Buying a home is a huge step, and one of the biggest hurdles is figuring out how to afford it. With today's market, many folks are finding that an adjustable-rate mortgage, or ARM, is becoming a seriously attractive option. Adjustable-rate mortgages are gaining popularity as buyers look for ways to lower their initial mortgage costs, and for good reason. They can offer a lower starting payment, which can make getting into a new home feel a little more within reach.

Why More Buyers Are Betting on Adjustable-Rate Mortgages in 2025?

For a while there, fixed-rate mortgages have been the go-to. You know, where your interest rate stays the same for the entire life of the loan – usually 15 or 30 years. This gives you predictable monthly payments, and that peace of mind is priceless for many. However, as interest rates fluctuate, sometimes the initial sting of a higher fixed rate can really make you pause. That's where ARMs come in, offering a different path. They typically start with a lower, fixed interest rate for a set number of years, like five, seven, or even ten. After that introductory period, the rate “adjusts” based on what's happening in the wider market.

I've seen firsthand how confusing mortgage options can be. When I was looking to buy my first place, the sheer number of choices felt overwhelming. But by talking to lenders and doing my homework, I learned that understanding the different types of mortgages is key to making a smart financial decision. ARMs, while they might seem a bit riskier because the payments can go up, can actually be a fantastic tool if you're strategic about it.

Why All the Buzz About ARMs Right Now?

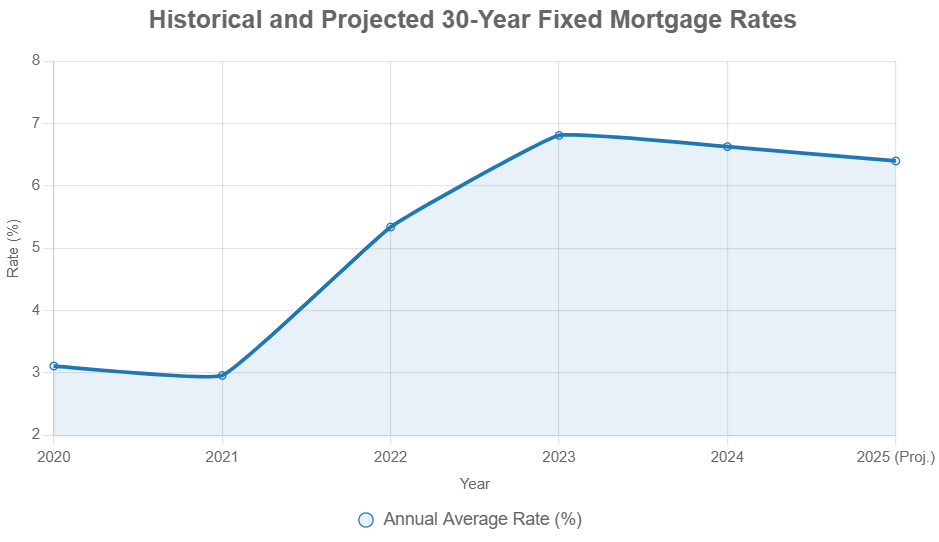

It's no secret that the Federal Reserve making moves on interest rates can shake things up. Recently, they've cut their benchmark interest rates a couple of times. Now, this doesn't mean your mortgage rate instantly drops, but it does influence broader market rates. Freddie Mac reported that the average 30-year fixed-rate mortgage dipped to about 6.17% recently, which is great news if you're looking for a fixed rate. But here's where ARMs really start to shine: loans like ARMs might see a more direct impact from these Fed adjustments.

The experts at the Mortgage Bankers Association (MBA) have noticed this shift. In September, ARMs made up about 10% of all mortgage applications, which was the highest it's been in nearly two years. That's a pretty significant jump and tells us a lot of people are seriously considering them.

The Savings: A Closer Look at ARMs

Let's talk numbers, because that's what really matters when you're trying to buy a house. Typically, an ARM offers a lower interest rate during its initial fixed period compared to a 30-year fixed mortgage. For example, a 5/1 ARM (meaning the rate is fixed for the first five years and then adjusts annually) averaged around 5.66% in September. That's almost a full percentage point lower than the average 30-year fixed rate at the time.

What does that mean in real dollars? If we're talking about a $400,000 loan, that difference could save you about $200 per month during those first five years. Multiply that by 60 months (five years), and you're looking at around $12,000 in savings, just on monthly payments. That's real money that can help with moving costs, furniture, or just gives you a bit more breathing room in your budget.

Understanding the “Adjustable” Part: What to Watch Out For

Now, as much as I love a good money-saving opportunity, it's crucial to be realistic. The “adjustable” part of an ARM is where the potential risk lies. After that initial low-rate period ends, your interest rate will change based on market conditions. This means your monthly payment could go up, or, if the market is favorable, it could even go down.

Joel Kan, the deputy chief economist at the MBA, wisely pointed out that while ARMs offer opportunities, you need to understand the potential risks. If interest rates climb significantly after your fixed period, your mortgage payment could become much harder to manage. This is where my own experience kicks in: I always advise talking to a lender and really getting a clear picture of what the worst-case scenario looks like for your payment. Don't just dive in without fully understanding it.

Who Benefits Most from an ARM?

ARMs aren't for everyone, but they can be a smart move for certain buyers:

- First-time homebuyers: The lower initial payment can make getting into your first home more achievable.

- People who plan to sell or refinance: If you anticipate selling your home or refinancing your mortgage before the initial fixed period ends, you can take advantage of the lower rate without facing the adjustment.

- Buyers who can afford higher payments: If your budget can comfortably accommodate a higher payment if rates rise, an ARM can be a calculated risk for initial savings.

- Those who expect interest rates to fall: If you believe that overall interest rates will decline in the future, you might benefit from the rate adjusting downward after the initial period.

Recommended Read:

Fixed vs. Adjustable Rate Mortgage in 2025: Which is Best for You

Fixed-Rate Mortgages Still Offer Value

Even with the rise in ARM popularity, 30-year fixed-rate mortgages are still a great option for many. As I mentioned, rates have been dropping. Freddie Mac's data shows that the 30-year fixed-rate mortgage averaged 6.17% recently. For some, the security of a predictable payment for decades outweighs the potential for short-term savings with an ARM.

The National Association of REALTORS® (NAR) actually reported a 4.1% annual increase in existing-home sales for September, which signals renewed buyer activity. This shows that even with rates hovering in the mid-6% range, people are still finding ways to make homeownership happen. A LendingTree analysis found that buyers already saved an average of $40,000 over the life of a 30-year loan just from rate drops earlier in the year.

My Take on the Current Mortgage Market

As someone who's navigated the home-buying process and kept a close eye on the market, I think the current environment presents some really interesting choices. The fact that both fixed-rate mortgages and ARMs are becoming more attractive shows a market that's trying to balance affordability with stability.

My advice? Don't pick a mortgage type based on what everyone else is doing or what sounds cheapest at first glance. Instead, take a deep breath, crunch your numbers, and have honest conversations with mortgage professionals. Understand the terms, the potential upsides, and the possible downsides of each option.

For adjustable-rate mortgages, the key is to do your due diligence on the initial fixed period, the rate adjustment formula, and what your potential maximum payment could be. For fixed rates, it's about finding the best rate and term that fits your long-term financial plan. Both have their place, and sometimes the “best” mortgage is the one that best fits your unique situation and goals.

Here's a quick peek at how mortgage rates have been looking:

| Mortgage Type | Average Rate (Week Ending Oct. 30) | Year Ago Rate |

|---|---|---|

| 30-Year Fixed-Rate | 6.17% | 6.72% |

| 15-Year Fixed-Rate | 5.41% | 5.99% |

(Data from Freddie Mac)

Ultimately, the goal is to find a home you love and a mortgage that you can comfortably manage. ARMs are definitely a tool worth exploring in today's market to potentially lower those upfront costs.

Earn Passive Income Through Smart Real Estate Investments

With fluctuating mortgage rates, savvy investors are exploring flexible financing options to maximize returns.

Norada offers a curated selection of ready-to-rent properties in top markets, helping you capitalize on current mortgage trends and build long-term wealth.

HOT NEW LISTINGS JUST ADDED!

Connect with an investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Expect High Mortgage Rates Until 2026: Fannie Mae's 2-Year Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?