The mortgage rates today, Jan 14, have seen a significant drop, with the 30-year fixed refinance rate plunging by 18 basis points. This means that for many, a golden opportunity to lower their monthly payments has just opened up. According to Zillow, the national average for a 30-year fixed refinance rate has fallen from last week's average of 6.51% down to 6.33% as of Wednesday. This isn't just a small blip; it's a notable shift that could put real dollars back into your pocket.

Mortgage Rates Today, Jan 14: 30-Year Refinance Rate Drops by 18 Basis Points

What Exactly Does a 18 Basis Point Drop Mean for You?

You might be wondering what a “basis point” even is, and more importantly, what this 18 basis point drop actually translates to in terms of real savings. Think of it this way: a basis point is one-hundredth of a percentage point. So, an 18 basis point drop means the interest rate on your mortgage has decreased by 0.18%.

Let's break it down with an example. Imagine you have a mortgage balance of $300,000.

- At 6.51% interest, your monthly principal and interest payment would be approximately $1,895.

- At the new rate of 6.33% interest, your monthly principal and interest payment drops to about $1,864.

While $31 per month might not sound enormous at first glance, over the life of a 30-year mortgage, that adds up. Over 30 years (360 payments), that’s a saving of over $11,000! This is why even small rate drops can be incredibly impactful, especially for those with larger loan amounts. It's not just about saving a few dollars a month; it's about significantly reducing the total interest paid over the coming years.

A Deeper Dive into Today's Mortgage Rate Movements

The 30-year fixed refinance rate isn't the only area seeing positive movement. Zillow also reported that the 15-year fixed refinance rate saw a decrease of 12 basis points, moving from 5.50% down to 5.38%. This is excellent news for those looking to pay off their mortgage faster and reduce their overall interest costs.

And for those considering adjustable-rate mortgages (ARMs), the 5-year ARM refinance rate is currently holding steady at 7.27%. While ARMs can offer lower initial rates, it's crucial to understand their structure and potential for future increases.

Here’s a quick look at the current refinance rates:

| Loan Type | Rate (Today, Jan 14) | Rate (Previous Week) | Change (Basis Points) |

|---|---|---|---|

| 30-Year Fixed Refi | 6.33% | 6.51% | -18 |

| 15-Year Fixed Refi | 5.38% | 5.50% | -12 |

| 5-Year ARM Refi | 7.27% | N/A | N/A |

Data provided by Zillow.

The Refinance Strategy: 30-Year Fixed vs. 15-Year Fixed

Choosing between a 30-year and a 15-year fixed refinance is a critical decision, and it really depends on your personal financial goals and current situation. In my experience, there’s no one-size-fits-all answer, but understanding the trade-offs is key.

The 30-Year Fixed Refinance:

- Pros: Lower monthly payments. This is the biggest draw. By spreading your loan over a longer term, you reduce the immediate financial burden, freeing up cash flow for other expenses, savings, or investments. This is especially beneficial if you're looking to consolidate debt or if your income fluctuates.

- Cons: You’ll pay significantly more in interest over the life of the loan compared to a 15-year term. The total cost of your home will be higher.

The 15-Year Fixed Refinance:

- Pros: Substantially lower interest rate and you’ll pay off your mortgage much faster (in half the time!). This means you'll build equity in your home quicker and pay considerably less in total interest.

- Cons: Monthly payments will be higher. You need to ensure your budget can comfortably accommodate these larger payments.

My take? If the current 15-year fixed rate (5.38%) is well within your budget with room to spare, and you’re focused on long-term savings and paying off your home sooner, that’s often the mathematically superior choice. However, if your priority is to lower your monthly expenses and improve your immediate cash flow, while still securing a much better rate than you might have had last year, the 30-year fixed option at 6.33% is a fantastic move. It’s about finding the balance that works for your financial life right now.

Mortgage Refinance Market Demand: A Surge in Activity

This recent drop in rates hasn’t gone unnoticed by the market. We're seeing a clear shift from a typical holiday slowdown into a period of heightened activity. The news that the administration would order mortgage giants to purchase billions in mortgage-backed bonds has acted as a significant catalyst.

- Surge in Applications: Refinance applications jumped by an impressive 40% last week. This is a direct response to the falling rates and the positive sentiment they’ve generated.

- Annual Growth: The demand for refinancing is currently 128% higher than in the same week last year. This indicates that many homeowners who secured loans at rates above 7% in the past year are now finding a viable “refinance window” to reduce their payments. It’s a smart move to capitalize on favorable market conditions.

- Larger Loan Focus: Interestingly, it appears that borrowers with larger loan sizes have been the most responsive to these rate drops. They’re leading the spike in application volume, likely because the savings on larger mortgages are more substantial and immediately apparent.

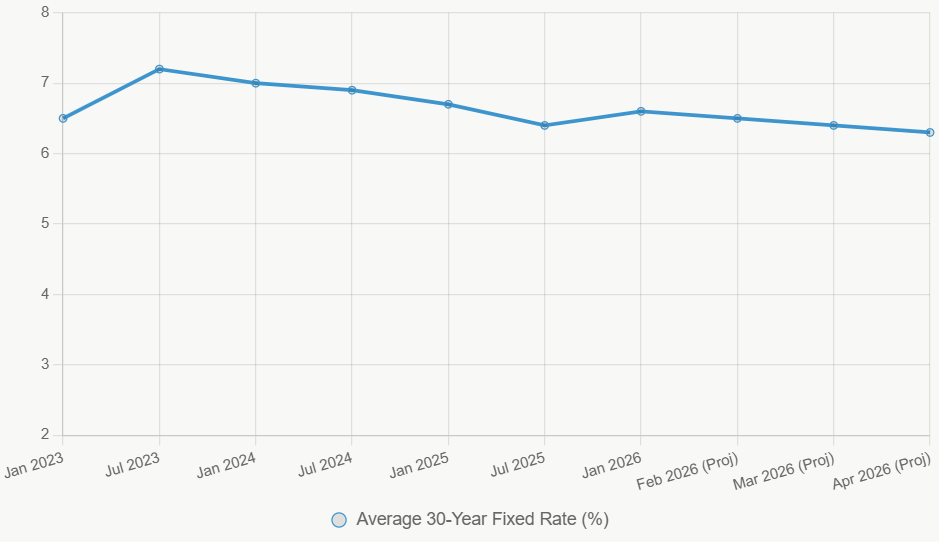

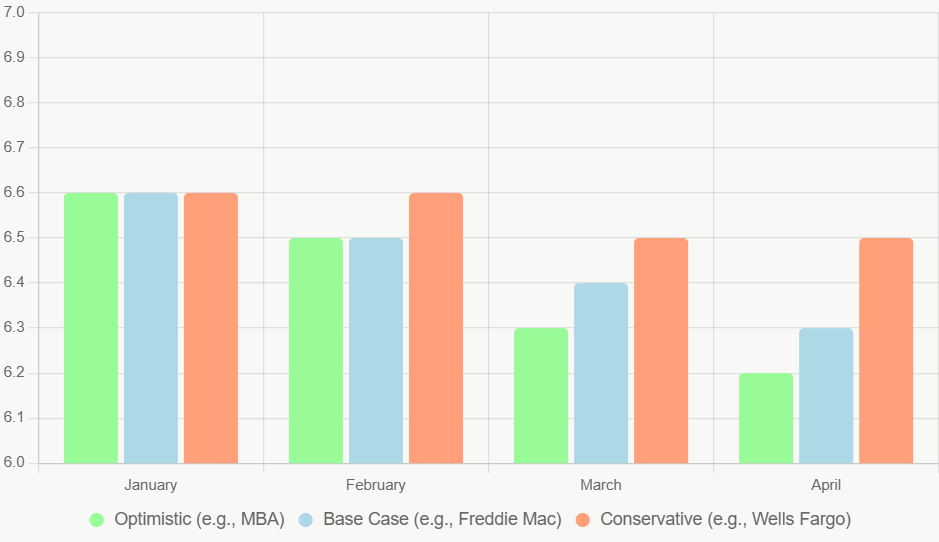

The 2026 Outlook and Forecast: What's Next for Rates?

Looking ahead, the mortgage market is expected to remain dynamic. While some experts predict that rates could dip as low as 5.5% if a recessionary environment takes hold, the consensus among major authorities like the Mortgage Bankers Association (MBA) and Fannie Mae points to a more moderate outlook.

- Moderate Volatility: For the remainder of 2026, the general expectation is that 30-year fixed mortgage rates will average between 5.9% and 6.4%. This means that while there might be ups and downs, the current attractive rate of 6.33% is likely to be a competitive offering for much of the year.

- Ongoing Refi Trend: Analysts are predicting a healthy 30% annual increase in total refinance volume for 2026. Based on current data, approximately 20% of all mortgaged homeowners still hold rates above 6%, meaning there’s a significant pool of borrowers who stand to benefit from refinancing.

- Shift to Home Equity: For the vast majority of Americans who secured mortgages during the pandemic at rates below 5% (roughly 70%), the demand isn't for traditional refinancing. Instead, their focus is shifting towards Home Equity Lines of Credit (HELOCs) and home equity loans. This allows them to tap into the substantial equity they've built in their homes without touching their low-interest primary mortgages.

This is a fascinating development. It shows how different segments of the homeowner population are strategizing based on their unique situations. Those with high rates are rushing to refinance, while those with low rates are looking to leverage their home's value for other financial needs.

In Conclusion:

The mortgage rates today, Jan 14, present a compelling opportunity for many homeowners to refinance. The significant drop in the 30-year refinance rate to 6.33% marks a favorable shift in the market. Whether you're looking to lower your monthly payments with a 30-year term or pay off your home faster with a 15-year term, now is an excellent time to explore your options and potentially save thousands over the life of your loan. Don't miss out on this chance to make your mortgage work better for you!

and

Florida’s modern build with strong cash flow vs Missouri’s affordable rental with higher cap rate. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Market forecasts suggest steady demand, making turnkey real estate one of the most reliable paths to passive income and wealth creation.

Norada Real Estate helps investors capitalize on these trends with turnkey rental properties designed for appreciation and consistent cash flow—so you can grow wealth securely while others wait for clarity in the market.

Recommended Read:

- 30-Year Fixed Refinance Rate Trends – January 13, 2026

- Best Time to Refinance Your Mortgage: Expert Insights

- Should You Refinance Your Mortgage Now or Wait Until 2026?

- When You Refinance a Mortgage Do the 30 Years Start Over?

- Should You Refinance as Mortgage Rates Reach Lowest Level in Over a Year?

- Half of Recent Home Buyers Got Mortgage Rates Below 5%

- Mortgage Rates Need to Drop by 2% Before Buying Spree Begins

- Will Mortgage Rates Ever Be 3% Again: Future Outlook

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years