrasted with the higher rates on ARMs, really highlights the value of locking in a predictable payment. For anyone looking to lower their monthly costs or simply gain more financial certainty, now is a prime time to explore your refinancing options and potentially lock in some valuable savings for the future.

and

Florida’s modern build with strong cash flow vs Missouri’s affordable rental with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to Our Investment Counselor (No Obligation):

(800) 611-3060

Market forecasts suggest steady demand, making turnkey real estate one of the most reliable paths to passive income and wealth creation.

Norada Real Estate helps investors capitalize on these trends with turnkey rental properties designed for appreciation and consistent cash flow—so you can grow wealth securely while others wait for clarity in the market.

Recommended Read:

- 30-Year Fixed Refinance Rate Trends – February 17, 2026

- Best Time to Refinance Your Mortgage: Expert Insights

- Should You Refinance Your Mortgage Now or Wait Until 2026?

- When You Refinance a Mortgage Do the 30 Years Start Over?

- Should You Refinance as Mortgage Rates Reach Lowest Level in Over a Year?

- Half of Recent Home Buyers Got Mortgage Rates Below 5%

- Mortgage Rates Need to Drop by 2% Before Buying Spree Begins

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years