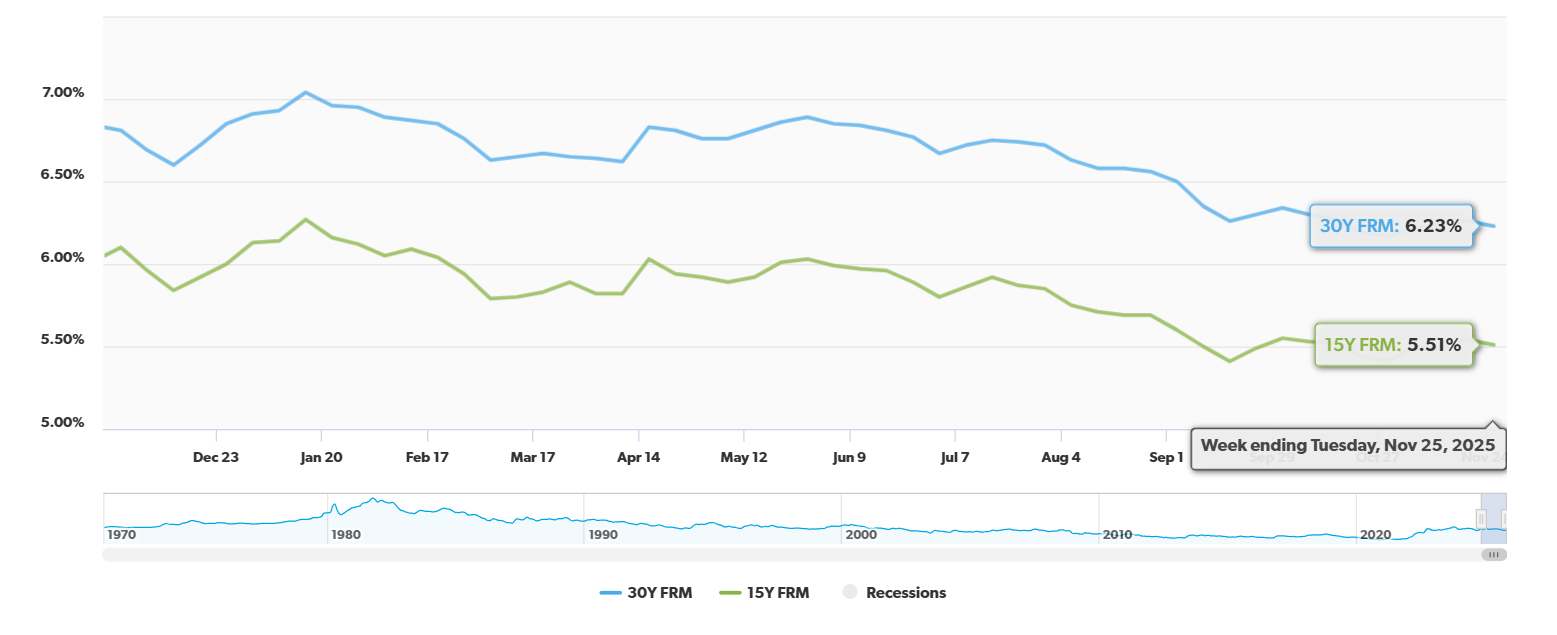

The good news is out: mortgage rates have dropped just before Thanksgiving, offering a much-needed glimmer of hope for those looking to buy a home or refinance. This is a welcome shift, and as of November 26, 2025, the average 30-year fixed-rate mortgage (FRM) is sitting at 6.23%, according to Freddie Mac's latest Primary Mortgage Market Survey®.

I’ve been following the housing market closely for years, and seeing these numbers ease before such a major holiday feels significant. It's not just a small dip; compared to this time last year, when the 30-year FRM was averaging a much higher 6.81%, this is a noticeable improvement. It suggests that the housing market, while complex, is responding to economic shifts in ways that can benefit hopeful homeowners.

Mortgage Rates Fall Ahead of Thanksgiving, Offering Buyers Rare Holiday Relief

What Does This Mean for You?

Let's break down these numbers and what they could mean for your wallet and your homeownership dreams. When mortgage rates go down, your monthly payments can become more affordable, and you might be able to afford a slightly more expensive home or save a considerable amount of money over the life of your loan.

Here's a look at how the rates have changed, according to Freddie Mac:

| Mortgage Type | Current Average (11/26/2025) | 1-Week Change | 1-Year Change |

|---|---|---|---|

| 30-Year FRM | 6.23% | -0.03% | -0.58% |

| 15-Year FRM | 5.51% | -0.03% | -0.59% |

Seeing both the 30-year and 15-year fixed-rate mortgages decrease is a positive signal across the board. For many, the 30-year fixed rate is the go-to choice for its predictable monthly payment and the ability to spread out payments over a longer period. The 15-year fixed rate, while leading to higher monthly payments, often offers a lower overall interest cost and allows homeowners to build equity faster.

The Expert Take: Why the Drop?

As Freddie Mac's Chief Economist, Sam Khater, pointed out, this decrease comes as a pleasant surprise heading into the Thanksgiving week. He noted that pending home sales are at their highest level since last November, indicating that buyer activity is showing resilience. This is a crucial piece of insight – even with economic uncertainties, people are still actively looking to buy homes.

So, what's behind these rates heading in the right direction? I’ve been thinking a lot about the interplay of economic factors, and here are a few key reasons I believe are driving this trend:

- Federal Reserve's Interest Rate Moves: The Federal Reserve plays a huge role in setting the tone for interest rates. There's been anticipation, and in some cases, action, regarding rate cuts from the Fed. When the Fed signals or enacts rate cuts, it often leads directly to lower mortgage rates. The market is currently factoring in a potential rate cut in December, which would naturally push mortgage rates down. I've seen this pattern play out before – anticipated Fed actions can move markets even before they officially happen.

- Cooling Inflation and Economy: As the economy starts to cool down and inflation eases its grip, there’s less pressure on the Fed to keep interest rates high. Think of it like this: when prices everywhere are soaring, the Fed raises rates to slow things down. When those prices start to stabilize or even decrease, they have more room to ease up on rates. Signs of a softening job market, while potentially concerning for some, can also contribute to lower borrowing costs.

- Investor Behavior: Mortgage rates aren't set in a vacuum; they are closely tied to the performance of things like the 10-year Treasury yield. When investors feel confident that interest rates will continue to fall, they tend to buy more bonds. This increased demand for bonds pushes their prices up and their yields down, which, in turn, often leads to lower mortgage rates for consumers.

Navigating the Nuances: What Could Slow This Down?

While it's fantastic to see rates dropping, it's important to remember that the economy is a dynamic beast. Several factors could prevent these rates from falling much further or might cause them to fluctuate:

- Stubborn Inflation: If inflation proves to be more persistent than anticipated, the Federal Reserve might be hesitant to make significant rate cuts. They are primarily focused on getting inflation back to their target. If inflation doesn't cooperate, it could put a ceiling on how low mortgage rates can go.

- Fed's Cautionary Stance: The Fed is walking a tightrope, balancing economic growth with inflation control. Any unexpected upward movement in inflation or a strong economic indicator could make them pause or even reverse course on rate cuts, causing volatility in mortgage rates.

- Increased Buyer Demand: This might sound counterintuitive, but as mortgage rates fall, more people are likely to enter the housing market. This surge in demand can sometimes lead to increased competition and a rise in home prices. While lower rates are great, if home prices shoot up significantly, it could partially offset the savings.

Looking Ahead: Expert Predictions for 2026

So, what does the future hold? It seems the general consensus among experts is that mortgage rates are likely to trend downwards through late 2025 and into 2026. However, the key word here is gradually. Most forecasts suggest rates will likely settle in the low-to-mid 6% range rather than plummeting dramatically.

Here’s what some major organizations are projecting for the average 30-year fixed rate in 2026:

| Organization | 2026 Forecast (Average 30-Yr FRM) |

|---|---|

| Fannie Mae | 5.9% |

| Mortgage Bankers Association (MBA) | 6.4% |

| National Association of Realtors (NAR) | Around 6% |

As you can see, there's a range of predictions, but a common theme is a move towards slightly lower rates. Fannie Mae is the most optimistic, projecting a dip below 6%, while the MBA sees rates holding relatively steady. The NAR’s forecast lands somewhere in the middle, painting a picture of continued moderation.

From my perspective, these predictions highlight the inherent uncertainty. While many expect a downward trend, unexpected economic events can always shift the outlook. The most important thing for potential buyers and homeowners is to stay informed and work with trusted advisors to navigate these potential changes.

How the Rate Drop Could Translate to Savings

Let's put this into perspective with a simple example. Imagine you're looking to buy a $300,000 home.

- At 6.81% (Last Year): Your estimated monthly payment (principal and interest) would be approximately $1,975.

- At 6.23% (Current Rate): Your estimated monthly payment (principal and interest) would be approximately $1,844.

That's a difference of $131 per month, or about $1,572 per year in savings on just this one loan. Over the 30-year life of the mortgage, this could amount to tens of thousands of dollars saved. This is why even small drops in mortgage rates can have a significant impact on affordability and your overall financial well-being.

Final Thoughts

This pre-Thanksgiving drop in mortgage rates is more than just a statistic; it's a sign of the market responding to economic signals and potentially offering a more accessible entry point for many into homeownership. While challenges remain, and volatility is always a possibility, this is a moment for optimism. If you've been on the fence about buying or refinancing, now might be a good time to explore your options.

Mortgage Rates Fall Just in Time for Thanksgiving

Rates dipping before the holiday are giving homebuyers and investors a rare seasonal advantage—lower monthly payments and stronger affordability heading into year-end.

Norada Real Estate helps you seize this opportunity with turnkey rental properties in high-demand markets—so you can lock in financing and passive income while rates remain favorable.

🔥 HOT HOLIDAY LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?