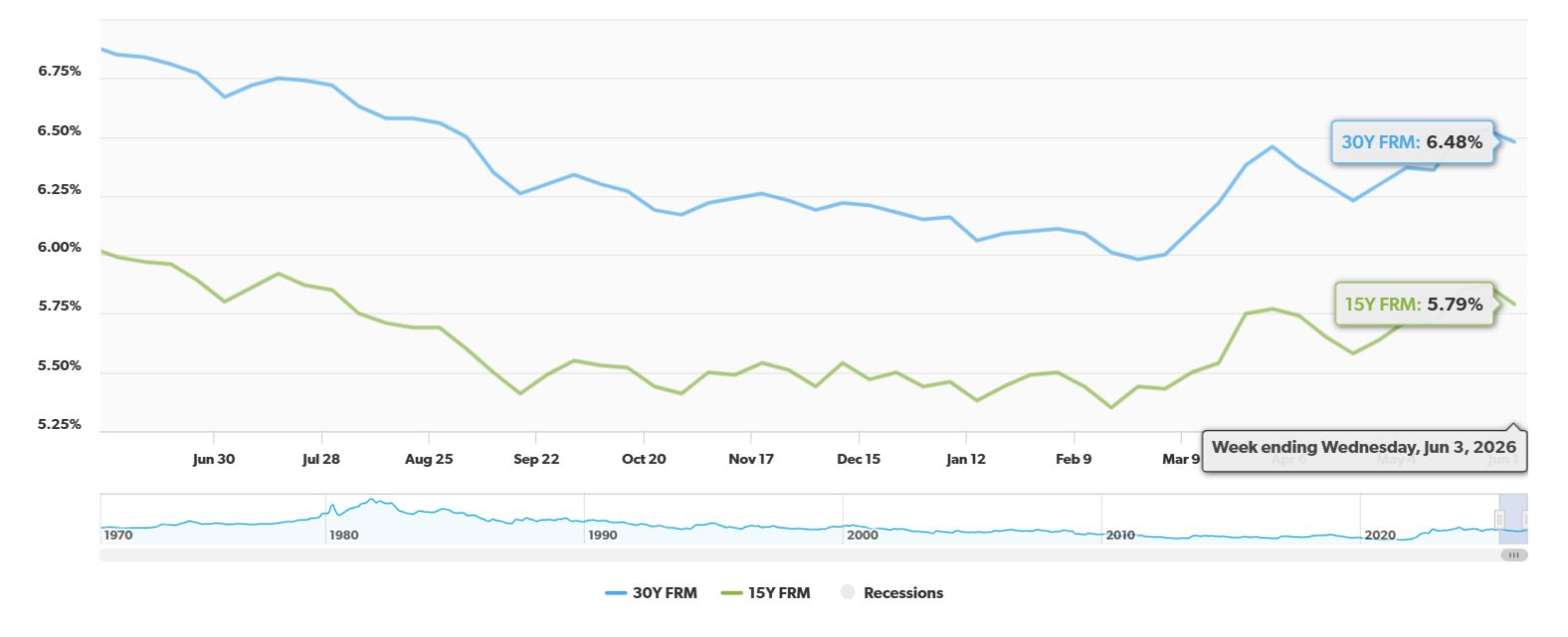

The latest numbers from Freddie Mac are certainly encouraging for anyone dreaming of homeownership. For the week ending June 4, 2026, the average rate for a 30-year fixed mortgage landed at 6.48%. This is a significant 37 basis point drop from where we were a year ago. And looking at the most immediate data, that rate also saw a slight dip of 0.05% just in the last week.

This combination of year-over-year and weekly improvement is more than just a number; it’s a tangible boost to affordability for many potential homeowners. This dip, while perhaps not a dramatic plunge, is a welcome breath of fresh air. It’s the kind of movement that can tip the scales for someone who’s been on the fence, or help make a move possible for those who thought they couldn't afford it.

30-Year Fixed Mortgage Rate is Down by 37 Basis Points Year-Over-Year

What Does This Rate Drop Really Mean for You?

Let’s break down what this 37 basis point (which is the same as 0.37%) drop actually signifies. Freddie Mac's Primary Mortgage Market Survey (PMMS) is the gold standard for tracking these rates, and their data shows that the average 30-year fixed-rate mortgage was at 6.85% for the same week in 2025. Fast forward a year, and we're now at 6.48%.

On the surface, that might not seem like a huge difference, but when you're talking about a loan that lasts 30 years, even small percentage points add up. My experience tells me that people often underestimate the power of these seemingly minor rate changes, especially when considering the long-term financial impact.

Calculating the Savings: A Look at the Numbers

To really understand the impact, let's look at a common scenario. Imagine you're taking out a $400,000 mortgage.

- Last Year (at 6.85%): Your monthly principal and interest payment would have been approximately $2,621.04.

- This Year (at 6.48%): Your monthly payment drops to about $2,523.01.

That's a saving of nearly $98.03 per month. Now, $98 might not sound like life-changing money on its own, but over the course of a 30-year loan, that adds up to a staggering $35,290.80 in total savings on interest alone! That’s a significant chunk of change that can go towards other financial goals, home improvements, or simply provide a little more breathing room in your budget.

Here's a table showing how this savings plays out for different loan amounts:

| Home Loan Amount | 2025 Payment (6.85%) | 2026 Payment (6.48%) | Monthly Savings | 30-Year Lifetime Savings |

|---|---|---|---|---|

| $300,000 | $1,965.78 | $1,892.26 | $73.52 | $26,467.20 |

| $400,000 | $2,621.04 | $2,523.01 | $98.03 | $35,290.80 |

| $500,000 | $3,276.30 | $3,153.77 | $122.53 | $44,110.80 |

As you can see, the larger your loan, the more significant the savings become.

Beyond the 30-Year Fixed: Other Rates to Consider

While the 30-year fixed is the most popular for its predictable payments, it's worth noting how other mortgage products are performing. The 15-year fixed-rate mortgage, a great option for those looking to pay off their home faster and save more on interest, has also seen a dip. For the week ending June 4, 2026, it averaged 5.79%, down from 5.87% the previous week. Year-over-year, this is a 20 basis point decrease from 5.99% in 2025.

Here’s a quick snapshot from Freddie Mac:

| Mortgage Type | Week Ending 06/04/2026 | Previous Week | Year-over-Year Change |

|---|---|---|---|

| 30-Yr FRM | 6.48% | 6.53% | -0.37% |

| 15-Yr FRM | 5.79% | 5.87% | -0.20% |

This tells me that the broader trend is one of moderating interest rates, which is generally positive for the housing market.

Why Are Rates Moving Down? The Economic Picture

According to Sam Khater, Chief Economist at Freddie Mac, this slight drop into the mid-6% range is offering some much-needed breathing room for homebuyers. He points out that national income growth is currently outpacing home price appreciation. This is a critical factor for affordability. When your paycheck grows faster than the cost of the house, it makes buying a home feel more achievable.

It’s not just Freddie Mac's numbers telling this story. Broader affordability indexes, like the First American Real House Price Index (RHPI), are also showing that these lower year-over-year rates are contributing to modest affordability gains in major U.S. cities. This suggests a more widespread, albeit gradual, improvement in the housing market's accessibility.

Looking ahead, forecasts from organizations like the Mortgage Bankers Association (MBA) suggest that these 30-year rates are likely to fluctuate between 6.1% and 6.3% for the rest of 2026. This prediction is based on the expectation that inflation pressures will continue to stabilize, which is a good sign for borrowers.

My Take: A Balanced Outlook for Buyers

From my perspective, this is a really encouraging development for anyone considering buying a home. The combination of slightly lower mortgage rates and rising incomes creates a more favorable environment than we've seen in some time. It’s important to remember that the housing market is complex, and many factors influence prices and rates. However, this move downwards in mortgage rates is a significant positive signal.

It's not a time for wild speculation, but rather a moment for thoughtful consideration. If you've been waiting for a better opportunity to enter the housing market, now might be the time to start seriously exploring your options. Getting pre-approved for a mortgage and speaking with a trusted real estate agent can give you a clearer picture of what you can afford in today's market.

The fact that rates have decreased by 37 basis points year-over-year on the 30-year fixed mortgage is a clear indication that the market is responding to economic conditions in a way that benefits borrowers. It’s a gentle nudge in the right direction, making that dream home feel a little closer and a lot more affordable.

VS

Out‑of‑State investors can compare Indiana’s affordable rental with higher cap rate vs Florida’s newer A+ property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?