Picking the right lender can seriously make or break your rental property investment journey, and in 2026, I've found the top players are those offering flexible terms, fast closings, and a deep understanding of investor needs. This guide dives into the U.S. market, spotlighting lenders who truly get what it takes to grow a robust rental portfolio.

Best Mortgage Lenders for Real Estate Investors in 2026

What's Cooking in Rental Property Financing for 2026?

Alright, let's talk about where things stand for us rental property investors heading into 2026. The market has definitely shifted from the frenzy of a few years ago. While interest rates aren't at those crazy lows we saw, they've actually settled down a bit, making things feel a lot more predictable. I’ve seen rates for investment property loans hovering, let’s say, between about 6% and 7.7% for a standard 30-year fixed, depending on who you're talking to and your own financial picture. This stabilization is actually good news for us because it means we can plan better.

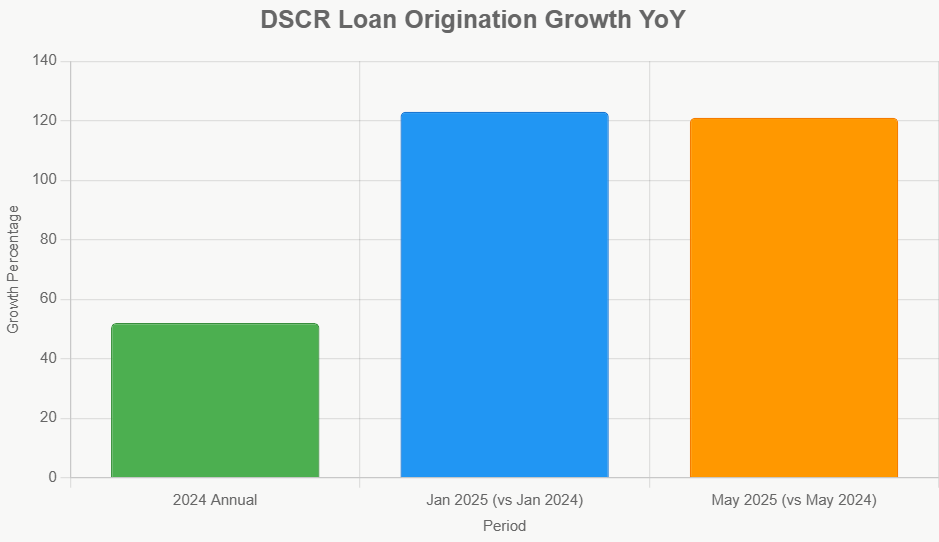

What’s really changed the game, though? It’s the rise of products like DSCR loans (Debt Service Coverage Ratio). These are a lifesaver for investors like me because they focus on the property’s rental income to qualify you, not just your personal W-2 income. This is huge for folks who are self-employed, run an LLC, or just want to scale up without relying solely on their personal tax returns.

Beyond DSCR, I'm seeing a lot more lenders using technology to speed things up. Think online applications, quick approvals, and closings that feel like they happen in the blink of an eye. Lenders like Kiavi and Rocket Mortgage are really leading the charge here, offering processes that can get you from application to keys in as little as 10-18 days. That’s a massive advantage when you're trying to snatch up a deal before anyone else.

Non-QM (non-qualified mortgage) lenders and private money lenders are also becoming more common, which is great news for those of us with slightly more complex financial situations. They're often more willing to work with you if the property itself can prove it can cover the debt.

And for those of us with a growing portfolio, portfolio loans and blanket loans are becoming more accessible. These allow you to bundle multiple properties under one loan, which can seriously simplify management and sometimes even get you better terms. Some lenders are even starting to offer interest-only loan options again, which can really boost your cash flow in the early years of owning a rental property, especially if you're doing some light renovations or repositioning the property.

Why DSCR Loans Are a Game Changer

Let’s dig a little deeper into the DSCR loan. It's pretty straightforward, and honestly, it's become my go-to for buying new rental properties. The core idea is to look at how much money the property makes from rent compared to how much it costs to pay the mortgage, taxes, and insurance.

The formula is:

DSCR = Net Operating Income (NOI) / Total Debt Service (PITIA)

- NOI (Net Operating Income): This is your rental income minus all your operating expenses (like property taxes, insurance, maintenance, property management fees, etc.), but before you pay your mortgage.

- PITIA: This stands for Principal, Interest, Taxes, and Insurance – your total monthly mortgage payment.

If your DSCR is above 1.0, it means the property is generating enough income to cover its own debts. Most lenders want to see a DSCR of at least 1.0 to 1.25. Some might go a bit lower if you have a strong financial background or are putting down more money.

The Upside of DSCR Loans:

- No Income Verification Hassle: This is the big one. You don't usually need to show your personal tax returns or prove your employment history.

- Speed: Because they focus on the property, underwriting can be much faster. I've seen closings happen in 10-21 days.

- Flexibility: They work for LLCs, corporations, and even foreign investors.

- Scalability: There's generally no hard limit on how many DSCR loans you can have.

- Versatility: Great for both long-term rentals and short-term stays like Airbnb.

Things to Keep in Mind:

- Slightly Higher Rates: Expect rates to be a bit higher than a conventional owner-occupied loan, typically by 0.5% to 2%.

- Prepayment Penalties: Many DSCR loans come with these, usually for 3 to 5 years. This means if you pay off the loan early, you might owe a penalty. Always check the terms!

- Down Payment: You'll typically need a down payment of 20% to 25%.

Beyond DSCR: Other Smart Choices for Investors

While DSCR loans are fantastic, I also keep an eye on other options:

- Interest-Only (IO) Loans: These allow you to pay only the interest for a set period (like 5 or 10 years). This dramatically increases your monthly cash flow, which is great for properties you're planning to hold long-term or if you're doing a value-add strategy.

- Portfolio and Blanket Loans: If you own multiple rental properties, these can be a lifesaver. They let you combine several properties into one loan, simplifying management and often giving you better terms than multiple individual loans.

- Private Money / Hard Money Loans: These are usually for shorter terms and come with higher costs but offer incredibly fast funding, often used for fix-and-flip projects or when you need to close super quickly and traditional lenders are too slow.

Top Picks: The Best Lenders for Rental Property Investors in 2026

After digging through the market, I've rounded up a few lenders that really stand out for rental property investors. I’m focusing on the U.S. market here because that’s where I see the most innovation and investor-friendly products right now.

Here’s a breakdown of some of my favorites, with a comparison table to make it easy to see what they offer:

| Lender | Core Loan Products | Min. Down Payment | DSCR Loan Available? | Avg. Interest Rate (Est. 2024-26) | Typical Approval Speed | Who It's Best For |

|---|---|---|---|---|---|---|

| Kiavi | DSCR, Bridge, IO, Portfolio | 20%–25% | Yes | 7.25%–9.00% | 10–15 days | Experienced investors, tech-savvy, chasing fast digital closings. Ideal for single-family rentals (SFRs). |

| Rocket Mortgage | Conventional, DSCR, IO | 25% | Yes | 7.06% (2024) | 20–25 days | Digital-first investors who prioritize user experience and top-notch customer service. |

| Rate (formerly Guaranteed Rate) | Conventional, DSCR, IO, Portfolio | 15% | Yes | 7.23% (2024) | 18 days | Investors seeking quick closings and a comprehensive digital platform across many loan types. |

| Griffin Funding | DSCR, Portfolio, IO | 15%–20% | Yes | 7.25%–9.00% | 6–21 days | Investors needing rapid, flexible funding options, even with less-than-perfect cash flow. |

| Angel Oak Mortgage Solutions | DSCR, Non-QM, IO, Portfolio | 20%–25% | Yes | 7.25%–9.00% | 21–30 days | Investors with complex credit, LLCs, or those who are foreign nationals needing flexible underwriting. |

| Visio Lending | DSCR, IO, Portfolio | 20% | Yes | 7.25%–9.00% | 21–30 days | Short-term rental (STR) investors, those who prefer no income documentation, and portfolio builders. |

| RCN Capital | DSCR, Bridge, IO | 20%–25% | Yes | 7.25%–9.00% | 14–21 days | Investors transitioning from fix-and-flip to long-term rentals (“flip-to-rent”) or needing quick bridge loans. |

| Bank of America | Conventional, Portfolio | 10% | Limited | 6.63% (2024) | 21–30 days | Prime borrowers with strong credit seeking the lowest rates and robust banking support. |

| Flagstar Bank | Conventional, DSCR, Non-QM, IO | 15% | Yes | 7.24% (2024) | 21–30 days | Investors needing lower down payments, non-QM options, or flexible underwriting with good service. |

Note: Rates are estimates based on 2024-2026 market data and can fluctuate based on individual circumstances, market conditions, and loan terms.

Diving Deeper into My Top Lender Picks

Let me give you a little more flavor on a few of these I've personally found to be excellent:

1. Kiavi: I’ve used Kiavi a few times, and their speed is legit. They’re a fintech company, so everything is online, and they’ve really streamlined the DSCR loan process. If you’re an experienced investor who knows what they want and needs to move fast on a single-family rental (SFR), they are fantastic. They process applications very quickly, often within 10–15 days. The caveat? They’re not as flexible for really unique or complicated situations.

2. Rocket Mortgage: You've probably heard of them. Rocket is a powerhouse because they’ve invested heavily in technology and customer experience. For rental properties, they do offer DSCR loans. Their average rates are competitive, not the absolute lowest, but their digital tools and customer service are top-notch. I’ve found their pre-approval process to be super smooth. The main thing is they usually require a 25% down payment, which is higher than some other options.

3. Rate (formerly Guaranteed Rate): Rate is another strong contender in the digital space that also offers a broad range of products, including DSCR and portfolio loans. Their average closing time is around 18 days, which is great. They have a lot of educational resources online, and their rates were pretty solid in 2024. I like that they offer a 15% down payment option on some of their investor loans, which is more accessible for many.

4. Griffin Funding: These guys are all about speed and flexibility. I’ve heard from other investors that Griffin Funding can get approvals done in as little as 6 days, and their DSCR guidelines are pretty forgiving, sometimes going as low as 0.75 if you have other strong points. They operate nationwide and offer personalized service, which is a big plus. If you need to close quickly and the property’s cash flow is just okay, but you’re confident about its potential, Griffin is definitely worth a look.

5. Angel Oak Mortgage Solutions: This is the lender I’d steer towards if you have a more complex financial profile. Angel Oak specializes in non-QM and DSCR loans and is known for its ability to underwrite manually. That means they can often work with investors who have less-than-perfect credit, or perhaps are purchasing through an LLC or are foreign nationals. While their closings might take a bit longer (around 21-30 days), their flexibility can be invaluable for these situations.

Key Things to Consider When Shopping Around

Beyond just the lender's name, here’s what I always look at:

- Interest Rates: Even a fraction of a percent can make a big difference over the life of a loan. Compare not just the advertised rate but also the Annual Percentage Rate (APR), which includes fees. For 2026, I'm expecting investment property rates to generally fall in the 6.0%–7.7% range for 30-year fixed loans. DSCR loans will typically be a bit higher.

- Down Payment and LTV (Loan-to-Value): How much cash do you need upfront? Traditional loans might ask for 20-25%, but some DSCR lenders are more flexible, allowing as little as 15-20% down.

- Approval Speed: If you're in a competitive market, speed is crucial. Fintech lenders like Kiavi and Rate often have the edge here. Are you looking at 10 days or 30 days?

- Customer Service & Experience: Is it easy to communicate with them? Do they seem to understand your needs as an investor? Ratings from sources like J.D. Power or even just online reviews can give you a good feel. Rocket Mortgage consistently scores high here.

- Fees & Prepayment Penalties: Don't get blindsided by origination fees, appraisal costs, or other charges. And definitely understand any prepayment penalties on DSCR loans or other investor products.

The Bottom Line

Choosing the best lender for rental property investors in 2026 isn't a one-size-fits-all decision. It truly depends on your specific situation: your credit score, how much you can put down, the type of property you're buying, and how quickly you need to close.

DSCR loans have really opened the door for a lot of investors, myself included, allowing us to focus on the asset's income potential. Companies like Kiavi, Rocket Mortgage, Rate, Griffin Funding, and Angel Oak are leading the pack with innovative products and streamlined processes.

My advice? Do your homework. Reach out to a few of these lenders, get pre-approved, and compare their offers side-by-side. Understanding their strengths and weaknesses will help you find the perfect partner to help you build your rental property empire.

And

Murfreesboro’s affordable A- rental vs Nashville’s higher‑priced property with stronger NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Norada Real Estate helps you invest in turnkey rental properties—designed to generate passive income and long‑term wealth while minimizing the headaches of property management.

Also Read:

- Why Investors Are Buying New-Build Turnkey Rentals Across Multiple Markets

- Top Real Estate Investment Markets to Watch in 2026

- Top 10 Most Popular Housing Markets of 2025 for Homebuyers

- Will Real Estate Rebound in 2026: Top Predictions by Experts

- Housing Market Predictions for the Next 4 Years: 2026, 2027, 2028, 2029

- Housing Market Predictions for 2026 Show a Modest Price Rise of 1.2%

- Housing Market Predictions 2026 for Buyers, Sellers, and Renters

- 12 Housing Markets Set for Double-Digit Price Decline by Early 2026

- Real Estate Forecast: Will Home Prices Bottom Out in 2025?

- Housing Markets With the Biggest Decline in Home Prices Since 2024

- Why Real Estate Can Thrive During Tariffs Led Economic Uncertainty

- Rise of AI-Powered Hyperlocal Real Estate Marketing in 2025

- Real Estate Forecast Next 5 Years: Top 5 Predictions for Future

- 5 Hottest Real Estate Markets for Buyers & Investors in 2025