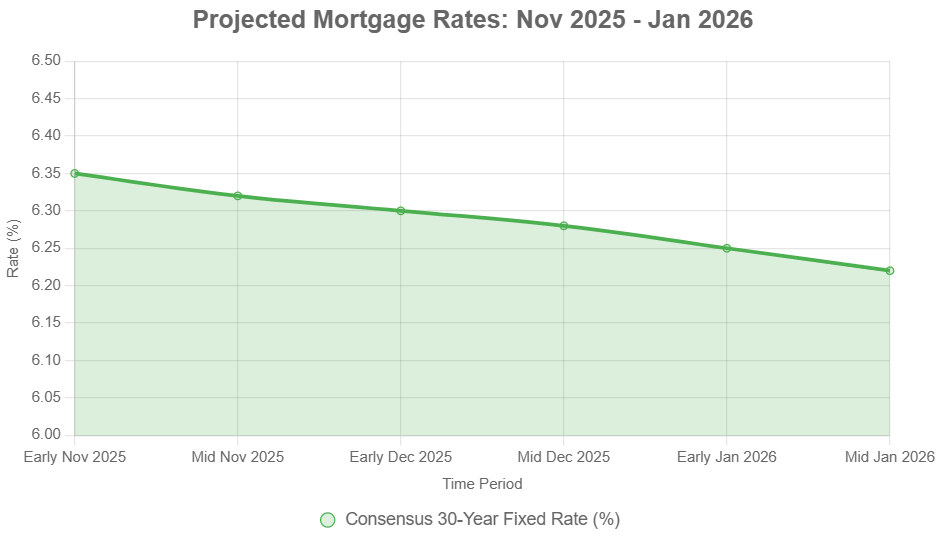

Mortgage rate predictions for 2026 by top housing experts largely point towards a period of stabilization, with the average 30-year fixed-rate mortgage hovering between 6.0% and 6.4%. While most anticipate a relatively flat year for rates, a slight dip might occur towards the end of 2026 as the Federal Reserve's efforts to manage the economy mature.

It’s a question on so many minds right now: what will happen with mortgage rates in the coming years, especially as we look ahead to 2026? As someone who’s been following the housing market for a while, I know how much these numbers impact people’s decisions, whether they’re buying their first home, looking to upgrade, or even just dreaming about owning. The good news is, the chatter among the pros suggests we're moving out of the wild swings we've seen and into a more predictable phase.

What Leading Housing Experts Predict for Mortgage Rates in 2026

What the Experts Are Saying: A Look at 2026 Mortgage Rates

After a period of significant ups and downs, the common thread among leading housing experts for 2026 is stability. The general consensus is that the dramatic rate hikes and cuts are likely behind us, and we're settling into a range that feels more like a “new normal” for borrowing.

Here’s a breakdown of what some major players in the housing finance world are predicting for the average 30-year fixed-rate mortgage in 2026:

- Fannie Mae: They see a gentle downward trend, starting the year (Q1) around 6.2% and easing to about 5.9% by the close of 2026. This suggests a modest improvement as the year progresses.

- National Association of Realtors (NAR): The NAR is a bit more optimistic, projecting an average rate of 6.0% for the entire year. This would be a noticeable drop from the higher rates we saw in earlier 2025.

- Wells Fargo: Their crystal ball shows rates staying above the 6% mark. They foresee an annual average of around 6.18%, indicating a persistent high-interest environment.

- Realtor.com: This platform expects a pretty flat trend, with an average rate of 6.3% throughout 2026. This is slightly lower than their reported full-year average for 2025.

- Mortgage Bankers Association (MBA): They have the most conservative outlook, predicting rates to remain steady at 6.4% across all quarters of 2026. This forecast highlights a “new normal” where affordability might remain a challenge.

- Freddie Mac: Current analyses put their 2026 outlook near 6.2%, though they've been less specific with detailed quarterly figures for the later half of the year.

- Morgan Stanley: While they don't always release granular mortgage rate predictions for specific years, their broader economic forecasts generally align with a stabilization in the low-to-mid 6% range as the Federal Reserve aims for a more balanced economic stance.

Key Themes Shaping 2026 Mortgage Rates

When I look at these predictions, a few main ideas keep coming up:

- The “Flat” Forecast: The overwhelming sentiment is that the wild ride of mortgage rate volatility is over. We're looking at a period where rates might not change dramatically, which, in my opinion, is actually a good thing for planning. It allows buyers and sellers to make more informed decisions without the constant worry of big swings.

- The 6% Barrier: While some, like Fannie Mae and NAR, hint at dipping below 6% by year-end, the general feeling is that sub-6% rates will be more of an occasional guest than a permanent resident. For many, this means adjusting their expectations from the ultra-low rates of a few years ago.

- Home Prices vs. Rates: Even with stable or slightly falling mortgage rates, it’s important to remember that home prices are still expected to creep up, likely by 1.3% to 4.0% nationally in 2026. This is a crucial point: waiting for significantly lower rates might mean facing higher purchase prices down the line.

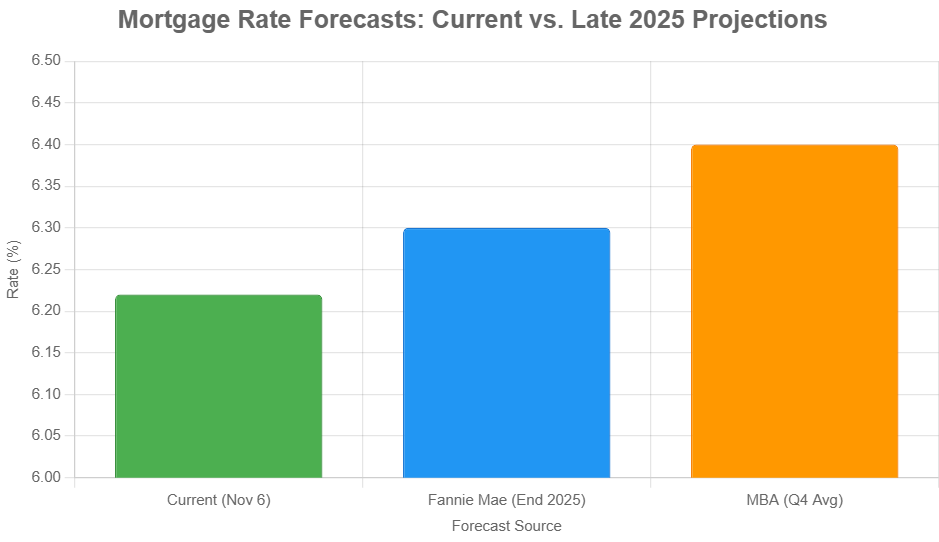

Understanding the MBA's 6.4% Outlook: A Deeper Dive

The Mortgage Bankers Association's (MBA) prediction of a 6.4% average rate for 2026 is particularly interesting because it paints a picture of persistent affordability challenges. While this is an improvement from the over 7% rates seen in early 2025, it's still a good bit higher than the sub-4% rates that many enjoyed not too long ago.

Let's break down what a 6.4% rate could mean:

- Continued Pressure on Budgets: Monthly mortgage payments will likely remain high for many buyers. This, combined with still-rising home prices, means that saving for a down payment and qualifying for a loan will continue to be a hurdle.

- A “New Baseline” for Buyers: For those who have been on the sidelines waiting for a return to 3% or 4% rates, the MBA's forecast suggests a need to recalibrate. A range of 6% to 6.5% is increasingly seen as the new normal, and many buyers may decide it's time to enter the market rather than wait indefinitely.

- A Modest Boost in Sales: Despite the affordability challenges, the MBA expects a modest increase in home sales. They anticipate single-family mortgage originations to rise to $2.2 trillion in 2026, up from $2.05 trillion in 2025. This suggests that while rates aren't rock-bottom, other factors like improved inventory and stable incomes will drive some activity.

- Flat or Slightly Falling Home Prices: The MBA's forecast is linked to an expectation that national home prices will be largely stable or even see a slight dip by late 2026. This would offer some incremental relief on affordability, though it contrasts with more optimistic growth forecasts from other agencies.

- Limited Opportunities for Refinancing: If rates hold steady or begin to edge up in 2027, the MBA predicts that refinancing activity will remain subdued. Not many homeowners will find themselves in a position where refinancing offers a significant financial advantage.

- Market Predictability: The consistent 6.4% prediction signifies a period of market stability. This stability, in my view, is a big plus. It removes a layer of uncertainty that can make planning for a home purchase so stressful.

What Could Push Rates Lower Than Expected?

While the consensus is for stability, there are a few scenarios that could push mortgage rates below the predicted ranges. It all hinges on how certain economic indicators perform.

Here are the key factors that might lead to lower mortgage rates:

- Inflation Hits the Target: The biggest driver for lower rates would be if inflation consistently cools down to the Federal Reserve's 2% target. If the Fed sees a sustained drop in inflation, they'll likely feel more comfortable making more significant interest rate cuts, which would then ease pressure on mortgage rates.

- A Softer Job Market: If the U.S. labor market shows signs of significant weakening, like a sharp rise in unemployment (say, above 4.5%), that would signal a slowing economy. In response, the Fed might cut rates more aggressively to try and stimulate growth, leading to lower mortgage rates.

- Economic Slowdown or Recession: Any major, unforeseen economic shock, like a significant drop in consumer spending or a financial crisis, could trigger a recession. In such “flight to safety” situations, investors tend to move their money into safer assets like U.S. Treasury bonds. This increased demand for bonds drives their yields down, and consequently, mortgage rates tend to follow.

- Sharp Drop in Bond Yields: Mortgage rates are very closely tied to the yield on the 10-year U.S. Treasury note. For mortgage rates to genuinely fall below 6%, the 10-year Treasury yield would likely need to drop considerably from its projected 4% range. This often happens when there's global economic uncertainty or strong demand for these safe investments.

- Narrowing Mortgage Spreads: The difference between the 10-year Treasury yield and the 30-year fixed mortgage rate (known as the “mortgage spread”) has been wider than usual lately. If this spread narrows and returns to its historical average, it could help lower mortgage rates even if Treasury yields don't change much.

Ultimately, navigating the mortgage market requires staying informed and understanding these different possibilities. While the experts lean towards a stable year for mortgage rates in 2026, keeping an eye on economic indicators will be key for anyone hoping for more favorable borrowing costs.

With forecasts from top industry experts, mortgage rates for 2026 remain a critical factor for buyers and investors. Whether rates stabilize, rise, or finally decline, the impact on affordability and cash flow is significant.

Norada Real Estate helps you navigate these shifts with turnkey rental properties designed to deliver consistent passive income and appreciation—so you can build long‑term wealth regardless of where mortgage rates move.

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Why Are Mortgage Rates Going Up in 2025: Will Rates Drop?

- Why Are Mortgage Rates So High and Predictions for 2025

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?