The summer of 2024 promises to be an interesting one for the housing market. While some key indicators suggest a potential shift, others hint at a continuation of existing trends. Here, we'll explore 10 predictions for the housing market this summer, helping you decide whether it's a good time to buy or sell.

10 Predictions for the Housing Market This Summer (2024)

1. Continued Price Stability

Recent data shows a leveling off of home prices. Realtor.com reports the median listing price remaining flat year-over-year for the third week in a row. This suggests a potential end to the rapid price growth that has characterized the market in recent years. While some modest price increases may still occur, particularly in desirable locations, the breakneck speed of appreciation is likely to slow. This could be a welcome sign for potential buyers who have been priced out of the market in recent years.

2. More Homes on the Market

Good news for buyers! Inventory continues to rise. The latest data shows active inventory up 36.0% year-over-year. This increase in available homes is a significant shift from the seller's market that dominated for much of the past two years.

With more options to choose from, buyers will be able to take their time, compare properties, and negotiate for better deals. This increased selection is likely to put some downward pressure on prices, particularly for homes that may have been overpriced in the earlier period of rapid appreciation.

3. Mortgage Rates May Dip

While mortgage rates remain elevated compared to pre-pandemic levels, there are signs that they may start to come down. Recent weeks have seen a slight decline in rates, driven by promising inflation readings. If this trend continues, it could significantly improve affordability for potential buyers.

A drop in rates, even by a small percentage, could free up additional buying power, making homeownership a more realistic possibility for many. This could lead to a renewed surge in buyer activity, particularly from first-time buyers who have been particularly impacted by high mortgage rates.

4. Sellers May Become More Flexible

With rising inventory and the potential for declining mortgage rates, sellers may need to adjust their strategies. The days of multiple offers and bidding wars above asking price may be coming to an end. As the market shifts towards a more balanced state, sellers may need to be more flexible on price and negotiation.

This could involve being more open to contingencies, offering incentives to buyers, or considering lower offers. For buyers who have been discouraged by the intense competition of the seller's market, this newfound flexibility could present a significant opportunity.

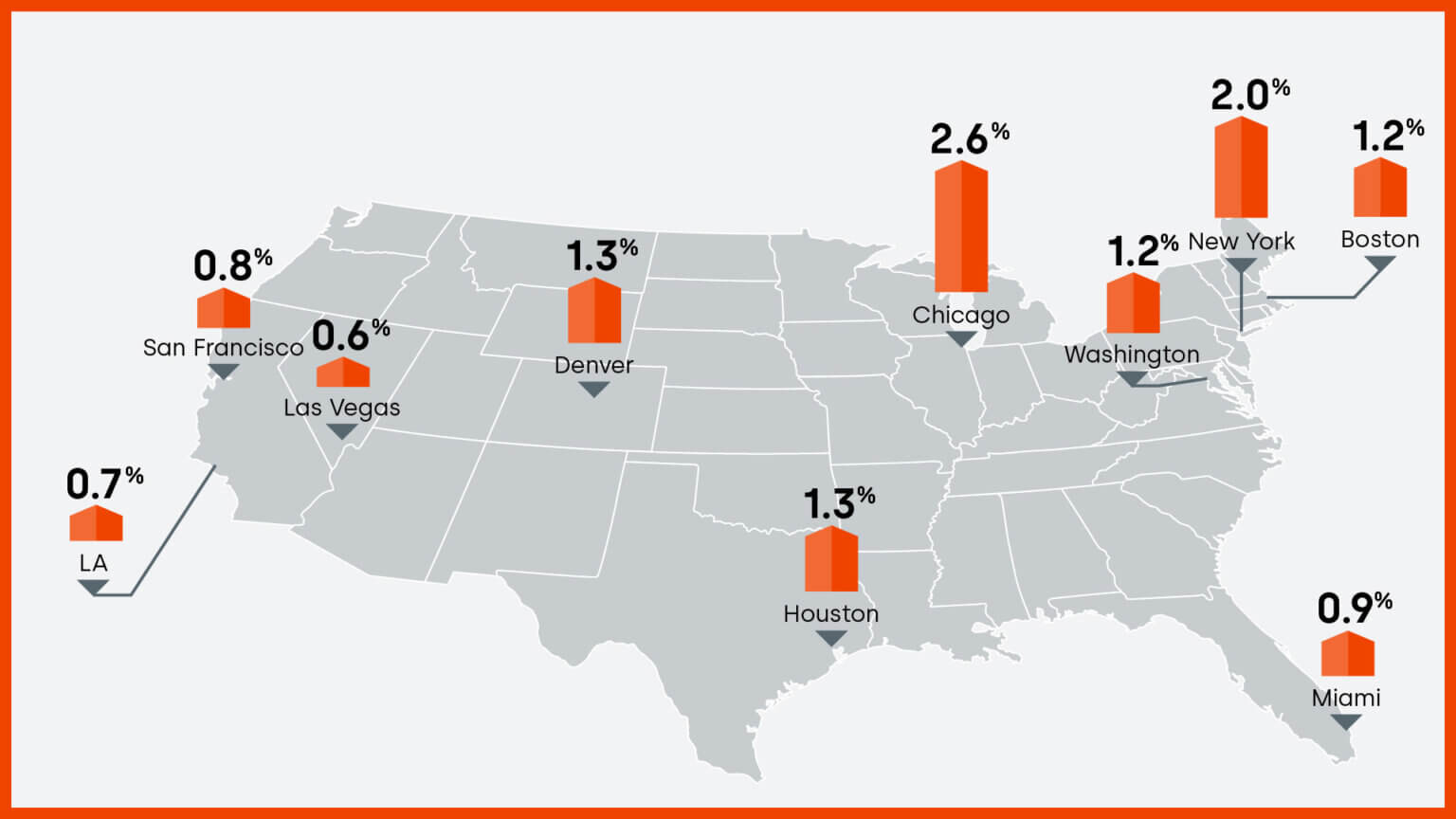

5. Regional Variations Will Persist

The housing market is not a monolith. Trends will continue to vary significantly depending on location. While some areas may experience a slowdown in price growth or even price declines, others, particularly those with strong job markets and limited inventory, may see continued price appreciation.

It's crucial for both buyers and sellers to consider local market conditions before making any decisions. Researching recent sales data, consulting with a local realtor, and understanding the economic outlook for your specific area will be essential for navigating the summer market effectively.

6. Time on Market May Increase

With more homes available and potentially more selective buyers due to lingering affordability concerns, the time it takes to sell a house may increase this summer. This is a shift from the fast-paced market of recent years, where homes often sold within days of listing.

Sellers who are unrealistic about pricing or inflexible in negotiations may find their properties lingering on the market for longer periods. However, for buyers who are patient and willing to do their research, this extended time on the market could present opportunities to find good deals and negotiate favorable terms.

7. First-Time Buyers May Have More Opportunities

The combination of rising inventory, potentially declining mortgage rates, and a more balanced market could create a window of opportunity for first-time buyers this summer. While affordability remains a challenge, an easing of competition and a potential increase in buying power could make homeownership a more attainable goal for many.

However, first-time buyers should still be prepared to act quickly on properties that meet their needs and budget. Carefully considering their financial situation, getting pre-approved for a mortgage, and working with a qualified real estate agent will be crucial for success in this evolving market.

8. Investors May Take a Backseat

With declining returns due to rising property values and potentially increasing mortgage rates, investor activity in the housing market may cool off this summer. This could be a positive development for first-time buyers who have faced stiff competition from investors willing to pay above the asking price. A decrease in investor activity could contribute to a more stable market and potentially lead to more favorable pricing for owner-occupants.

9. New Construction May Slow

The combined effect of rising interest rates and a potential softening of demand could lead to a slowdown in new construction this summer. Builders may become more cautious about starting new projects, particularly in areas with already high inventory levels. This could further tighten supply in the long term, especially in desirable locations with limited existing housing stock. However, in the short term, a slowdown in new construction could help to stabilize inventory levels and prevent a glut of houses on the market.

10. The Market Remains Dynamic

The housing market is constantly evolving, and the predictions outlined here should be viewed as possibilities, not certainties. Economic factors, government policies, and unforeseen events can all impact market conditions. For both buyers and sellers, staying informed about the latest trends and consulting with qualified professionals will be essential for making sound decisions in this dynamic market environment.

Overall Picture and Takeaway

So, to buy or sell this summer? The answer depends on your individual circumstances and priorities.

For buyers, the summer of 2024 presents a potentially more favorable market compared to recent years. Rising inventory, a potential dip in mortgage rates, and a shift towards a more balanced market could all create opportunities. However, affordability remains a concern, and regional variations will be significant. Careful research, sound financial planning, and working with a realtor are key to navigating this evolving market.

For sellers, the days of bidding wars and instant offers may be over. Adjusting pricing strategies, being flexible on negotiations, and considering market conditions are crucial for successful sales this summer.

The overall takeaway? The housing market this summer is likely to be characterized by greater stability compared to the recent period of rapid price growth. While some uncertainties remain, both buyers and sellers can find opportunities by staying informed, adapting their strategies, and making well-considered decisions based on their individual needs.

ALSO READ:

- Housing Market Predictions for the Next 2 Years

- Housing Market Predictions for Next 5 Years (2024-2028)

- Housing Market Predictions 2024: Will Real Estate Crash?

- Housing Market Predictions: 8 of Next 10 Years Poised for Gains

- Housing Market Predictions for 2027: Experts Differ on Forecast

- Prediction: Interest Rates Falling Below 6% Will Explode the Housing Market