If you're anything like me, the thought of buying a home or even just keeping up with mortgage payments in today's economy can feel a little overwhelming. That's why when someone like Dave Ramsey, a guy who's built a career on giving straightforward financial advice, talks about the housing market, people tend to listen.

And recently, he's made a pretty significant prediction: major mortgage rate changes are likely on the horizon soon. In fact, Ramsey believes these changes, specifically a drop in rates, could be the key to unlocking a more active housing market. So, what exactly did he say, and more importantly, what does it mean for those of us dreaming of owning a home or looking to make our current mortgage more manageable? Let's dive in.

Dave Ramsey Predicts Mortgage Rates Will Drop Soon in 2025

Who is Dave Ramsey and Why Should We Care?

For those who might not be as familiar, Dave Ramsey is a personal finance guru. He's the author of several best-selling books, most notably The Total Money Makeover, and hosts the nationally syndicated The Ramsey Show. What I appreciate about Ramsey is his down-to-earth approach to money. He doesn't speak in complicated financial jargon; he tells it like it is.

Having navigated his own financial ups and downs, including a bankruptcy early in his career, he speaks from experience. He's built a massive following by offering practical, no-nonsense advice on getting out of debt, saving, and building wealth. When he talks about mortgages, people pay attention, especially because he often advocates for more conservative approaches like the 15-year fixed-rate mortgage.

Ramsey's Forecast: Lower Mortgage Rates Ahead

In a recent interview with TheStreet, Ramsey shared his prediction that mortgage rates will “probably fall.” This isn't just a casual hunch; he believes this potential decrease could be the spark that the current housing market needs to see a significant uptick in activity. While he didn't throw out specific numbers, he suggested that even a one to two percentage point drop could lead to what he called a “home buying frenzy” due to the pent-up demand that's been building up.

This prediction comes at a crucial time. We've seen mortgage rates climb quite a bit, which has understandably made many potential homebuyers hesitant. Ramsey's optimistic outlook is interesting because, while some experts are cautiously optimistic, others anticipate rates staying relatively high for a while longer. His focus on a potential near-term drop suggests he sees factors at play that could lead to improved affordability for buyers.

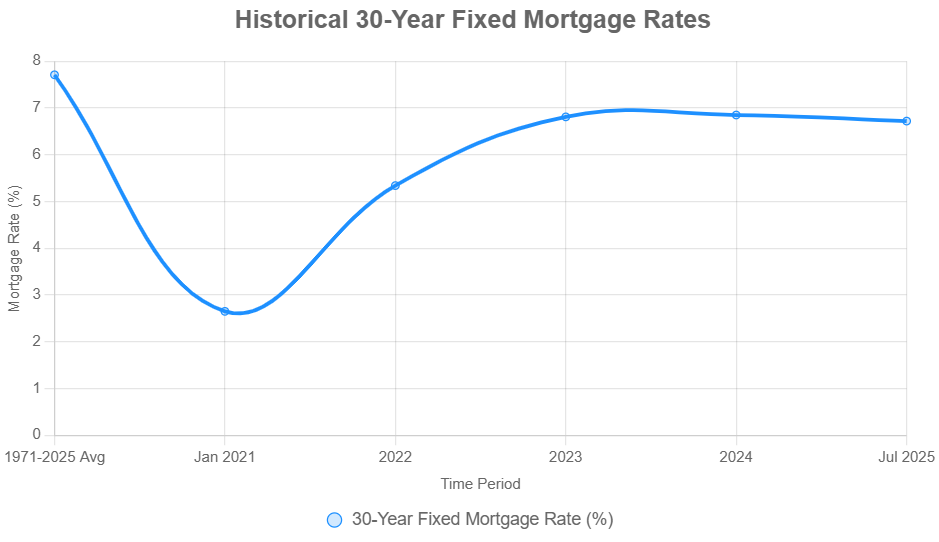

The Current Mortgage Rate Landscape (May 2025)

To put Ramsey's prediction into context, let's take a look at where mortgage rates stand right now, in May 2025.

- The average rate for a 30-year fixed mortgage is hovering around 6.8%. Sources like Freddie Mac reported it at 6.76% for the week ending May 8th, 2025, while Bankrate showed a slightly higher 6.91% for the same type of refinance.

- If you're considering a shorter term, the 15-year fixed-rate mortgage is averaging between 5.89% and 5.92%. This lower rate comes with higher monthly payments but saves you significantly on interest over the life of the loan, something Ramsey often emphasizes.

- For those looking to refinance a 30-year fixed mortgage, the average is around 6.91%, according to Bankrate.

- Even jumbo mortgages, for higher-priced homes, are sitting at about 6.80%.

It's worth remembering that these rates are down a bit from their peak of 7.79% in October 2023, but they're still considerably higher than the sub-3% rates we saw just a few years ago. This jump is a big reason why many people are feeling the pinch when it comes to buying or refinancing a home.

What Drives Mortgage Rates? A Look Under the Hood

Understanding why mortgage rates fluctuate is key to making sense of any predictions. Several factors play a significant role:

- Inflation: When the cost of goods and services rises (inflation), lenders often demand higher interest rates to ensure their returns don't lose purchasing power over time. Recent reports have highlighted that persistent inflation is a major reason why rates have remained elevated.

- Federal Reserve Policies: The Federal Reserve (the Fed) sets the federal funds rate, which is the rate banks charge each other for overnight borrowing. While this doesn't directly set mortgage rates, it significantly influences them. Even though the Fed cut rates a few times in 2024, mortgage rates haven't mirrored that decrease completely, indicating other market forces are at play.

- Economic Growth: A strong economy usually means more demand for credit, which can push interest rates higher. Conversely, if the economy slows down, rates might decrease to encourage borrowing and spending.

- Bond Market Yields: Mortgage rates tend to closely follow the yield on the 10-year Treasury note. This yield reflects investors' confidence in the economy and their expectations for future inflation.

- Global and Geopolitical Events: Things happening around the world, like trade disputes, fears of recession, and instability in financial markets, can also impact mortgage rates by affecting bond yields. For instance, recent tariff announcements have been cited as a factor influencing bond markets.

Because these factors are constantly shifting and interacting, predicting future mortgage rates with absolute certainty is incredibly difficult. Ramsey's prediction likely takes these dynamics into account, but ultimately reflects his belief that the scales will tip towards lower rates in the near future.

What Other Experts Are Saying

It's always a good idea to see how Ramsey's prediction aligns with what other experts in the field are saying. Here's a snapshot of some forecasts:

- The National Association of Home Builders (NAHB) projects the average 30-year fixed-rate mortgage to be around 6.62% by the end of 2025 and slightly above 6% by the end of 2026.

- Analysts at U.S. News anticipate rates to stay in the mid-6% range throughout 2025 and 2026, citing ongoing economic uncertainty and a cautious approach from the Federal Reserve.

- Both Freddie Mac and the Mortgage Bankers Association (MBA) are also forecasting a gradual decline, with rates stabilizing around 6.5% by late 2025.

While these projections generally point towards a downward trend, they seem a bit more measured in their optimism compared to Ramsey's suggestion of a potential “frenzy.” Most experts agree that a return to the very low rates of the early 2020s is unlikely, a point Ramsey himself has acknowledged.

Read More:

Mortgage Rates Forecast: May 8-14, 2025 – What Experts Predict

Will Mortgage Rates Finally Go Down in May 2025?

Future of Mortgage Rates Post-Fed Decision: Will Rates Drop?

Fed's Decision Signals Mortgage Rates Won't Go Down Significantly

Potential Ripple Effects: How Lower Rates Could Impact You and the Housing Market

If Ramsey's prediction, or even the more conservative expert forecasts, come to pass, we could see some significant effects on both homebuyers and the broader housing market:

- Lower Monthly Payments: Even a small drop in interest rates can make a big difference in your monthly mortgage payment. For example, if the rate on a $300,000 30-year fixed mortgage drops from 6.8% to 6%, the monthly payment could decrease by around $157. Over the life of the loan, that adds up to significant savings – over $56,000 in interest! This increased affordability could bring more people into the market.

- Increased Buying Power: Lower rates mean you can afford to borrow more money for the same monthly payment. This could open up options for buyers to consider larger homes or homes in more desirable locations.

- Refinancing Opportunities: For current homeowners with mortgages at higher interest rates, a drop could present an opportunity to refinance and secure a lower rate. This could reduce their monthly payments or allow them to shorten their loan term, saving them money on interest in the long run.

- Market Dynamics: As more buyers enter the market due to improved affordability, we could see increased competition for available homes. Ramsey believes that this strong demand will likely keep home prices stable or even push them higher.

However, it's important to remember that the housing market faces other challenges. Limited inventory and home prices that have risen faster than wages are still significant hurdles. The fact that only 33% of 27-year-olds own homes today, compared to 40% of baby boomers at the same age, underscores the affordability issues many face. While lower rates would be a welcome development, they need to be considered alongside these existing market realities.

Ramsey's Advice for Navigating the Current Market

Regardless of when and how much mortgage rates might change, Dave Ramsey's advice for homebuyers remains consistent: don't try to time the market. He emphasizes that trying to predict the absolute lowest point for rates is a risky game. Instead, he advises purchasing a home when you are truly financially ready.

For Ramsey, being financially ready means:

- Being debt-free (excluding the mortgage itself).

- Having a 3–6 month emergency fund in place.

- Opting for a 15-year fixed-rate mortgage where the monthly payment, including taxes and insurance, doesn't exceed 25% of your take-home pay.

He is a strong advocate for the 15-year mortgage over the traditional 30-year term, highlighting the massive amount of interest you can save over the shorter loan period. For those considering refinancing, his advice is to carefully evaluate whether the lower interest rate and potentially shorter term justify the associated closing costs.

Final Thoughts: Staying Informed in a Changing Landscape

Dave Ramsey's prediction of upcoming mortgage rate changes offers a beacon of hope for a housing market that has felt out of reach for many. While the exact timing and extent of these changes remain to be seen, his forecast aligns with a general expectation among experts for a gradual decline in rates. For those of us navigating the complexities of buying a home or managing a mortgage, staying informed about these trends and understanding the underlying economic factors is crucial. Ultimately, Ramsey's core advice – to be financially prepared and make wise, long-term decisions – remains timeless, no matter where mortgage rates go.

Invest Smarter in a High-Rate Environment

With mortgage rates remaining elevated so far this year, it's more important than ever to focus on cash-flowing investment properties in strong rental markets.

Norada helps investors like you identify turnkey real estate deals that deliver predictable returns—even when borrowing costs are high.

HOT NEW LISTINGS JUST ADDED!

Connect with a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Expect High Mortgage Rates Until 2026: Fannie Mae's 2-Year Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Why Are Mortgage Rates Going Up in 2025: Will Rates Drop?

- Why Are Mortgage Rates So High and Predictions for 2025

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?