Is the housing market about to take a turn? The short answer is yes, but perhaps not the dramatic drop some were expecting. The National Association of Realtors (NAR) has adjusted its housing market forecast for 2025, now anticipating existing-home sales to reach 4.3 million, a 6% increase compared to 2024. While still positive, this is a step down from their previous, more optimistic projections.

For months, I've been closely watching the market, speaking with local agents, and analyzing trends. The initial excitement for a booming 2025 is now tempered with a dose of reality. Let's dive into what's causing this revision and what it could mean for you, whether you're a buyer, seller, or simply curious about the real estate world.

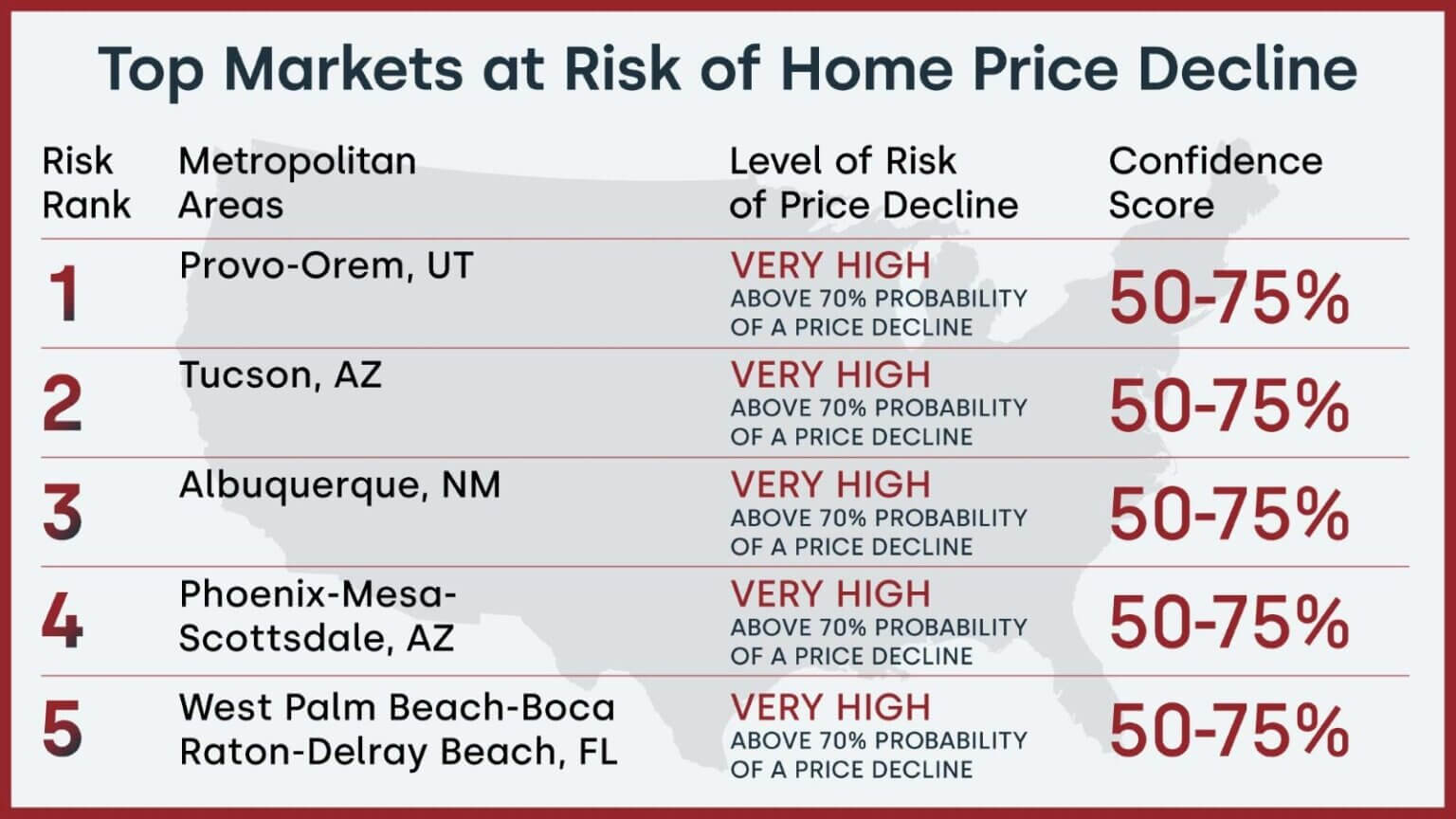

NAR Cuts 2025 Housing Market Forecast: Home Sales to Hit 4.3 Million

Why the Change of Heart at NAR?

Back in late 2024, NAR was pretty confident, forecasting existing-home sales to hit 4.9 million in 2025. So what happened? According to their updated NAR Real Estate Forecast Summit Update, several factors contributed to this shift.

- Strained Affordability: This is the big one. Home prices have remained stubbornly high, and while mortgage rates have fluctuated, they haven't dropped enough to significantly ease the burden on potential buyers.

- Price Growth Adjustments: NAR initially predicted a modest 2% home-price growth for both 2025 and 2026. Now, they've revised that upward to 3% and 4%, respectively. This means homes will likely be even less affordable than previously thought.

- Realistic Expectations: I believe part of the revision is simply a dose of realism. While the market has shown resilience, the factors that were expected to fuel a major boom haven't materialized as strongly as anticipated.

A Closer Look at the Revised Numbers

Here's a breakdown of NAR's revised forecasts:

- Existing-Home Sales (2025): 4.3 million (up 6% from 2024) – Previous forecast: 4.9 million

- New-Home Sales (2025): Up 10% – Previous forecast: Up 11%

- Existing-Home Sales (2026): Up 11% (remains within the previously projected range of 10%-15%)

- New-Home Sales (2026): Up 5% – Previous forecast: Up 8%

- Home-Price Growth (2025): 3% – Previous forecast: 2%

- Home-Price Growth (2026): 4% – Previous forecast: 2%

The biggest takeaway? While the market is still expected to grow, the pace of that growth is slowing down.

Is It All Doom and Gloom?

Not at all! Despite the downgraded forecast, NAR Chief Economist Lawrence Yun remains optimistic. He stated on the webinar that “The worst is over [for home sales]. The worst for inventory is over. I think the recession probability is still slim. Job additions, lower mortgage rates and all the factors driving home sales are moving positively, so look for more business opportunities this year.”

And honestly, I agree with his sentiment. The market has been through some rough patches, and the fact that it's still showing signs of growth is encouraging. Several positives are still at play:

- Job Market Stability: A strong job market provides confidence to potential homebuyers.

- Potential for Lower Mortgage Rates: While rates haven't plummeted, the expectation is that they will gradually decrease, making homes more accessible.

- Inventory Slowly Improving: While still below historical averages, housing inventory is slowly increasing in many markets, giving buyers more options.

How Does This Compare to Other Forecasts?

It's important to remember that NAR isn't the only organization making predictions. Their revised forecast of 4.3 million existing-home sales is actually more in line with other industry experts.

To put things in perspective:

- NAR (Revised): 4.3 million

- HousingWire (Mohtashami/Simonsen): 4.2 million

- Realtor.com: 4 million

This suggests that NAR's initial forecast was an outlier, and the revised numbers represent a more consensus view of the market.

Recommended Read:

Warning of a Weak Housing Market: Are We Headed for Another Crisis?

Fannie Mae Lowers Housing Market Forecast and Projections for 2025

Housing Market Forecast 2025 by JP Morgan Research

Housing Predictions 2025 by Warren Buffett's Berkshire Hathaway

What Does This Mean for Buyers?

If you're hoping for a dramatic price crash, this forecast suggests you might be waiting a while. While prices might not skyrocket, they're expected to continue their upward trend.

Here's my advice for buyers:

- Get Pre-Approved: Knowing how much you can afford is crucial.

- Be Realistic: Don't expect to find a bargain. Focus on finding a home that meets your needs within your budget.

- Consider Different Markets: Look at areas that might be slightly more affordable than your ideal location.

- Be Patient: The right home will come along, so don't feel pressured to jump into something you're not comfortable with.

- Do not time the market:*Time in the market is more important than timing the market.

What Does This Mean for Sellers?

While the market might not be as hot as it was a few years ago, it's still a good time to sell, especially if you've built up equity.

Here's my advice for sellers:

- Price Your Home Competitively: Don't overprice your home. Work with a real estate agent to determine a fair market value.

- Make Necessary Repairs: Ensure your home is in good condition to attract buyers.

- Stage Your Home: Make your home as appealing as possible to potential buyers.

- Highlight the Positives: Emphasize the unique features of your home and neighborhood.

My Personal Take

As someone deeply involved in real estate, I believe the revised forecast is a healthy dose of realism. The initial excitement for a massive boom was probably a bit overblown. The market is still moving in a positive direction, but it's doing so at a more sustainable pace.

I've seen firsthand how affordability challenges are impacting buyers. Many are priced out of their ideal markets, forcing them to make compromises or delay their home-buying dreams. This is why it's crucial to focus on solutions that address affordability, such as increasing housing supply and exploring alternative financing options.

Overall, I remain cautiously optimistic about the future of the housing market. While there are challenges ahead, the fundamentals remain strong. With a stable job market and the potential for lower mortgage rates, I believe the market will continue to grow, albeit at a more moderate pace.

Key Takeaways:

- NAR has downgraded its housing market forecast for 2025, now expecting existing-home sales to reach 4.3 million.

- The revision is primarily due to strained affordability and upward adjustments to home-price growth projections.

- Despite the downgrade, NAR remains optimistic about the market's overall trajectory.

- The revised forecast is more in line with other industry experts' predictions.

- Buyers should focus on affordability and be patient, while sellers should price their homes competitively.

Tables:

| Forecast | Previous Estimate | Revised Estimate | Change |

|---|---|---|---|

| Existing Home Sales 2025 | 4.9 million | 4.3 million | -0.6 million |

| New Home Sales 2025 | Up 11% | Up 10% | -1% |

| Home Price Growth 2025 | 2% | 3% | +1% |

| Home Price Growth 2026 | 2% | 4% | +2% |

Final Thoughts

The housing market is always changing. Stay informed, consult with trusted professionals, and make decisions that are right for your individual circumstances. Whether you're buying, selling, or simply keeping an eye on the market, understanding the trends is key to navigating this complex landscape.

Work with Norada in 2025, Your Trusted Source for Investment

in the Top Housing Markets of the U.S.

Discover high-quality, ready-to-rent properties designed to deliver consistent returns.

Contact us today to expand your real estate portfolio with confidence.

Contact our investment counselors (No Obligation):

(800) 611-3060

Also Read:

- Will the Housing Market Crash Due to Looming Recession in 2025?

- 4 States Facing the Major Housing Market Crash or Correction

- 5 Cities Where Home Prices Are Predicted To Crash in 2025

- New Tariffs Could Trigger Housing Market Slowdown in 2025

- Housing Market Forecast 2025: Affordability Crisis Will Continue

- Lower Mortgage Rates Will Reignite the Housing Demand in 2025

- NAR Predicts 6% Mortgage Rates in 2025 Will Boost Housing Market

- Housing Market Forecast for the Next 2 Years: 2024-2026

- Housing Market Predictions for the Next 4 Years: 2025 to 2028

- Housing Market Predictions for Next Year: Prices to Rise by 4.4%

- Housing Market Predictions for 2025 and 2026 by NAR Chief

- Real Estate Forecast Next 5 Years: Top 5 Predictions for Future

- Real Estate Forecast Next 10 Years: Will Prices Skyrocket?