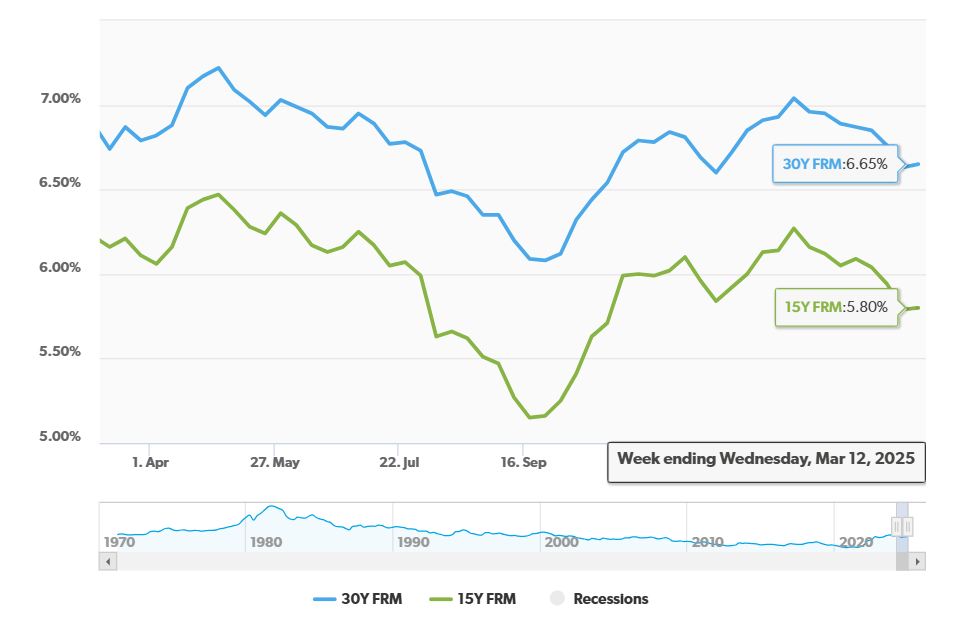

As of March 2025, mortgage rates remain near a 3-month low, hovering around 6.65% for a 30-year fixed mortgage, according to Freddie Mac. For many potential homebuyers, this presents a significant opportunity, and the answer is leaning towards yes, it might be a good time to lock in a rate now. Given the current market conditions and economic factors, now could be an opportune time to secure a rate before they potentially rise again.

I've been watching the housing market closely for years, and I can tell you that timing is everything. It’s not an exact science, but understanding the trends can give you a real edge.

Mortgage Rates Remain Near 3-Month Low: Should You Lock in Now?

Mortgage rates are a bit like the weather – they change constantly! Several key ingredients go into the mix that determines where they land:

- Inflation: When prices for goods and services rise (inflation), mortgage rates tend to follow suit. Lenders want to protect themselves against losing money, so they charge higher interest rates.

- Employment: A strong job market often leads to higher consumer confidence and spending. This can also push inflation upwards, ultimately affecting mortgage rates.

- Economic Stability: A stable economy usually results in more predictable mortgage rates. Uncertainty in the market can cause rates to fluctuate more wildly.

Freddie Mac's latest report shows the average rate for a 30-year fixed mortgage at 6.65%. While this is a slight increase from the previous week's 6.63%, it's still below the 6.74% we saw a year ago. It's pretty much flat. But what does this mean for you?

A Look Back: Where We've Been

To truly understand the current rates, it's important to take a quick trip down memory lane. 2024 was a tough year for the housing market. It was the slowest year since 1996! High rates and limited inventory made it difficult for buyers to find and afford homes. I remember talking to so many frustrated families who had to put their dreams on hold.

That's why this slight dip in rates feels so significant. Even a small decrease can make a big difference in your monthly payment and overall affordability.

Signs Pointing Towards a Buyer-Friendly Market

I'm seeing several shifts in the market that could be beneficial for those looking to buy:

- More Homes to Choose From: Inventory levels are rising, which means you have more options than you did last year. The competition for homes isn’t as fierce.

- Sellers are Lowering Prices: Sellers are starting to realize they can't ask for sky-high prices anymore. Price reductions are becoming more common, giving buyers more negotiating power.

- Spring is Blooming: The spring homebuying season is upon us. This is traditionally the busiest time of year for real estate, with more homes hitting the market and more buyers actively searching.

| Trend | Impact on Buyers |

|---|---|

| Increased Inventory | More choices, less competition |

| Price Reductions | Potential to find homes at lower prices |

| Spring Buying Season | Increased activity, more options available |

Thinking Beyond the 30-Year Fixed: The 15-Year Fixed Mortgage

While the 30-year fixed mortgage gets most of the attention, let's not forget about the 15-year fixed option. The average rate for a 15-year fixed mortgage is currently around 5.8%, a slight increase from 5.79% last week but still lower than the 6.16% from a year ago.

I personally love the 15-year option for those who can afford the higher monthly payments. You'll pay off your mortgage in half the time and save a ton on interest over the life of the loan.

Is Now the Right Time For You to Lock In?

This is the million-dollar question, isn't it? The answer isn't the same for everyone. You need to consider your unique situation:

- Are you Financially Ready?: Do you have a stable income and a good credit score? Can you comfortably afford the monthly payments at the current rate?

- How Long Do You Plan to Stay?: If you plan to stay in the home for a long time, securing a lower rate now could save you a significant amount of money.

- What are the Economic Winds Saying?: Keep an eye on economic indicators. If inflation is expected to rise, or if interest rates are forecasted to increase, locking in a rate now might be a smart move.

Recommended Read:

Mortgage Rates Drop: Can You Finally Afford a $400,000 Home?

Housing Demand Surges as Mortgage Rates Drop Significantly

Mortgage Rates Forecast March 2025: Will Rates Finally Drop?

Expect High Mortgage Rates Until 2026: Fannie Mae's 2-Year Forecast

Navigating the Lock-In Decision: A Deeper Dive

Okay, so you're thinking about locking in a mortgage rate. Here's a more in-depth look at some of the factors you should consider:

- Understanding Lock-In Agreements: Make sure you fully understand the terms of your lock-in agreement. How long is the rate locked for? What happens if the closing is delayed? Are there any fees involved?

- The Float-Down Option: Some lenders offer a “float-down” option, which allows you to take advantage of a lower rate if rates happen to decrease during your lock-in period. This can be a great perk, but make sure you understand the terms and any associated costs.

- Shop Around: Don't just settle for the first rate you're offered. Shop around and compare rates from multiple lenders. Even a small difference in the interest rate can save you thousands of dollars over the life of the loan. I have personally saved my clients thousands of dollars by just rate shopping.

- Get Pre-Approved: Getting pre-approved for a mortgage will give you a better idea of how much you can afford and will also strengthen your offer when you find the right home.

A Word of Caution: Don't Try to Time the Market Perfectly

I've seen so many people try to time the market perfectly, and they almost always end up missing out on opportunities. Trying to predict the future is a fool's errand. Focus on what you can control: your finances, your credit score, and your research.

My Personal Take: Act Now, But Do Your Homework

In my opinion, with rates hovering near a three-month low and the housing market showing signs of shifting in favor of buyers, now is a good time to seriously consider locking in a mortgage rate.

However, don't rush into anything. Take your time, do your research, and consult with a qualified mortgage professional. This is a big decision, so make sure you're making the right one for you and your family.

- Consult a Pro: Talking to a mortgage broker or financial advisor can provide personalized advice.

- Review Your Credit: A better credit score can get you a better rate.

- Calculate All Costs: Don’t forget to factor in closing costs, property taxes, and insurance.

In Conclusion: Seize the Opportunity

The housing market is a dynamic beast, and it can be difficult to predict what will happen next. But right now, the conditions seem favorable for buyers. Mortgage rates are relatively low, inventory is improving, and sellers are becoming more willing to negotiate. If you're ready to buy, now might be the time to take the plunge.

Remember to assess your finances, consider your long-term plans, and stay informed about market trends. By doing your homework and making a well-informed decision, you can seize this opportunity and achieve your dream of homeownership.

Work With Norada, Your Trusted Source for

Real Estate Investments

With mortgage rates fluctuating, investing in turnkey real estate

can help you secure consistent returns.

Expand your portfolio confidently, even in a shifting interest rate environment.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Recommended Read:

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Why Are Mortgage Rates Going Up in 2025: Will Rates Drop?

- Why Are Mortgage Rates So High and Predictions for 2025

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?