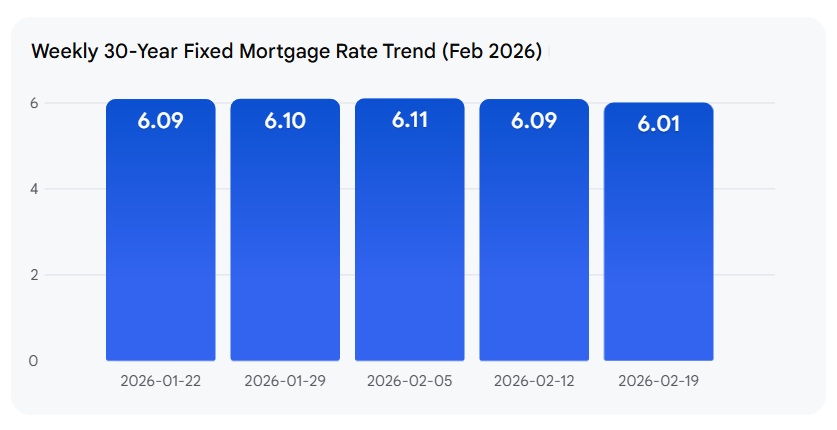

In 2026, with benchmark rates hovering between 6.5% and 7%, aiming for that coveted 5% mortgage rate can feel like an uphill challenge. However, by thinking outside the typical 30-year fixed loan box and employing a few smart strategies, securing a rate at or even below 5% is absolutely achievable. It's not about luck; it's about knowing where to look and how to negotiate.

Having spent years working with borrowers, I’ve seen how even small shifts in strategy can make a big difference in monthly payments and the total interest over the life of a loan. Here’s how you could position yourself to secure a 5% mortgage rate in 2026.”

How to Get a 5% Mortgage Rate in 2026?

The dream of a 5% mortgage rate, especially when average rates are higher, feels like finding a hidden gem. Based on my experience and current market trends, this often means stepping away from the standard 30-year fixed mortgage and exploring more creative avenues.

1. Harnessing New Construction Builder Incentives

Builders are often your biggest allies when trying to secure a lower rate, especially on new homes. They have a vested interest in selling quickly, and they have the capital to make it happen.

- Permanent Rate Buydowns: Many large homebuilders partner with mortgage companies or have their own to offer permanent rate buydowns. This is where the builder pays a portion of the interest upfront, permanently lowering your rate for the entire life of the loan. I've seen these offers frequently in the 4.99% to 5.25% range on 30-year fixed mortgages. It's a fantastic way to get a low rate without significantly altering your monthly payment structure.

- Temporary Buydowns: Another strategy is a temporary buydown, often structured as a 2-1 or 3-1. For example, a 3-1 buydown means your interest rate is reduced by 3% for the first year, then 2% for the second year, and 1% for the third year, before settling at the full contract rate. While not a permanent 5% rate, it significantly lowers your payments in those crucial early years, giving you time to refinance or build equity.

2. The Power of Shorter Loan Terms

It’s a simple principle: less risk for the lender generally means a better rate for you.

- 15-Year Fixed Mortgage: Opting for a 15-year fixed loan instead of a 30-year term can typically shave off 0.5% to 1.0% from your interest rate. This means if the average 30-year rate is 6.5%, a 15-year term might put you in the 5.5% to 6.0% range, much closer to your 5% goal. While the monthly payments will be higher due to the shorter repayment period, the overall interest savings are substantial.

3. Considering Adjustable-Rate Mortgages (ARMs)

ARMs can be a powerful tool if you plan to move or refinance before the initial fixed period ends.

- Initial Fixed Period: Products like a 5/1, 7/1, or 10/1 ARM offer a fixed interest rate for the first 5, 7, or 10 years, respectively. After that period, the rate adjusts annually based on market conditions.

- Rate Discount: These introductory ARM rates are almost always significantly lower than their 30-year fixed counterparts. This makes hitting a 5% rate much more attainable upfront. My advice here is to carefully assess your long-term plans and the potential risks of rate increases down the line.

4. Buying Down Your Rate with Discount Points

This is a more direct way to lower your rate, but it requires an upfront investment.

- Upfront Fees: You can pay discount points directly to the lender at closing. One discount point typically costs 1% of your loan amount and can lower your interest rate by approximately 0.25%.

- The Math: If you're aiming for a 5% rate and the best available rate is 5.75%, you might need to purchase about 3 discount points (3% of the loan value) to get down to 5%. It's crucial to calculate your break-even point – how long you need to stay in the home for the savings from the lower rate to offset the upfront cost of the points. If you plan to sell or refinance before this point, it might not be the best strategy.

5. Leveraging Government-Backed Programs

Certain government-backed loans are designed to make homeownership more accessible, often with more favorable rates.

- Assumable Loans: FHA and VA loans can be assumable. This means if you find a seller who has one of these loans with a rate at or below 5% (which is quite possible if they secured it a few years ago), you may be able to take over their existing mortgage. This is a fantastic way to bypass current market rates entirely. However, you'll still need to cover the seller's equity.

- Government Rate Baselines: Even without an assumable loan, FHA, VA, and USDA loans generally have lower baseline interest rates and more flexible qualification requirements compared to conventional loans.

6. Maximizing Your Financial Profile

Your financial health is a huge factor in the rate you'll be offered. Lenders see a strong financial profile as less risk.

- Credit Optimization: A FICO score of 780 or higher is generally considered excellent and will unlock the best available interest rates. If your score is lower, focus on paying down debt and ensuring on-time payments to boost it before applying.

- Bank Relationships: Sometimes, deepening your relationship with a bank where you already have significant assets can pay off. Some institutions offer preferential rates or waive fees for their premier or high-balance depositors.

- The 20% Down Payment: While not always necessary for a 5% rate, putting 20% down eliminates Private Mortgage Insurance (PMI) and signals to lenders that you are a very low-risk borrower, often qualifying you for their best pricing tiers.

Comparing Paths to a 5% Mortgage Rate

To help visualize the different approaches, here’s a quick comparison:

| Strategy | Property Type | Upfront Cash Required | Rate Type | Risk Profile | Notes |

|---|---|---|---|---|---|

| Builder Incentive | New Construction | Often $0 (paid by builder) | 30-Year Fixed | Very Low (rate locked for life) | Look for permanent buydowns; check builder's preferred lender. |

| 15-Year Fixed + Points | Existing Property | 2.5% – 3% of loan amount (for points) | 15-Year Fixed | Low (higher monthly payment) | Calculate break-even point carefully. |

| Seller Concession Buydown | Existing Property | $0 (paid by seller, negotiated) | 30-Year Fixed | Low (requires motivated seller) | Negotiate as part of the purchase agreement. |

| Temporary Buydown | Either | Varies (builder or seller can fund) | 30-Year Fixed | Low initially, increases over time | Great for first few years; ensure you can afford rate after period. |

| ARM (e.g., 7/1) | Either | Often $0 | Adjustable | Medium (rate is variable after fixed period) | Best if you plan to move or refinance before rate adjusts. |

| Assumable Loan | Existing Property | Varies (equity gap to seller) | FHA/VA (Existing) | Low (if current rate is good) | Requires finding a specific type of listing and seller. |

Remember, hitting a 5% mortgage rate isn't guaranteed and often involves trade-offs. It might mean compromising on the exact house you want, accepting a shorter loan term, or paying more upfront. However, by understanding these strategies and working closely with your real estate agent and loan officer, you can significantly increase your chances of securing that favorable interest rate in 2026.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?