Is Florida's housing market headed for another crash akin to 2008? According to real estate analyst Nick Gerli, CEO of Reventure, the answer is potentially yes. A combination of dwindling migration, an oversupply of homes, and sky-high prices are creating a perfect storm that could trigger a significant and prolonged downturn in the Sunshine State's housing sector.

Is the Florida Housing Market Headed for Another Crash Like 2008?

The Ghost of 2008: Are We Seeing a Repeat?

The 2008 housing crisis is a scar on the American economy. We all remember the stories: rampant speculation, easy credit, and ultimately, a massive collapse that sent shockwaves through the world. So, when someone suggests we might be heading down that road again, it's only natural to feel a sense of unease.

And frankly, as someone who's been following the real estate market for years, I share that concern. While there are some key differences between then and now, the warning signs in Florida are definitely flashing.

The Pandemic Boom and the Subsequent Bust

The pandemic created an artificial surge in Florida's housing market. People fled densely populated cities in search of more space, sunshine, and a perceived lower cost of living (at least initially). This influx of new residents fueled a frenzy of construction, with developers rushing to meet the seemingly insatiable demand.

However, as Gerli points out, that trend has reversed. The massive wave of migration has slowed to a trickle, dropping by a staggering 80% from its peak. Suddenly, the market is flooded with homes, but the buyers are gone.

Here’s a breakdown of the key factors contributing to the potential downturn:

- Decreased Migration: The pandemic-fueled influx has subsided, leaving a void in demand.

- Oversupply of Homes: Construction boomed during the pandemic, creating an excess of available properties.

- Affordability Crisis: Prices remain stubbornly high, pricing out local buyers.

- High Housing Costs: 39% of income goes towards house payments.

The Numbers Don't Lie: A Deep Dive into the Data

Gerli highlights some truly alarming statistics. Florida currently has a record 177,000 homes for sale, while the entire Northeast U.S. has only 79,000 listings. That stark contrast paints a clear picture of the oversupply issue in Florida.

Moreover, the affordability crisis is reaching a critical point. According to Reventure's estimates, Floridians now need to spend a whopping 39% of their income on mortgage and tax costs – a level not seen since the 2006-07 bubble. That kind of financial strain is unsustainable and leaves homeowners vulnerable to economic shocks.

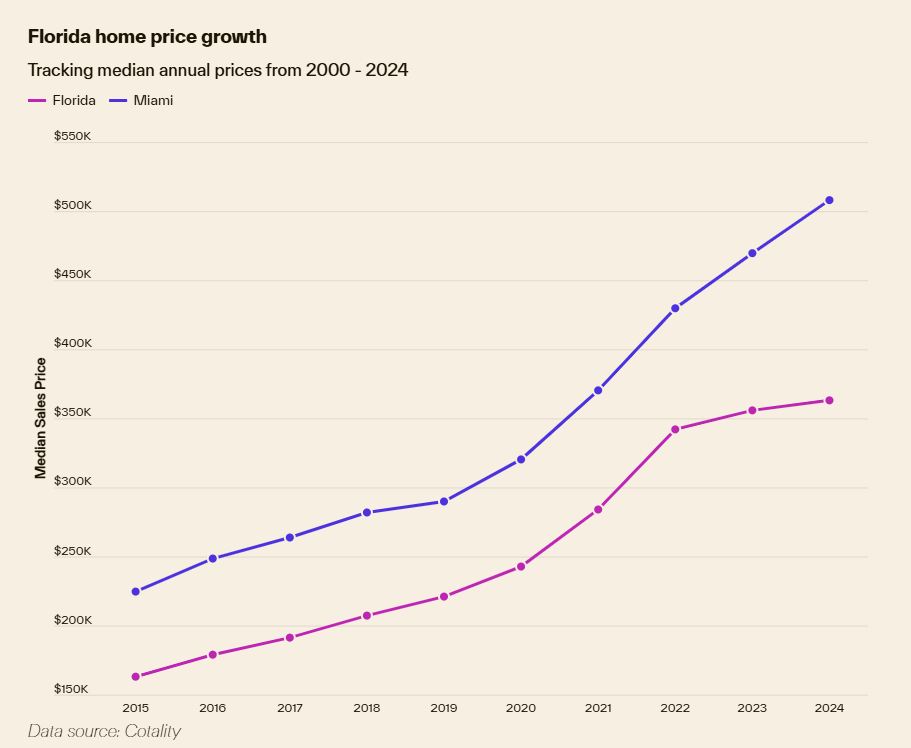

Furthermore, while home prices are rising in many parts of the country, they've already started to decline in Florida, dropping by 2.4% in the past year. Reventure predicts a further 5% drop in the coming year. This suggests that the market is already correcting, and the correction could accelerate if the underlying issues aren't addressed.

I don't think people understand what's happening in housing market right now.

Florida now has 177,00 listings. Highest level on record.

Entire Northeast U.S. has 79,000 listings. Lowest level on record.

People are leaving Florida. And moving back north. A structural trend that… pic.twitter.com/NYAJ9jN0Hp

— Nick Gerli (@nickgerli1) May 1, 2025

Why Migration Matters: It's Not Just About the Weather

Gerli correctly identifies the decline in inbound migration as the most critical factor driving the potential downturn. While things like HOA fees, hurricane risk, and insurance costs certainly play a role, they're not the primary drivers.

Migration is the lifeblood of Florida's housing market. It fuels demand, supports construction, and drives economic growth. Without a steady stream of new residents, the market simply can't sustain itself, especially with the current oversupply of homes.

I think Gerli is on the right track, and his main point is that blaming insurance and other expenses is not the entire picture.

The Human Cost: Who Will Be Affected?

A housing market downturn in Florida would have far-reaching consequences, affecting homeowners, developers, and the broader economy.

- Homeowners: Those who bought at the peak of the market could find themselves underwater on their mortgages, owing more than their homes are worth. This can lead to foreclosures and financial hardship.

- Developers: Builders who have invested heavily in new construction could face significant losses as demand dries up and prices fall.

- The Economy: A housing market crash could trigger a recession, leading to job losses and decreased consumer spending.

Is There a Way Out? A Glimmer of Hope

Gerli believes that the only way to counteract these trends is through “significantly cheaper prices” that could entice more people to move back to Florida. A significant drop in price may reignite the market.

While that may seem like a drastic measure, it's a necessary correction. The market needs to find a new equilibrium where prices are more aligned with local incomes and the overall economic reality.

Here is a summary of ways out:

- Significant Price Reduction: Lower prices could attract new buyers and stimulate demand.

- Incentives for Relocation: State or local initiatives could encourage migration.

- Economic Diversification: Creating new industries and job opportunities could attract a wider range of residents.

My Take: A Time for Caution and Prudent Planning

I wouldn't start panic selling. However, I believe that Florida homeowners should be aware of the risks and take steps to protect themselves. If you're considering buying a home in Florida, proceed with caution and do your research. Don't get caught up in the hype, and be sure to factor in all the potential costs, including insurance, taxes, and HOA fees.

What Can We Learn From 2008?

The 2008 crisis taught us some hard lessons about the dangers of speculation, overleveraging, and unsustainable growth. Hopefully, policymakers, developers, and individuals will heed those lessons and take steps to prevent a repeat of the past.

While Florida's housing market faces significant challenges, it's important to remember that the situation is not necessarily hopeless. By understanding the risks, taking proactive steps, and working together, we can navigate these turbulent times and build a more sustainable housing market for the future.

This is a long game, and a slow bleed is better than a quick hemorrhage.

“Invest in Real Estate in Top Florida Markets”

Discover high-quality, ready-to-rent properties designed to deliver consistent returns.

Contact us today to expand your real estate portfolio with confidence.

Contact our investment counselors (No Obligation):

(800) 611-3060

Read More:

- Tax Relief Proposed as Florida Housing Market Faces Deepening Crisis

- Is the Florida Housing Market on the Verge of Collapse or a Crash?

- 3 Florida Cities at High Risk of a Housing Market Crash or Decline

- 4 States Facing the Major Housing Market Crash or Correction

- Florida Housing Market: Record Supply Expected to Favor Buyers in 2025

- Florida Housing Market Forecast for Next 2 Years: 2025-2026

- Florida Real Estate Market Saw a Post-Hurricane Rebound Last Month

- Florida Housing Market: Predictions for Next 5 Years (2025-2030)

- Hottest Florida Housing Markets in 2025: Miami and Orlando

- Florida Real Estate: 9 Housing Markets Predicted to Rise in 2025

- Housing Markets at Risk: California, New Jersey, Illinois, Florida

- 3 Florida Housing Markets Are Again on the Brink of a Crash

- Florida Housing Market Predictions 2025: Insights Across All Cities

- Florida Housing Market Trends: Rent Growth Falls Behind Nation

- When Will the Housing Market Crash in Florida?

- South Florida Housing Market: Will it Crash?

- South Florida Housing Market: A Crossroads for Homebuyers