As of today, November 29th, today's mortgage rates are tantalizingly close to a significant psychological barrier. According to Zillow's data, the average 30-year fixed mortgage rate stands firm at 6.00%. This means we're just a hair's breadth away from seeing rates dip into the 5% range, a move that could very well send a jolt of excitement through the housing market. For many potential buyers and homeowners looking to refinance, this 5% threshold has been a waiting game, and we might be on the cusp of seeing that signal to jump in.

Today's Mortgage Rates, Nov 29: 30-Year FRM Maintains Firm Stability at 6.00%

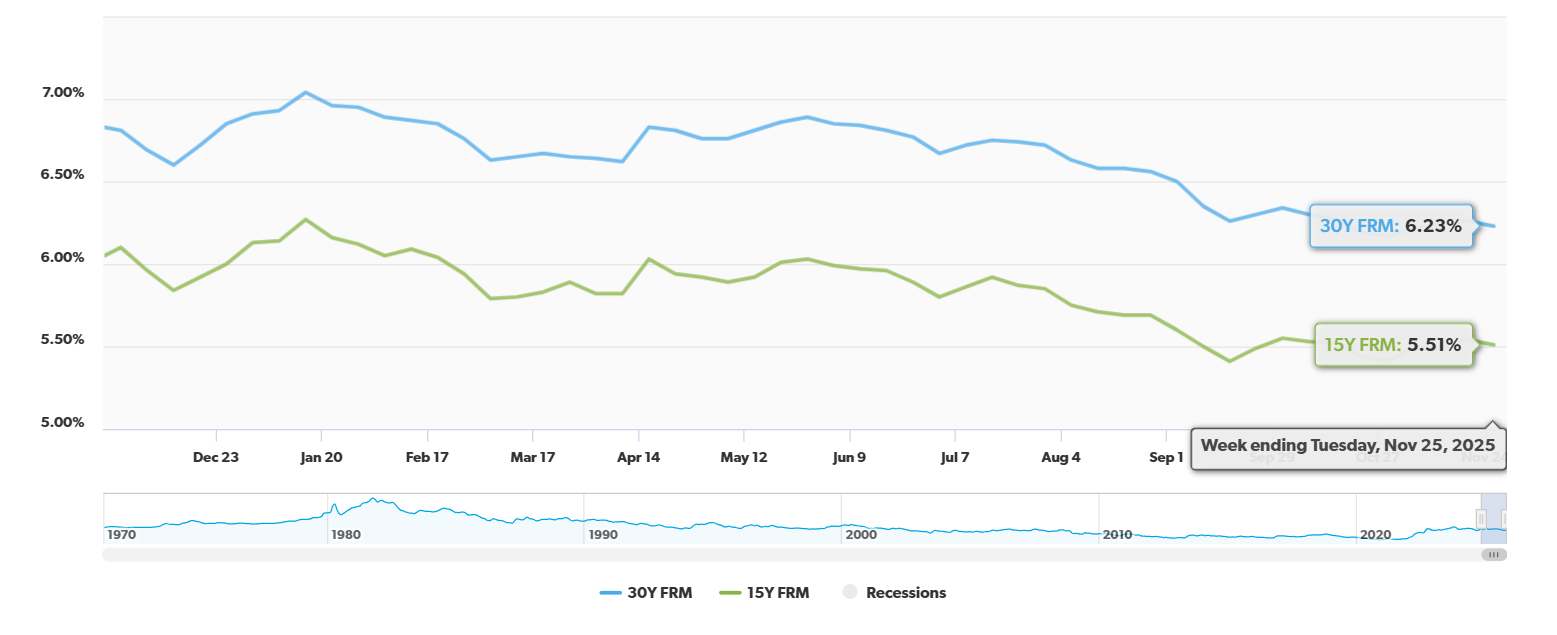

It's been a bit of an emotional rollercoaster watching mortgage rates. They've danced around this 6% mark for a while now, making potential buyers pause and homeowners consider if now is the time to lock in a better deal. But this shift we're seeing, this slow and steady creep downwards, feels different. It’s like watching a tide slowly pull back, revealing more of the shoreline than we’ve seen in a while.

The 15-year fixed mortgage rate is also holding steady, currently at 5.50%. This shorter-term option has always been a popular choice for those who want to pay off their homes faster and save on overall interest, and it’s good to see it offering even more attractive terms as rates generally trend lower. This steady movement on both fronts really underscores just how close we are to a more favorable borrowing environment.

What’s Actually on the Table Today: Today's Mortgage Rates

Let’s break down what these numbers mean in practical terms. Here’s a look at the average rates you might see, according to Zillow’s latest figures:

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.00% |

| 20-year fixed | 5.86% |

| 15-year fixed | 5.50% |

| 5/1 ARM | 6.11% |

| 7/1 ARM | 6.15% |

| 30-year VA | 5.44% |

| 15-year VA | 5.10% |

| 5/1 VA | 5.11% |

I've been following these numbers for years, and seeing rates hover around are generally good indicators. The 30-year fixed is the workhorse for most homebuyers, and 6.00% isn't a bad place to be, especially when you consider how much higher they were not too long ago. The 15-year fixed at 5.50% is a fantastic deal for those who can comfortably manage higher monthly payments for a decade less.

VA loans, designed for our veterans, continue to offer some of the most competitive rates, which is always heartening to see. The 30-year VA rate at 5.44% is a significant advantage for eligible borrowers.

Thinking About a Refinance? Today’s Mortgage Refinance Rates

For those of you already owning a home, the refinance market is also showing some promising movements. Refinancing at a lower rate can significantly reduce your monthly payments and the total interest paid over the life of your loan. Here’s how refinance rates are looking today:

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.14% |

| 20-year fixed | 6.05% |

| 15-year fixed | 5.60% |

| 5/1 ARM | 6.55% |

| 7/1 ARM | 6.72% |

| 30-year VA | 5.57% |

| 15-year VA | 5.18% |

| 5/1 VA | 5.04% |

It’s important to note that refinance rates are often a fraction of a percent higher than purchase rates. This difference accounts for the lender’s perspective on the risk involved. However, even a small drop can make a big difference when you're looking at a 15- or 30-year loan. If you bought your home a few years ago when rates were higher, it's definitely worth exploring if a refinance makes sense for you. My personal opinion? If you can shave off even half a percent or more, and your closing costs are manageable, it's often a win.

Fixed vs. ARM: Navigating Your Choices Near 6%

As rates hover around the 6% mark, the age-old question of fixed-rate mortgages versus Adjustable-Rate Mortgages (ARMs) comes to the forefront.

- Fixed-Rate Mortgages: These offer stability. Your interest rate and monthly principal and interest payment remain the same for the entire loan term. This is ideal if you value predictability and plan to stay in your home for a long time, or if you anticipate rates rising in the future. The 30-year fixed is the most common, offering lower monthly payments but more interest over time. The 15-year fixed has higher monthly payments but less interest overall.

- Adjustable-Rate Mortgages (ARMs): ARMs typically start with a lower introductory interest rate than fixed-rate loans. This initial rate is usually fixed for a set period (like 5 or 7 years), after which the rate adjusts periodically based on market conditions.

- Pros: Lower initial payments, which can help you qualify for a larger loan or save money in the short term.

- Cons: Payments can increase significantly after the introductory period if interest rates rise. This makes them riskier if you aren't prepared for potential payment hikes.

Looking at today's mortgage rates, the 5/1 ARM and 7/1 ARM are only slightly higher than the 30-year fixed. This is a bit unusual. Typically, ARMs are significantly lower to entice borrowers. This narrow gap might suggest a market environment where lenders are less aggressive with ARM pricing, possibly anticipating future rate stability or even declines. For someone who plans to move or refinance before the adjustment period kicks in, an ARM could still offer a good initial savings. However, the risk of future payment increases means I always advise caution with ARMs, especially if your financial situation isn't rock-solid.

Refinance Opportunities: Who Stands to Gain Most?

The prospect of rates dipping below 6% truly opens up refinancing doors for a wider group of homeowners.

- Recent Buyers: If you purchased a home in the last couple of years when rates were higher, even a small decrease can translate into significant savings. If your rate is, say, 7% or higher, moving down to 6% or even into the 5% range could easily save you hundreds of dollars a month.

- Those with Jumbo Loans: Sometimes, jumbo loans (loans exceeding conforming limits) can have slightly different rate movements. If you have a jumbo mortgage and your current rate is above 6%, explore refinancing options.

- Cash-Out Refinancers: If you need funds for home improvements, debt consolidation, or other major expenses, a cash-out refinance could be an option. With lower rates, the cost of borrowing that extra cash might be more manageable than it was previously.

- Homeowners Who Initially Waited: Many people held off on buying or refinancing, waiting for rates to become more favorable. The current movement towards the 5% range could be their cue to act.

I always encourage people to get a personalized quote. Zillow's data is a great snapshot, but your individual credit score, down payment, loan type, and lender will all play a big role in the actual rate you're offered.

What’s Pushing the Rates Around?

Several economic factors are influencing where mortgage rates are today. Understanding these can help give you a clearer picture of what might come next.

- Federal Reserve Actions (and Anticipation): The Federal Reserve has been actively adjusting its key interest rate. They've cut it twice this year, and there's a strong possibility of another cut in December. While the Fed doesn't directly set mortgage rates, their actions send ripples through the financial markets. Lowering the Fed's rate generally makes borrowing cheaper for banks, and they can pass some of those savings along to consumers in the form of lower mortgage rates.

- The Job Market's Temperature: Recent signals suggesting a softening in the job market have played a role in pushing mortgage rates down. When the economy shows signs of slowing, investors often seek safer assets, and bonds (which influence mortgage rates) become more attractive.

- The 10-Year Treasury Yield: This is perhaps the most direct influence on mortgage rates. The 10-year Treasury yield has seen a recent dip, and this has directly contributed to the downward trend in mortgage rates we're observing. Think of it as a close cousin to mortgage rates – when one goes down, the other usually follows.

- Housing Market Vibes: It’s a bit of a feedback loop. As rates decline and housing inventory (the number of homes for sale) sees a slight increase, it makes buying a home more accessible and attractive. We saw pending home sales pick up in October, which is a good sign that buyers are responding to these more favorable conditions.

Looking Ahead: What Experts Are Saying

Forecasting interest rates is notoriously tricky, and even the experts have differing opinions.

- Fannie Mae predicts that mortgage rates will likely stick around the low 6% range through 2026. This suggests a period of relative stability rather than dramatic drops.

- The Mortgage Bankers Association offers a slightly different outlook, suggesting rates might trend a bit higher than that prediction.

- However, a consensus seems to be forming: a return to the ultra-low rates we saw during the height of the pandemic is highly unlikely in the foreseeable future. The economic conditions are simply too different now.

From my vantage point, I believe we're in a period of normalization. The extreme lows of the pandemic era were an anomaly. The current rates, while higher than those peaks, are more reflective of long-term economic trends and a healthier housing market balance. It's a more sustainable environment, even if it means buyers and refinancers need to adjust their expectations compared to a couple of years ago.

Ultimately, today's mortgage rates, sitting right at the cusp of the 5% range, are a significant development. Whether you're looking to buy your first home, move up, or refinance your current mortgage, now is definitely a time to pay close attention and potentially explore your options.

Invest Smartly in Turnkey Rental Properties

With rates dipping to their lowest levels, investors are locking in financing to maximize cash flow and long-term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income while borrowing costs remain historically low.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?