Are mortgage rates headed down to the magical 5% mark by 2026? While some experts are hinting at a brief dip into the high 5% range, it's highly unlikely we'll see average 30-year fixed mortgage rates consistently below 5% in 2026, with most forecasts pointing to rates hovering between 6% and 6.4% for much of the year.

Will Mortgage Rates Drop to 5% in 2026? What the Experts Say

It's the question on so many aspiring and current homeowners' minds: will mortgage rates finally dip to a more comfortable 5% by 2026? As someone who’s been following housing market trends for years, I can tell you it’s a complex picture, and a clear-cut “yes” or “no” is tough to give. However, based on what I'm seeing and the data from major financial institutions, a sustained drop below 5% in 2026 is highly improbable.

2026 Mortgage Rate Forecasts: A Look at the Numbers

To get a clearer picture, let's break down what some leading institutions are predicting for 2026. As of February 19, 2026, the average 30-year fixed mortgage rate is already sitting around 6.01%, which gives us a good starting point.

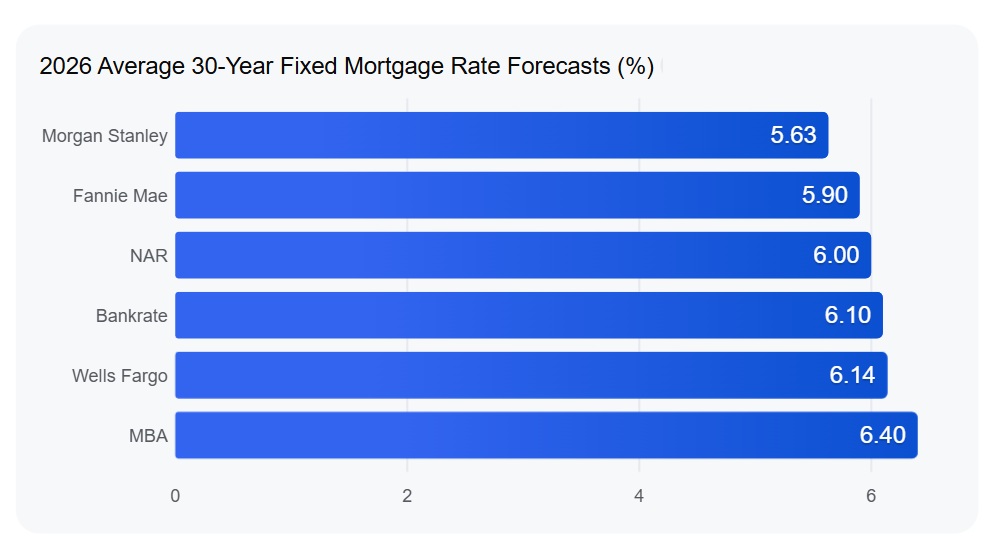

Here's a snapshot of what various experts are forecasting for 2026:

| Institution | 2026 Forecast (Annual Average/Year-End) | Timing/Type |

|---|---|---|

| Morgan Stanley | 5.50% – 5.75% | Projected mid-year low |

| Fannie Mae | 5.90% | Year-end 2026 |

| National Assoc. of Realtors | 6.00% | 2026 annual average |

| Bankrate | 6.10% | 2026 annual average |

| Wells Fargo | 6.14% | 2026 annual average |

| Mortgage Bankers Association | 6.40% | 2026 annual average |

As you can see, the most optimistic outlook from Morgan Stanley suggests a potential low point in the mid-5% range. However, the majority of forecasts cluster between 5.90% and 6.40% for the year. This tells me that going significantly below 5% is not what most seasoned financial minds are betting on.

Key Factors Shaping 2026 Mortgage Rates

So, what’s driving these predictions? It boils down to a few major economic forces that I’m keeping a very close eye on:

- Economic Softening: The biggest factor that could push rates lower is a slowdown in the economy. If the job market cools down and inflation continues to ease towards the Federal Reserve's 2% target, the Fed might feel more confident easing up on interest rates.

- Federal Reserve Policy: The Fed doesn't directly control mortgage rates, but their actions have a huge ripple effect. If they start cutting their benchmark interest rates in 2026, it usually puts downward pressure on the yields of 10-year Treasury notes. Mortgage rates tend to follow these Treasury yields quite closely.

- Mortgage-Backed Securities (MBS) Purchases: There have been some discussions about the government potentially buying mortgage-backed securities. If this were to happen on a large scale, it could help bring mortgage rates down, as we've already seen some early signs of this influencing rates in early 2026.

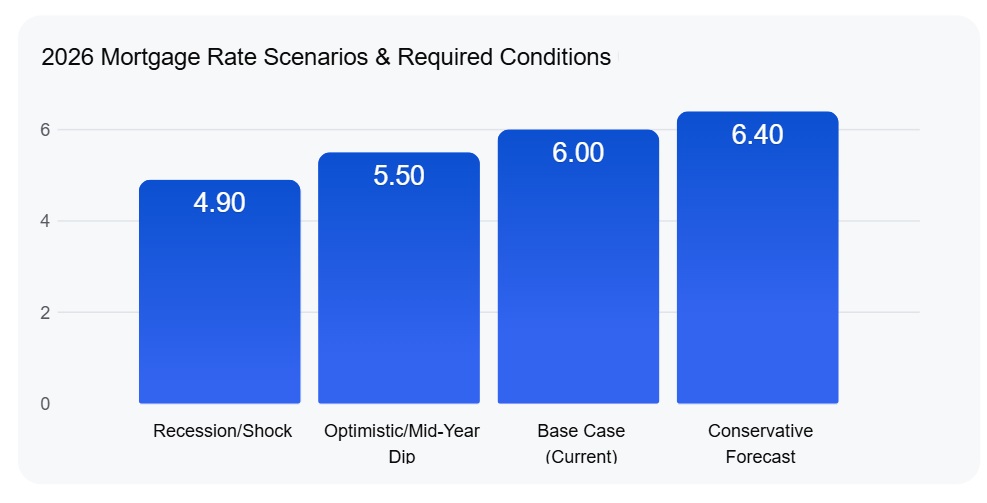

What Would It Take for Rates to Dive Below 5%?

For mortgage rates to truly plummet to below 5% in 2026, we'd likely need to see some pretty dramatic economic events occur. It’s not just a matter of inflation cooling slightly; we’d probably need a full-blown recession or a significant economic shock.

Here are the kinds of things that might push rates below that 5% threshold:

- Serious Labor Market Weakness: If unemployment numbers start to climb significantly, or if there's widespread fear of a recession, the Federal Reserve would likely be forced to cut interest rates much more aggressively than they are currently planning.

- Inflation Falling Sharply and Staying Low: For rates to drop into the 4% range, inflation would probably need to fall to pre-COVID levels and stay there consistently. That’s a tall order given current global economic conditions.

- A Big Drop in 10-Year Treasury Yields: Since mortgage rates are so closely tied to the 10-year Treasury yield, that benchmark would need to fall well below 3.5%. This usually happens when investors are seeking safety.

- Massive Government Intervention: Think large-scale, sustained purchases of mortgage-backed securities by the government or the Fed. This could artificially push rates down, but it's a strong intervention.

- A “Flight to Safety”: If there were a major global crisis or a huge stock market crash, investors often rush to buy bonds. This increased demand for bonds drives their yields down, which in turn can lower mortgage rates.

What's Holding Rates Up?

Even with some potential for rates to dip, several factors are preventing them from falling much further:

- Sticky Inflation: While inflation has cooled, any unexpected jump in consumer prices can quickly push mortgage rates back up. It's like trying to squeeze toothpaste back into the tube – once it's out, it's hard to control perfectly.

- Resilient Economy: If the economy continues to chug along or even show surprising strength, the Fed might hesitate to cut rates, or even consider raising them again.

- Government Borrowing: The government’s need to borrow money to fund its operations and manage the national debt can put upward pressure on long-term bond yields, which keeps mortgage rates from dropping too low.

The “Lock-In Effect”

It's also important to remember the “lock-in effect.” A massive number of homeowners refinanced or bought homes when rates were historically low. Now, with rates significantly higher, many are hesitant to sell or move because they don't want to give up their super-low existing mortgage rate. Estimates suggest that as many as 4 out of 5 homeowners have rates below 6%. This means even if rates dropped to 5.5%, a lot of people would still be reluctant to refinance, which can impact the overall demand and supply dynamics in the housing market.

My Take on the 5% Mark in 2026

From my perspective, while a brief dip into the high 5% range by mid-2026 is certainly within the realm of possibility, a sustained average rate below 5% seems like a long shot. The conditions required for such a drastic drop – a significant recession, inflation crashing below 2%, or massive, sustained government intervention – are not what most forecasts are predicting.

What I believe is more likely is a range between 5.5% and 6.4%, with the actual rate on any given day influenced by the ever-changing economic news. If you’re looking to buy or refinance, my advice is always to focus on what you can afford with current rates, keep a close eye on economic indicators, and be ready to act if rates move in a favorable direction. Don't pin all your hopes on the magical 5% mark appearing consistently in 2026; it’s a very optimistic scenario.

And

Alabama’s newer A- rental vs Tennessee’s larger property with higher NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?