Today's mortgage rates, as of March 18, 2025, are showing some fluctuation, leaving potential homebuyers and those looking to refinance wondering about the best course of action. The latest data indicates a mixed bag, with some rates slightly down and others inching up, all ahead of the Federal Reserve meeting.

Today's Mortgage Rates March 18, 2025: Rates Fluctuate as Fed Meeting Looms

Key Takeaways:

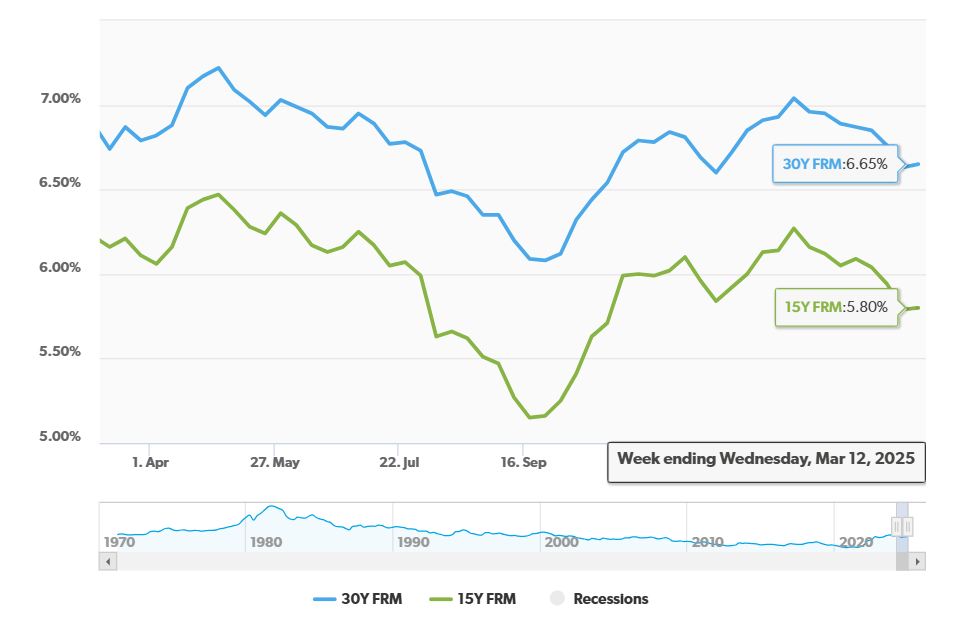

- 30-Year Fixed Rates: Slightly down to 6.57%.

- 15-Year Fixed Rates: Slightly up to 6.01%.

- Federal Reserve Meeting: Expected to influence rates in the near future.

- Refinance Rates: Generally higher than purchase rates.

- Economic Uncertainty: Continues to contribute to rate volatility.

Let's dive into the details.

Current Mortgage Rates

According to the latest data from Zillow, here's a snapshot of today's average mortgage rates across the nation:

| Loan Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.57% |

| 20-Year Fixed | 6.39% |

| 15-Year Fixed | 6.01% |

| 5/1 ARM | 6.64% |

| 7/1 ARM | 6.74% |

| 30-Year VA | 6.12% |

| 15-Year VA | 5.68% |

| 5/1 VA | 5.10% |

It's interesting to see the small dips in the 30-year and 20-year fixed rates, while the 15-year rate experienced a slight increase. Adjustable-rate mortgages (ARMs) are also in the mix, offering different options for borrowers. Keep in mind that these rates are national averages, and what you actually qualify for can depend on factors like your credit score, down payment, and overall financial situation.

Mortgage Refinance Rates Today

If you're looking to refinance your current mortgage, here's what the refinance rates look like today, according to Zillow:

| Loan Type | Interest Rate |

|---|---|

| 30-Year Fixed | 6.65% |

| 20-Year Fixed | 6.38% |

| 15-Year Fixed | 6.12% |

| 5/1 ARM | 6.74% |

| 7/1 ARM | 6.79% |

| 30-Year VA | 6.28% |

| 15-Year VA | 6.07% |

| 5/1 VA | 6.10% |

| 30-Year FHA | 6.00% |

| 15-Year FHA | 5.75% |

Notice that refinance rates are generally a bit higher than the rates for new home purchases. This is pretty typical. If you're considering a refinance, it's crucial to weigh the potential benefits, such as a lower interest rate or shorter loan term, against any associated costs.

The Fed Factor: How the Federal Reserve Impacts Mortgage Rates

Tomorrow's Federal Reserve meeting is on everyone's radar because the Fed's decisions can significantly influence mortgage rates. The Federal Reserve (also known as the Fed) is the central bank of the United States. One of the ways the Fed influences the economy is by setting the federal funds rate, which is the interest rate at which banks lend money to each other overnight.

While the federal funds rate doesn't directly determine mortgage rates, it does impact the broader interest rate environment. The Fed is not expected to cut the federal funds rate at this particular meeting. However, the commentary from Fed Chair Jerome Powell following the meeting could provide clues about the central bank's plans for the coming months.

30-Year vs. 15-Year Fixed Mortgage Rates

A common question is whether to go with a 30-year or 15-year fixed mortgage. The main difference is the loan term: 30 years versus 15 years. Typically, 15-year mortgage rates are lower than 30-year rates. While the shorter term saves you money on interest in the long run, your monthly payments will be higher since you're paying off the same amount of money in half the time.

For example, on a $400,000 mortgage at today's rates:

- A 30-year mortgage at 6.57% would result in a monthly payment of around $2,547 (principal and interest). You'd pay about $516,817 in interest over the life of the loan.

- A 15-year mortgage at 6.01% would have a monthly payment of roughly $3,378 (principal and interest). You'd pay approximately $207,966 in interest over the life of the loan.

That's a huge difference in the total interest paid!

Fixed-Rate vs. Adjustable-Rate Mortgages

With a fixed-rate mortgage, your interest rate stays the same for the entire loan term, giving you predictable monthly payments. Adjustable-rate mortgages (ARMs), on the other hand, have an interest rate that is fixed for a certain period, after which it can adjust based on market conditions. For example, a 5/1 ARM has a fixed rate for the first five years, then adjusts annually.

While ARMs may start with lower rates than fixed-rate mortgages, they come with the risk that your rate could increase later on. With current ARM rates starting higher than fixed rates, they aren't as attractive an option as they used to be.

Recommended Read:

Mortgage Rates Trends as of March 17, 2025

Mortgage Rates Drop: Can You Finally Afford a $400,000 Home?

Expect High Mortgage Rates Until 2026: Fannie Mae's 2-Year Forecast

What Will Be Your Mortgage Payments Today Under Current Rates

Let's break down what your monthly mortgage payments might look like for different loan amounts at today's interest rates. I will use the prevailing 30-year fixed mortgage rate of 6.57% to give you a general idea. Remember, this calculation only includes principal and interest; property taxes, homeowner's insurance, and potential HOA fees will add to your total monthly payment.

Monthly Payment on a $150k Mortgage

For a $150,000 mortgage at a 6.57% interest rate, your estimated monthly payment would be approximately $954.50. This amount represents the portion of your payment that goes towards paying down the principal and covering the interest charges.

Monthly Payment on a $200k Mortgage

If you were to borrow $200,000 at a 6.57% interest rate, you can expect to pay around $1,272.66 per month. This figure is a good starting point for budgeting purposes, but don't forget about those extra costs I mentioned earlier!

Monthly Payment on a $300k Mortgage

Stepping up to a $300,000 mortgage at 6.57%, your estimated monthly payment jumps to $1,908.99. As you can see, even small increases in the loan amount can significantly impact your monthly expenses.

Monthly Payment on a $400k Mortgage

With a $400,000 mortgage at a 6.57% interest rate, your approximate monthly payment will be $2,545.32. At this level, it's even more important to carefully assess your financial situation and make sure you're comfortable with the commitment.

Monthly Payment on a $500k Mortgage

Finally, for a $500,000 mortgage at a 6.57% interest rate, you're looking at a monthly payment of roughly $3,181.65. This is a substantial amount, and it's essential to factor in all your other financial obligations before taking on such a large loan.

Remember, these are just estimates based on the principal and interest. I strongly recommend using a comprehensive mortgage calculator that includes taxes and insurance to get a more accurate picture of your potential monthly payments.

Looking Ahead: Will Mortgage Rates Drop in 2025?

Predicting the future of mortgage rates is always tricky. While most experts anticipate a gradual decline throughout 2025, dramatic drops are unlikely. Factors like the economy, inflation, and the Federal Reserve's actions will all play a role in determining where rates ultimately land. Experts believe that rates would need to drop closer to 5.5% to really stimulate the housing market. However, a weaker economy could offset the positive effects of lower rates.

In conclusion, today's mortgage rates are a mixed bag, with slight fluctuations in both purchase and refinance rates. The upcoming Federal Reserve meeting adds another layer of uncertainty. Keeping a close eye on economic news and consulting with a mortgage professional are always good ideas.

Work With Norada, Your Trusted Source for

Real Estate Investments

With mortgage rates fluctuating, investing in turnkey real estate

can help you secure consistent returns.

Expand your portfolio confidently, even in a shifting interest rate environment.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Read More:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Why Are Mortgage Rates Going Up in 2025: Will Rates Drop?

- Why Are Mortgage Rates So High and Predictions for 2025

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?