Good news for prospective homebuyers and those looking to refinance! As of today, March 29, 2025, mortgage rates have generally decreased compared to the beginning of the year. This dip offers a potential window for securing a more favorable interest rate on your home loan or refinance.

Today's Mortgage Rates – March 29, 2025: Rates See a Slight Dip

Key Takeaways:

- Mortgage rates today have mostly decreased.

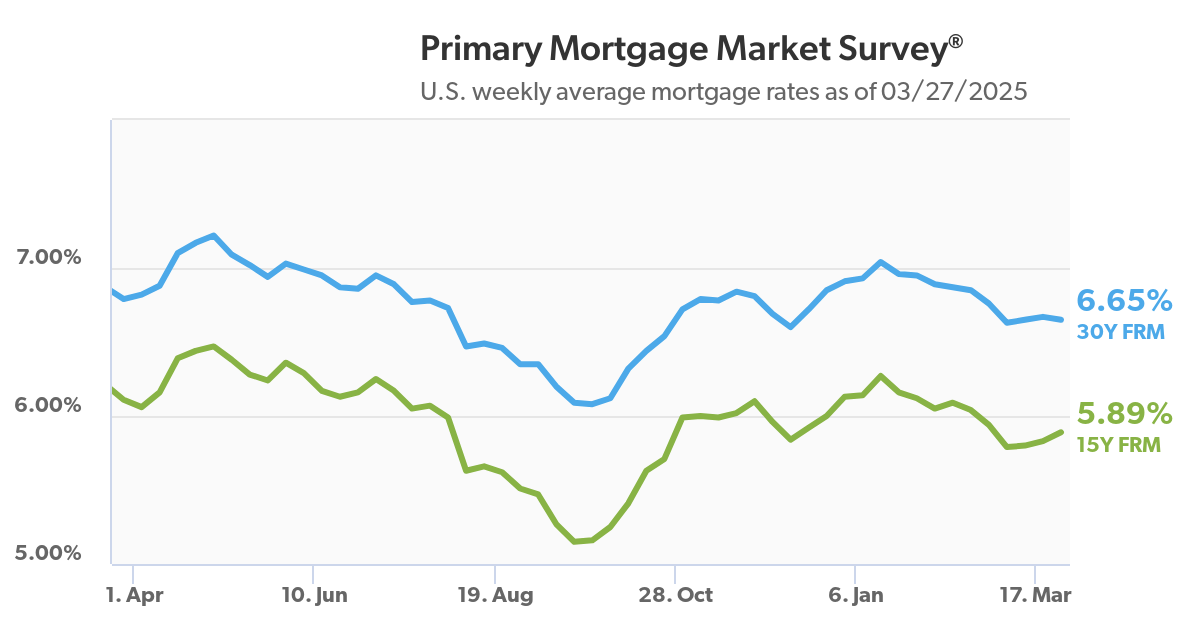

- The 30-year fixed mortgage rate is currently at 6.59%, down three basis points.

- The 15-year fixed rate has also dropped, now at 5.91%, a decrease of four basis points.

- Refinance rates have also seen a similar downward trend.

- Experts at Fannie Mae predict mortgage rates will likely continue to move lower through the rest of 2025 and into 2026.

- While a good time to buy compared to the peak of the pandemic, the absolute best time depends on your individual circumstances.

According to the latest data from Zillow, the trend we've seen since the start of 2025 of slightly decreasing mortgage rates continues today. For those in the market to purchase a new home, this small reduction in rates can translate to modest savings over the life of the loan.

Similarly, homeowners who have been considering refinancing their existing mortgage might find today's refinance rates more appealing than what was available earlier in the year. It's worth noting, however, that while these are national averages, the specific rate you'll qualify for will depend on a variety of factors, including your credit score, down payment amount, and the type of loan you choose.

Current Mortgage Rates on March 29, 2025

Here’s a snapshot of the national average mortgage rates being offered today:

| Loan Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.59% |

| 20-Year Fixed | 6.41% |

| 15-Year Fixed | 5.91% |

| 5/1 ARM | 6.82% |

| 7/1 ARM | 7.13% |

| 30-Year VA | 6.09% |

| 15-Year VA | 5.67% |

| 5/1 VA | 6.22% |

Keep in mind that these are just averages. The actual mortgage rate you receive could be higher or lower.

Today's Mortgage Refinance Rates

If you're thinking about refinancing your current home loan, here are the average mortgage refinance rates as of today:

| Loan Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.55% |

| 20-Year Fixed | 6.27% |

| 15-Year Fixed | 5.84% |

| 5/1 ARM | 6.54% |

| 7/1 ARM | 6.56% |

| 30-Year VA | 6.20% |

| 15-Year VA | 5.86% |

| 5/1 VA | 6.26% |

| 30-Year FHA | 6.18% |

| 15-Year FHA | 6.04% |

Source: Zillow

Interestingly, while it's often the case that refinance rates are a bit higher than purchase rates, the data today shows some instances where they are very close or even slightly lower for certain loan products. This could present a favorable opportunity for homeowners looking to lower their monthly payments or shorten their loan term.

Understanding 30-Year Fixed Mortgage Rates

The 30-year fixed-rate mortgage remains a popular choice for many homebuyers, and for good reason. Its primary advantages lie in the predictability and relatively lower monthly payments compared to shorter-term loans. Because the interest rate stays the same over the entire 30-year period, homeowners can budget with confidence, knowing their principal and interest payment won't change. This longer repayment period spreads out the total cost of the loan, making monthly payments more manageable for some borrowers.

However, the trade-off for these benefits comes in the form of higher overall interest paid over the life of the loan. While the monthly payments are lower, you're paying interest for a longer duration, and typically at a slightly higher interest rate compared to a 15-year fixed mortgage. For example, consider a $300,000 loan. Over 30 years at an interest rate of 6.59%, the total interest paid will be significantly more than if the same loan had a 15-year term with a lower interest rate.

Exploring 15-Year Fixed Mortgage Rates

On the other end of the spectrum is the 15-year fixed-rate mortgage. The key advantages here are a lower interest rate compared to the 30-year fixed and a significantly shorter repayment period. This means you'll not only pay less interest in total but also own your home free and clear in half the time. The peace of mind that comes with a shorter mortgage term and the substantial interest savings are significant draws for many.

The main challenge with a 15-year fixed mortgage is the higher monthly payment. Because you're paying off the same loan amount in a shorter timeframe, each payment will be larger. This requires a higher level of monthly income and can impact your ability to handle other financial obligations. However, for those who can comfortably afford the higher payments, the long-term financial benefits are substantial.

Considering Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages, like the 5/1 ARM or 7/1 ARM, offer an initial fixed interest rate for a specific period (e.g., five or seven years), after which the rate adjusts periodically based on prevailing market conditions. The initial “teaser” rate is often lower than that of a comparable fixed-rate mortgage, which can result in lower monthly payments during the introductory period.

The potential downside of an ARM is the uncertainty of future interest rate adjustments. If interest rates rise after the fixed-rate period ends, your monthly payments could increase, potentially significantly. This unpredictability makes ARMs a riskier option for borrowers who plan to stay in their homes long-term or who have tight monthly budgets. However, ARMs can be attractive to those who expect to move or refinance before the adjustment period begins, allowing them to take advantage of the lower initial rate. It's crucial to fully understand the terms of an ARM, including how often the rate can adjust and the maximum possible interest rate.

Is Now the Right Time to Get a Mortgage for Your House?

The question of whether now is a good time to buy a house is a common one, and the answer is often personal and depends on individual circumstances. Compared to the rapid home price increases and sometimes higher mortgage rates seen during the peak of the COVID-19 pandemic, the current market offers a bit more stability. Home price appreciation has slowed, and as we've seen today, mortgage rates have come down slightly from the beginning of the year.

Recommended Read:

Mortgage Rates Trends as of March 28, 2025

Mortgage Rates Drop: Can You Finally Afford a $400,000 Home?

Expect High Mortgage Rates Until 2026: Fannie Mae's 2-Year Forecast

Experts at Fannie Mae's Economic and Strategic Research (ESR) Group anticipate that mortgage rates will continue their downward trend, forecasting an average of 6.3% by the end of 2025 and 6.2% by the end of 2026 [Fannie Mae]. This suggests that waiting a bit longer could potentially result in even lower borrowing costs. However, as the saying goes, the best time to buy is often when you're financially ready and find the right home for your needs. Trying to perfectly time the market is a difficult task.

What Will Be Your Mortgage Payments Today Under Current Rates?

To give you a clearer picture of what today's mortgage rates might mean for your monthly payments, let's look at a few examples. These calculations are based on the current average 30-year fixed mortgage rate of 6.59% and do not include property taxes, homeowner's insurance, or any potential private mortgage insurance (PMI), which would add to your total monthly housing cost.

Monthly Payment on $150k Mortgage

Based on a $150,000 loan at a 6.59% interest rate with a 30-year term, your estimated monthly principal and interest payment would be approximately $953 per month.

Monthly Payment on $200k Mortgage

For a $200,000 mortgage at the same 6.59% interest rate over 30 years, your estimated monthly principal and interest payment would be around $1,270 per month.

Monthly Payment on $300k Mortgage

If you were to borrow $300,000 at a 6.59% interest rate with a 30-year repayment period, your estimated monthly principal and interest payment would be approximately $1,905 per month.

Monthly Payment on $400k Mortgage

A $400,000 mortgage at 6.59% fixed for 30 years would result in an estimated monthly principal and interest payment of about $2,540 per month.

Monthly Payment on $500k Mortgage

Finally, for a $500,000 loan at a 6.59% interest rate over a 30-year term, your estimated monthly principal and interest payment would be in the neighborhood of $3,176 per month.

These examples clearly illustrate how the loan amount directly impacts your monthly mortgage payment. It's crucial to consider your budget and long-term financial goals when determining how much you can comfortably afford to borrow. Remember to also factor in the additional costs associated with homeownership beyond just the principal and interest.

Work With Norada, Your Trusted Source for

Real Estate Investment in the U.S.

Investing in turnkey real estate can help you secure consistent returns with fluctuating mortgage rates.

Expand your portfolio confidently, even in a shifting interest rate environment.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Also Read:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Why Are Mortgage Rates Going Up in 2025: Will Rates Drop?

- Why Are Mortgage Rates So High and Predictions for 2025

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?