It might feel like mortgage rates are playing a game of statues lately, barely budging from week to week. However, if you're looking to buy a home, there's some good news: the popular 30-year fixed mortgage rate is actually down by 23 basis points compared to this time last year. While the number might not seem huge, that difference can add up to real savings in your monthly payments and over the life of your loan.

30-Year Fixed Mortgage Rate Drops by 23 Basis Points Year-Over-Year

As your friendly neighborhood real estate enthusiast and observer of all things housing, I've been keeping a close eye on these numbers. It’s easy to get caught up in the day-to-day chatter about rates ticking up or down a hair, but the bigger picture often tells a more interesting story. And right now, that bigger picture shows us rates are holding steady in the mid-6% range, which, while higher than many would ideally want, is still a welcome improvement from where we were a year ago.

Mortgage Rates: Staying Put, But A Little Cheaper Than Last Year

Let's break down what the latest numbers from Freddie Mac, a big player in the mortgage market, are telling us. They conduct a survey every week to see what the average mortgage rates are.

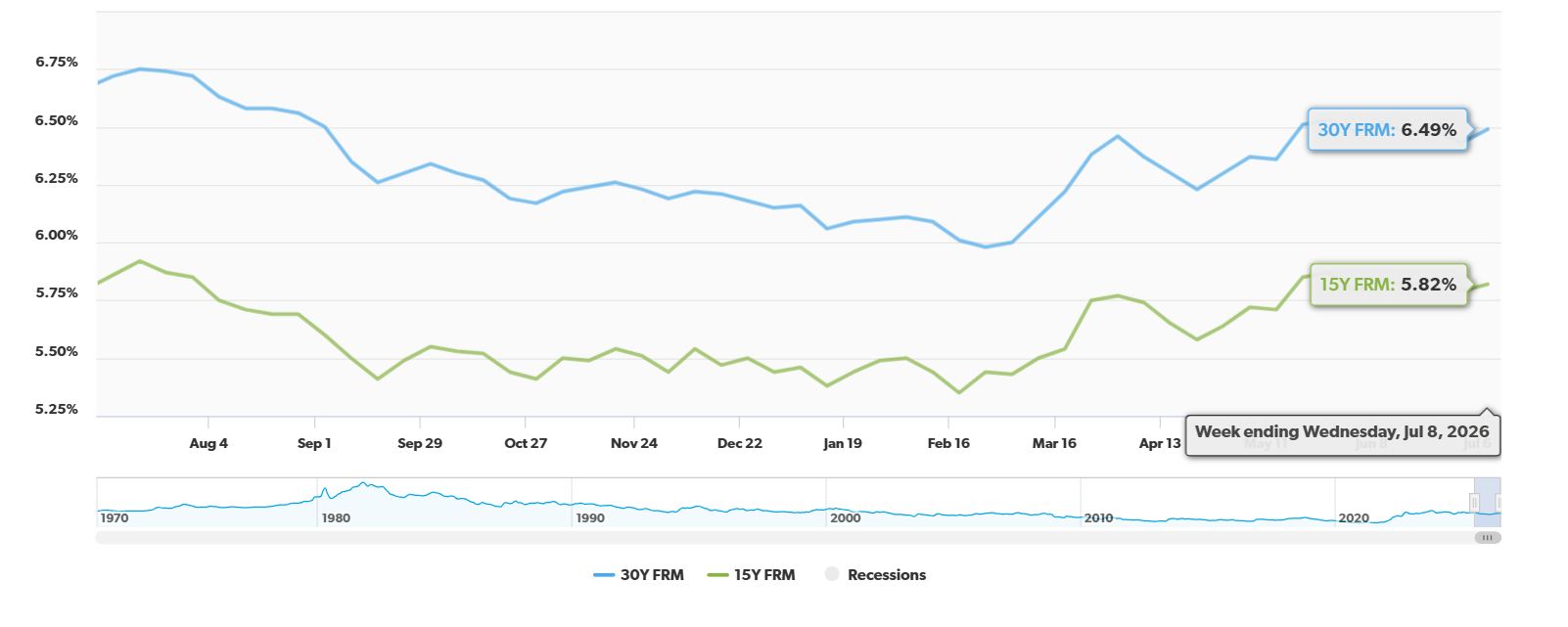

For the week ending July 9, 2026, the average rate for a 30-year fixed mortgage landed at 6.49%. Now, that’s a tiny bit higher than the week before (6.43%), but the really important part is looking back a whole year. This time last year, that same 30-year fixed mortgage was averaging a higher 6.72%. That difference of 0.23%, or 23 basis points, is significant.

It's not just the 30-year fixed rate that's behaving similarly. The 15-year fixed-rate mortgage is also showing this trend. It’s currently averaging 5.82%, slightly up from 5.79% last week, but down a smidge from 5.86% a year ago.

Here’s a quick look at how things have shaken out, according to Freddie Mac's latest Primary Mortgage Market Survey:

| Mortgage Type | Current Average (July 9, 2026) | Change from Previous Week | Change from Year Ago |

|---|---|---|---|

| 30-Year Fixed-Rate Mortgage | 6.49% | +0.06% | -0.23% |

| 15-Year Fixed-Rate Mortgage | 5.82% | +0.03% | -0.04% |

Why Aren't Rates Moving Much?

It’s a good question! When we see rates sitting relatively still, it’s often because there are opposing forces at play. Think of it like a tug-of-war.

One of the biggest things that influences mortgage rates is the 10-year Treasury yield. Right now, that yield is hovering around 4.58%. Why is that important? Well, mortgage lenders often use Treasury yields as a benchmark when setting their own rates. When Treasury yields climb, mortgage rates tend to follow suit, and when they fall, mortgage rates often do too. Geopolitical happenings and worries about prices going up (inflation) are pushing those Treasury yields higher, which puts upward pressure on mortgage rates.

However, on the flip side, we're seeing some signs of economic stability. According to Freddie Mac's Chief Economist, Sam Khater, while rates aren’t as low as buyers might dream of, the economy is growing, and that’s helping to keep things more balanced. When the economy is doing okay, it can temper some of the extreme movements in interest rates. It's a delicate balance, and right now, it seems to be leaning towards stability, keeping those mortgage rates in their current neighborhood.

What Does This Mean for You?

Even though the week-to-week changes are small, that year-over-year decrease in the 30-year fixed rate is definitely something to celebrate if you're in the market for a home. Let’s imagine what that saving looks like.

Suppose you're buying a $400,000 home and putting down 20%, so you're financing $320,000.

- At 6.72% (last year's rate): Your monthly principal and interest payment would be around $2,072.

- At 6.49% (this year's rate): Your monthly principal and interest payment is around $2,016.

That's a savings of $56 per month! Over 30 years, that adds up to over $20,000. That’s a pretty nice chunk of change that could go towards other things, like furniture for your new home, saving for retirement, or even just enjoying life a little more.

Even though rates are still above 6%, the fact that they’ve dipped from last year is a win for potential buyers. It means a bit more breathing room in the budget.

Looking Ahead: What Do the Experts Predict?

So, what's the crystal ball telling us about the future? Well, most of the smart folks who study the housing market, like those at Fannie Mae and the Mortgage Bankers Association, are predicting that the 30-year fixed rate will likely stay put between 6.3% and 6.5% for the rest of 2026.

This suggests that we shouldn't expect wild swings in mortgage rates in the immediate future. It’s more of a “steady as she goes” situation for now. This stability can actually be a good thing for buyers because it makes it easier to plan and budget for a home purchase without constantly worrying about rates jumping or plummeting.

My Take on the Market

From where I stand, watching the housing market and helping people navigate it, this period of stability, even with rates above 6%, is a sign of a more mature market. It’s not the frenzy we saw a few years back, and it’s not the deep freeze of a recession. It's a more balanced environment.

The fact that the 30-year fixed rate is down year-over-year is a gentle nudge of encouragement for those who have been waiting. It means that while affordability is still a concern for many, there's a slight easing of that pressure compared to last year.

I always tell people to focus on what they can control: their credit score, their down payment, and their overall financial health. Even a small improvement in your credit score can sometimes lead to a slightly better rate, and that extra bit of savings can make a big difference.

It's also important to remember that these are averages. Your personal mortgage rate will depend on many factors, including your creditworthiness, the loan amount, and the lender you choose. Shopping around and getting quotes from multiple lenders is always a smart move.

So, while the headlines might shout about minor weekly fluctuations, take comfort in the fact that the 30-year fixed mortgage rate is offering a bit of relief compared to last year. It’s a good time to reassess your homeownership goals and see if this slightly more favorable rate environment aligns with your plans.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?