The California housing market is showing signs of life again! After some ups and downs, more homes are being sold, and while prices are still high, they aren't climbing as fast as before. For folks wondering if now is a good time to buy or sell, or just curious about what the future holds, understanding these current trends is super important for making smart choices.

For a long time, it felt like buying a house in California was a distant dream for many. Prices kept climbing, and it was hard for regular families to even get a foot in the door. But recently, things have started to shift a little, and that's what I want to talk about. I've been looking at the reports from the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.), and they’ve given us a good picture of what’s going on. It's like the housing market is taking a deep breath.

California Housing Market Trends: What's Happening Now?

Home Sales Pick Up the Pace

Let’s get down to it. In June 2026, something neat happened: more homes were sold compared to the months before. This is a big deal! It means people are feeling more confident and are willing to jump into the market, even with interest rates still a bit higher than we’d all like.

- June 2026 saw a rebound in home sales. Specifically, the sale of existing, single-family homes hit a seasonally adjusted annualized rate of 279,880.

- This is a jump of 4.1 percent from May 2026.

- Even better, it's a 6.0 percent increase compared to June of last year (June 2025).

This is the third month in a row that sales have gone up when we compare it to the same time last year. It’s the biggest jump we've seen in quite a while! It tells me that even though it’s not as easy as it used to be, people are still finding ways to make their homeownership dreams happen.

Home Prices are Calming Down (a Little!)

Now, about those prices. Remember when the median home price in California hit a record high of $930,260 in May 2026? Well, it’s come down a bit. In June, the statewide median home price was $904,640.

- That’s a drop of 2.8 percent from May.

- But, it's still a little higher, up 0.4 percent, than it was in June 2025.

So, while prices aren't falling off a cliff, they're not shooting up at the same crazy speed anymore. This is good news for buyers who have been priced out. It means the market is starting to find a more stable spot. It’s not like prices are cheap, but it's a step in the right direction for many.

Why is This Happening? Let's Break it Down.

I think there are a few reasons why we're seeing these trends.

- Buyers are Adjusting: People are getting used to the current interest rate environment. They might not love it, but they're figuring out how to work with it.

- Inventory is Still Tight, But Improving: Even though fewer people are selling their homes (more on that later!), the number of homes available is still growing a little. When there are more homes to choose from, it can help balance things out.

- A Mix of Homes Selling: It’s interesting to note that the entry-level and mid-tier homes are seeing more sales. This is different from earlier when it felt like only the super-expensive homes were moving. This means more regular folks are finding homes.

Regional Differences: Not All Areas are the Same

It's super important to remember that California is a huge state, and what's happening in one place might be different somewhere else. The C.A.R. report shows us this clearly:

| Region | June 2026 Median Price | Sales YTY % Change |

|---|---|---|

| Far North | $405,000 | +23.3% |

| Central Valley | $514,800 | +13.8% |

| Southern California | $900,000 | +10.8% |

| San Francisco Bay Area | $1,400,000 | +7.8% |

| Central Coast | $1,110,000 | +4.2% |

As you can see, the Far North and Central Valley are seeing huge jumps in sales, probably because prices are more affordable there. Even the San Francisco Bay Area, known for its super high prices, saw sales increase! This shows that demand is pretty strong across the board, even if prices are very different.

California Housing Market Forecast: What to Expect in 2026

The California housing market is poised for a gentle upturn in 2026, with home sales and the median price expected to inch up slightly. According to the CALIFORNIA ASSOCIATION OF REALTORS® (C.A.R.), we can anticipate existing single-family home sales to reach around 274,400 units, a 2% increase from 2025. The median home price is projected to hit a new record, climbing 3.6% to $905,000. While this might sound like a straightforward prediction, dig a little deeper, and you'll find a more nuanced picture shaped by economic shifts, interest rates, and a slowly improving affordability situation.

My Take on the 2026 Outlook

As someone who's been following the California real estate scene for a while, I can tell you that “inching up” feels like a pretty accurate description. We've seen some wild swings in the past, and frankly, a period of relative stability is what many buyers and sellers are hoping for. C.A.R.'s forecast suggests that stability is on the horizon, but it's not going to be a free-for-all. Affordability is still a major hurdle, but there are glimmers of hope.

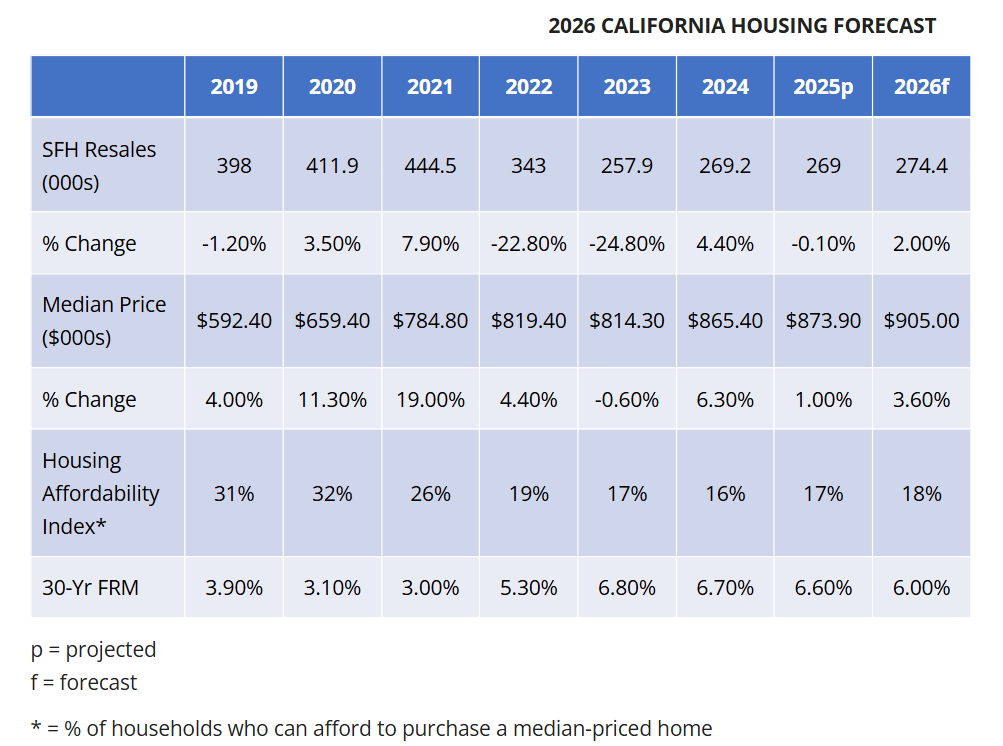

A Look at C.A.R.'s Projections

Let's break down what C.A.R. is predicting for the coming years:

| Year | SFH Resales (000s) | % Change | Median Price ($) | % Change | Housing Affordability Index (%) | 30-Yr FRM (%) |

|---|---|---|---|---|---|---|

| 2024 | 269.2 | 4.40% | $865,400 | 6.30% | 16% | 6.70% |

| 2025p | 269.0 | -0.10% | $873,900 | 1.00% | 17% | 6.60% |

| 2026f | 274.4 | 2.00% | $905,000 | 3.60% | 18% | 6.00% |

p = projected, f = forecast

As you can see, 2025 is looking like a bit of a holding pattern, with sales essentially flat compared to 2024. However, the median price is still expected to tick up slightly. The real movement, according to this forecast, is in 2026, where we see both sales and prices showing more noticeable, albeit still moderate, growth.

Why the Gentle Climb?

Several factors are expected to contribute to this gradual ascent:

- Interest Rates Cooling Down: This is a big one. C.A.R. forecasts the average 30-year fixed mortgage rate to drop to 6.0% in 2026. This is a significant improvement from the averages seen in recent years and even the 6.6% projected for 2025. Lower mortgage rates mean more buying power for consumers. Even though it's still higher than pre-pandemic levels, it's a move in the right direction and, importantly, lower than the 50-year historical average of nearly 8%.

- Slightly Better Affordability: With lower interest rates and potentially moderate price gains, housing affordability is predicted to inch up. The index is expected to reach 18% in 2026, meaning 18% of households will be able to afford to buy a median-priced home. This is a small but welcome improvement from 16% in 2024 and 17% in 2025. For many Californians, this slight shift could make the dream of homeownership feel a bit more attainable.

- Increasing Inventory: The forecast indicates that housing supply will continue to improve, with active listings potentially rising by nearly 10% in 2026. When more homes are available, it can ease some of the intense competition we've seen in the market. This could give buyers a bit more breathing room and potentially moderate intense bidding wars.

What About the Economy?

The housing market doesn't exist in a vacuum. The broader economic picture plays a crucial role.

- Slowing GDP Growth: The U.S. gross domestic product (GDP) is expected to grow at a slower pace in 2026, around 1%, after a projected 1.3% in 2025.

- Job Growth and Unemployment: California's nonfarm job growth is also projected to slow down, with a 0.3% increase in 2026 after a 0.4% rise in 2025. Consequently, the unemployment rate is expected to creep up to 5.8% in 2026 from 5.6% in 2025 and 5.3% in 2024. While a slight increase in unemployment can be concerning, these numbers suggest the job market, while cooling, isn't collapsing.

C.A.R. President Heather Ozur points out that as economic uncertainty begins to clear and mortgage rates decline, housing sentiment should improve. This is a key piece of the puzzle – people are more likely to make big financial decisions like buying a home when they feel more secure about their jobs and the economy.

Potential Roadblocks and Challenges

It wouldn't be wise to paint an entirely rosy picture. The forecast also highlights several challenges that could still impact the market:

- Inflation: Inflation is likely to pick up, with the annual average Consumer Price Index (CPI) expected to reach 3.0% in 2026, up from 2.8% in 2025. Higher inflation can erode purchasing power and impact what people can afford.

- Home Insurance Crisis: The ongoing issues with homeowners insurance in California are a significant concern. Rising premiums and reduced availability of coverage can make homeownership more expensive and less attractive, especially in fire-prone areas.

- Trade Tensions: Lingering trade tensions between the U.S. and its trading partners can create economic uncertainty, which can ripple through the housing market.

- Stock Market Volatility: A potential stock market bubble could burst, leading to financial instability and affecting the confidence of high-net-worth individuals who are often significant players in luxury real estate markets.

Senior Vice President and Chief Economist Jordan Levine notes that despite these headwinds, the improving lending environment and clearing economic clouds will be key drivers.

What This Means for You

So, what does all this forecast talk mean for you, whether you're looking to buy, sell, or just keep an eye on your investments?

- For Buyers: The forecast offers a glimmer of hope. Lower interest rates and a slight increase in inventory in 2026 could make it a more favorable year for buyers than the preceding ones. However, affordability remains a challenge, so smart financial planning and patience will still be crucial. Don't expect a crash, but rather a market that might be slightly less of a seller's dominance.

- For Sellers: If you've been holding off, 2026 might present a more opportune time to list your home. With stabilizing prices and rising demand, you could see your property fetch a good price. However, the days of astronomical offers might be behind us, and a more realistic pricing strategy will be important.

- For Homeowners: If you own a home in California, the moderate price appreciation suggests that your home equity is likely to continue growing, albeit at a steadier pace than in boom years.

My personal feeling is that California's housing market, given its fundamental strengths in desirability and economic output, will continue to be resilient. The forecast for 2026 suggests a return to a more sustainable growth pattern. It's not a market for speculators looking for quick flips, but for those looking for long-term value and a place to call home, opportunities will likely emerge.

The key takeaway from C.A.R.'s 2026 California Housing Market Forecast is that we're looking at a period of gradual improvement. Sales and prices are projected to rise modestly, driven by falling interest rates and slightly better affordability, while still navigating economic uncertainties and persistent challenges like insurance costs. It's a market that demands a well-informed approach, but one that holds promise for those looking to enter or move within it.

Turnkey real estate delivers immediate cash flow from day one and builds wealth for decades ahead.

Norada Real Estate helps you secure such properties—so your investment pays today and continues to grow for years to come.

Related Articles:

- California Housing Market Predictions 2025

- The Great Recession and California's Housing Market Crash: A Retrospective

- California Housing Market Cools Down: Is it a Buyer's Market Yet?

- California Dominates Housing With 7 of Top 10 Priciest Markets

- Real Estate Forecast Next 5 Years California: Boom or Crash?

- Anaheim, California Joins Trillion-Dollar Club of Housing Markets

- California Housing Market: Nearly $174,000 Needed to Buy a Home

- Most Expensive Housing Markets in California

- Abandoned Houses for Free California: Can You Own Them?

- California Housing in High Demand: 19 Golden State Cities Sizzle

- Homes Under 50k in California: Where to Find Them?

- Will the California Housing Market Crash in 2024?

- Will the US Housing Market Crash?

- California Housing Market Crash: Is a Correction Coming Up?