Based on what I'm seeing and hearing from the experts, combined with the latest economic figures and recent rate trends, it's highly unlikely that average 30-year fixed mortgage rates will drop below 6% within the next two months. While I know that's probably not the news some of you were hoping for, it’s important to have a realistic picture of where things stand.

Can Mortgage Rates Drop Below 6% in the Next 2 Months?

Predicting these things precisely is more of an art than a science. There are a lot of moving parts, and even the most respected analysts often have differing opinions. However, the consensus among major players like Fannie Mae and the Mortgage Bankers Association (MBA) suggests that we’ll likely see rates stay above that 6% mark through the end of 2025.

Some forecasts even suggest a possibility of dipping below 6% by late 2026. While a short-term forecast from HSH.com (ending January 2, 2026) places average rates in the 5.98% to 6.38% range, this still hints at staying right around or just above the 6% threshold in the immediate future.

So, What’s Really Driving Mortgage Rates Right Now?

It's easy to look at mortgage rates and think they’re just plucked out of thin air. But in reality, they're deeply connected to the economy and the decisions made by big players like the Federal Reserve. Think of it like a complex machine with many gears.

The Federal Reserve's Balancing Act

You’ve probably heard a lot about the Federal Reserve (often called the “Fed”). They are the central bank of the United States, and one of their main jobs is to manage the economy by influencing interest rates. Back in September and October of 2025, the Fed made two rate cuts, each of 25 basis points. This was a move designed to help out a labor market that was showing signs of weakness.

Now, a common question I get is: “Will these cuts automatically make my mortgage cheaper?” Not directly, and not overnight. The Fed’s cuts directly impact the federal funds rate, which is a short-term borrowing rate between banks. While this influences everything else in the financial system, mortgage rates are more closely tied to longer-term trends.

The big unknown is whether the Fed will decide to cut rates again in December. Officials are looking at a lot of data, and honestly, they're getting some mixed signals. Some see the economy improving, while others are still concerned about inflation. This uncertainty is a huge reason why mortgage rates aren't dropping rapidly. Traders are essentially split on whether another December cut will happen.

Inflation's Persistent Glow

Let’s look at the numbers. As of mid-November 2025, the latest figures show a Core CPI of around 2.95% year-over-year, with the overall headline CPI at roughly 2.99%. This means inflation has been rebounding slightly, largely thanks to higher energy and shelter costs, but it’s still hanging below the critical 3% mark.

- October 2025 Inflation Recap: Monthly data for October showed CPI increasing by 0.31% and Core CPI by 0.25%.

While these numbers are concerning enough to make the Fed cautious, they aren't so high that they necessarily demand immediate, aggressive action to raise rates. This persistent, but not runaway, inflation is a key factor keeping the Fed from aggressively lowering rates, which in turn keeps mortgage rates from dropping sharply.

The Job Market: Still Resilient, But Showing Cracks

The labor market is another crucial piece of the puzzle for the Fed. According to ADP, US companies have been shedding jobs at an average of about 2,500 per week in the four weeks leading up to November 1, 2025. Now, that might sound alarming, but it's a relatively small number in the grand scheme of the US economy.

We’re still awaiting updated government reports for October due to recent delays, but the September 2025 employment data gave us a picture of around 50,000 new jobs added, with the unemployment rate holding steady at 4.3%.

So, what does this tell us? The job market isn't roaring back to life, but it also isn't collapsing. This “middle ground” is what gives the Fed room to consider rate cuts, but the slight softening we're seeing in job additions might be enough to encourage them to pause and assess further before December.

Treasury Yields: A Modest Downward Trend

When we talk about mortgage rates, it's impossible to ignore the 10-year Treasury yield. As of November 18, 2025, this important benchmark is sitting at 4.12%.

What’s interesting is that this yield has declined modestly from earlier highs. It's actually about 0.29 percentage points lower than it was at the same time last year. This downward movement is a direct reaction to investors anticipating further Fed action and responding to the softer economic data we've been seeing, such as the jobs figures and the sticky-but-not-exploding inflation. Lower Treasury yields generally translate to lower mortgage rates, but as you can see, 4.12% on the 10-year yield doesn't typically translate to a 30-year fixed mortgage rate much below 6%.

Where Are Mortgage Rates Actually Sitting?

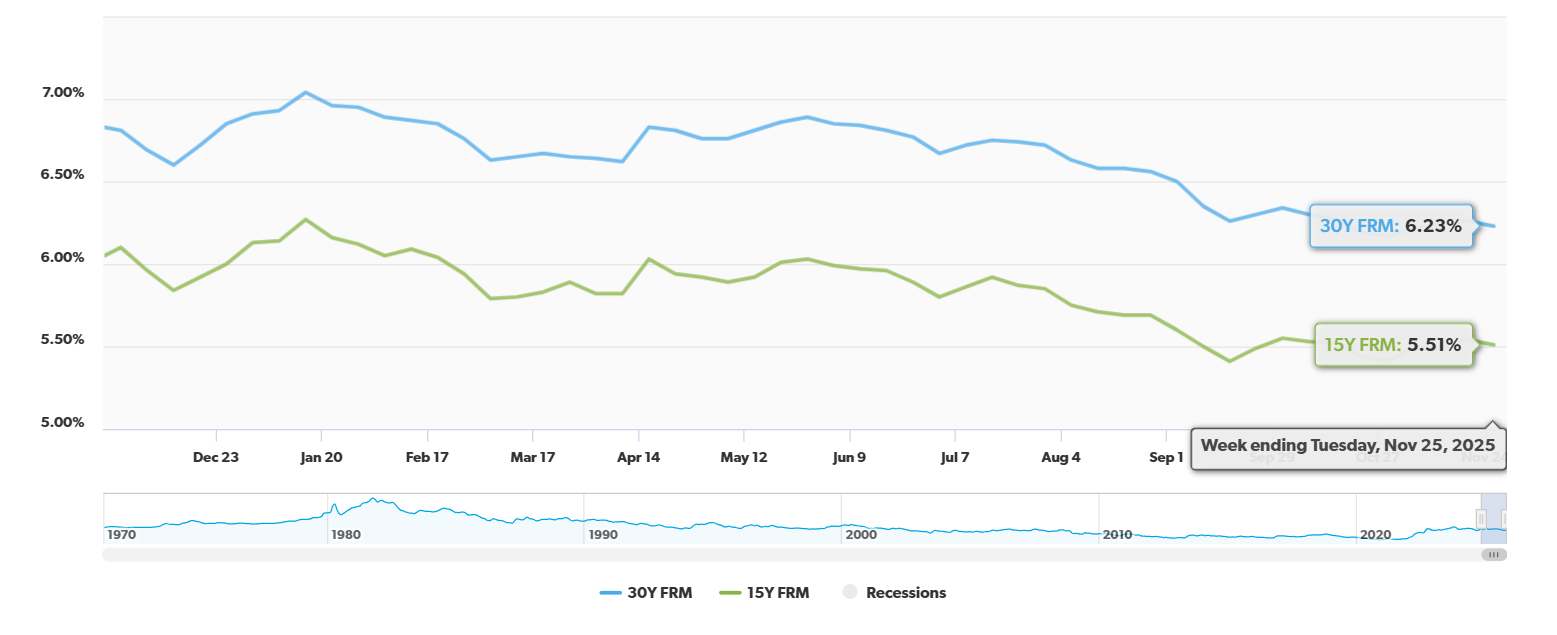

Looking at the Primary Mortgage Market Survey® data from November 13, 2025, provides a very current snapshot. The average 30-Year Fixed-Rate Mortgage (FRM) is currently at 6.24%.

It's worth noting that this is a slight increase of 0.02% from the week prior. However, when we look back a year, it's a significant improvement, down -0.54% from the same time last year. The monthly average is sitting just below at 6.21%, and the 52-week average is higher at 6.67%. The 52-week range has seen rates as low as 6.17% and as high as 7.04%.

Even the 15-Year Fixed-Rate Mortgage (FRM), which typically offers a lower rate, is at 5.49%. This is down just a hair by -0.01% from the previous week and down -0.50% year-over-year.

These figures from the survey reinforce the idea that we're hovering right around that 6% mark, and the very slight uptick within the last week suggests that any immediate downward pressure is being countered by other market forces.

Related Topics:

Mortgage Rate Predictions for the Next 30 Days: Nov 10 to Dec 10, 2025

Mortgage Rates Predictions for the Next 12 Months: Nov 2025 to Nov 2026

Mortgage Rates Predictions for Next 90 Days: October to December 2025

What Does This Mean for You as a Homebuyer?

Seeing a target like “sub-6% mortgage rates” can make anyone want to hit the pause button on their homebuying plans. I understand that temptation. However, from my experience, waiting for the “perfect” rate is often a gamble that doesn’t pay off. Here’s why:

- Predicting the Future is Hard (Really Hard!): As we've discussed, there are so many economic forces at play. Even experts get it wrong. You could wait for rates to drop, only to find they actually go up, or stay the same. The slight week-over-week increase in the 30-year FRM shows just how sensitive these numbers are.

- Home Prices Can Keep Rising: While higher mortgage rates can cool down buyer demand slightly, in many areas, low inventory continues to be a major issue. If rates do drop significantly in the future and more buyers flood the market, home prices could easily tick back up. You might end up paying more for the house in price, even if your monthly payment is similar due to a lower rate.

- You Can Improve Your Odds: Instead of just waiting, I always advise my clients to focus on what they can control.

- Boost Your Credit Score: Even a small improvement can make a difference. Pay bills on time, reduce credit card balances.

- Save for a Bigger Down Payment: More money down means borrowing less and potentially getting a better rate.

- Shop Around: This is HUGE! Don't just go with the first lender you talk to. Get quotes from at least 3-5 different lenders – banks, credit unions, mortgage brokers. You might be surprised at the differences.

- Explore Different Loan Options: Have you talked about an adjustable-rate mortgage (ARM)? While they come with their own risks, the introductory rates can be lower than fixed rates. Or consider a shorter loan term if your budget allows for the higher monthly payment; you'll pay significantly less interest over the life of the loan and potentially can get a lower fixed rate.

My Personal Take: Don't Be Paralyzed by Rate Fear

I’ve seen buyers hold off for months, even years, waiting for rates to hit a certain number. Sometimes it works out, but more often than not, they either miss out on a home they loved or end up paying more overall because of rising prices.

My advice is to figure out what monthly payment you are comfortable with and what you can afford today. Get your finances in order, get pre-approved, and start your home search. You can always refinance down the line if rates do drop significantly. Many homeowners who bought homes in recent years when rates were also elevated have since refinanced to lower rates. It's a strategy that has worked for many, and it could work for you too.

The market is dynamic, and while it looks improbable that we'll see average mortgage rates plummet below 6% in the next 60 days, that doesn't mean buying a home isn't a smart move for you right now. Focus on your financial health, do your homework, and make a decision that feels right for your personal circumstances.

Want Stronger Returns? Invest Where the Housing Market’s Growing

Turnkey rental properties in fast-growing housing markets offer a powerful way to generate passive income with minimal hassle.

Work with Norada Real Estate to find stable, cash-flowing markets beyond the bubble zones—so you can build wealth without the risks of ultra-competitive areas.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Who Benefits Most from Today's Lower Mortgage Rates?

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?