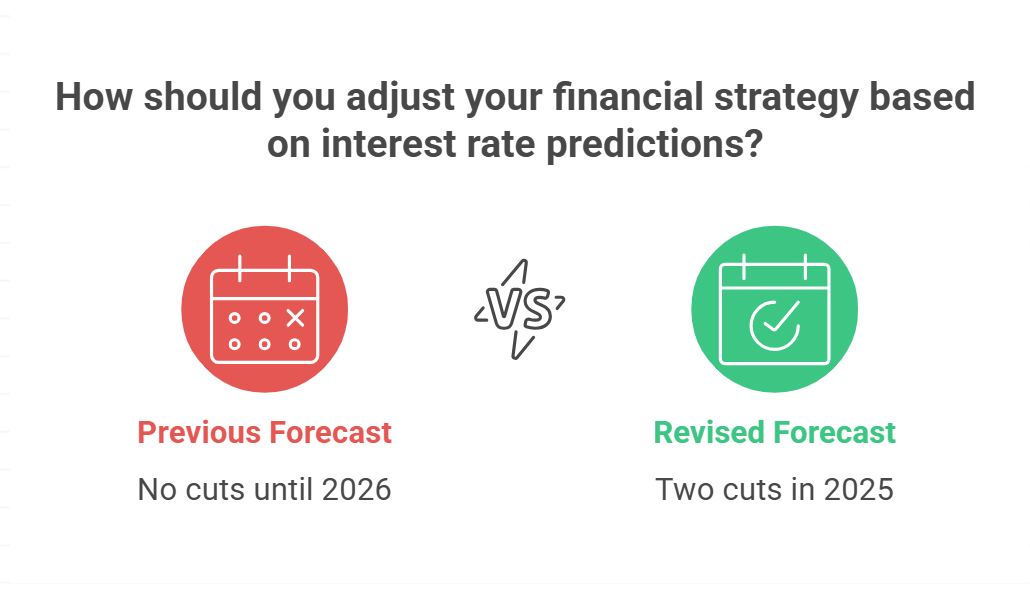

Are you keeping an eye on where interest rates are headed? You should be! Interest rate predictions by Bank of America have shifted, and it could impact your wallet. Bank of America now expects the Federal Reserve to cut interest rates twice in 2025. This is a change from their earlier forecast of no cuts until 2026. Expect two cuts of 25 basis points in September and December, bringing the federal funds rate down to 3.75%-4.00%.

This change of heart from Bank of America is a big deal. Why did they change their minds, and what does it mean for you, your savings, and your future investments? Let's dive into the details and break it down in a way that's easy to understand.

Interest Rate Predictions by Bank of America for 2025 and 2026

Background on Current Interest Rates

Before we get into Bank of America's predictions, let's remember where we are right now. The Federal Reserve (or “the Fed”) has kept the federal funds rate steady at 4.25%-4.50% throughout 2025. Think of this rate like a benchmark, influencing many other interest rates you see every day. This pause came after three cuts in late 2024, which brought rates down from a high of 5.25%-5.50%. The goal was and is to fight inflation, which has been hanging around 2.4%-2.5%, close to the Fed's target of 2%.

Why Bank of America Changed Its Tune

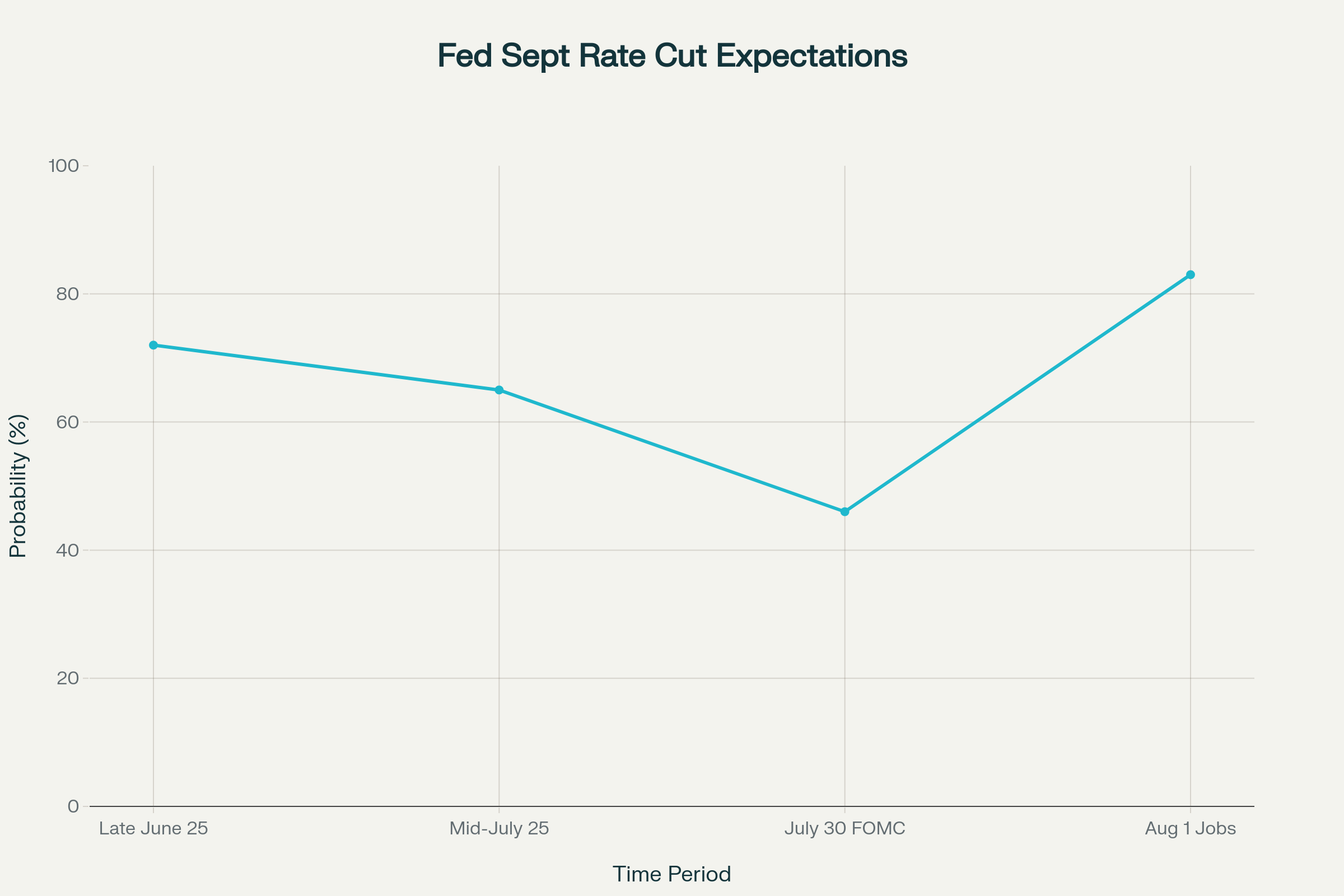

Okay, so what made Bank of America change their prediction from no cuts to two cuts? It all boils down to the economy, specifically some recent news about the job market. Earlier in the year, economists at Bank of America thought the economy was strong, growing steadily, and keeping inflation in check. This made them believe that the Fed wouldn't need to cut rates in 2025.

But then the August jobs report came out, and it wasn't pretty. Only 22,000 jobs were added, way below what experts predicted. This was the weakest job growth since 2020, apart from some weird times during the pandemic. On top of that, the unemployment rate rose to 4.3%.

This set of data made Bank of America realize that the economy might not be as strong as they thought. Weaker job growth is typically an indication that the Fed can loosen up on its strict stance.

What this means for everyday Americans and the economy

If these rate cuts happen, what will it mean for you and me? Here are some possible effects:

- Lower borrowing costs: Mortgages, auto loans, and credit cards could become cheaper.

- Lower savings account yields: Your savings accounts and CDs might not earn as much interest.

- Boost to investment: Businesses might be more likely to invest and grow.

- Possible stock market rally: Cheaper capital could send markets higher, but inflation is always a worry.

Comprehensive Analysis of Bank of America's Revised Interest Rate Forecast

Let's get deeper into why Bank of America changed its forecast and what it really means for you.

Before, they were pretty optimistic, thinking the U.S. would avoid a recession even with high interest rates. They saw steady growth – around 2.5% GDP increase – and felt inflation was under control. But the August jobs report changed everything.

1. The Shift and New Numbers

The numbers speak for themselves. Just 22,000 jobs were added in August. Let's be honest, that is really low. Seeing this data made Bank of America rethink their plan, and they now expect the Fed to drop rates twice this year.

Specifically, cuts to bring the federal funds rate to 4.00%-4.25% and 3.75%-4.00% in September and December, respectively. They also predict three more cuts in 2026, landing rates to 3.00%-3.25%.

Now, even with these cuts coming, be reminded that inflation is at almost 3%, so don't expect super-aggressive easing.

2. Economic Indicators That Sparked the Change

The August jobs report was the big turning point. But it wasn't the only sign of a cooling economy. Here's a look at other key figures:

- Job Growth and Unemployment: Only 22,000 jobs were added in August

- Wage Pressures: Average hourly earnings rose 0.2% monthly (3.9% annually). So it is gradually decreasing.

- Inflation Trends: The Consumer Price Index (CPI) stayed at around 2.5% year-over-year.

- GDP and Consumer Confidence: GDP was growing at 2.8% earlier in the year.

3. How Bank of America Compares to the Rest

Bank of America's updated forecast puts them closer to other big banks and market predictions. However, they're still a bit conservative. While most think it's close to being a certainty, nothing is ever guaranteed.

Here's a sample view of 2025 cuts as envisioned at top financial institutions.

| Institution | Predicted 2025 Cuts (Basis Points) | End-2025 Rate Range |

|---|---|---|

| Bank of America | 50 (Sep & Dec) | 3.75%-4.00% |

| J.P. Morgan | 100 | 3.25%-3.50% (by Q1 2026) |

| Morgan Stanley | 75 (Sep, Dec, potential third) | 3.50%-3.75% |

| Goldman Sachs | 50 | 3.75%-4.00% |

| Market (CME) | 75-100 (probabilistic) | 3.50%-3.75% |

4. Historical context

Looking back at the past can shed light on what might happen next. The Fed's current situation is like past cycles where they paused rate hikes to tame inflation. They acted similarly in 2001 and 2008 with the central bank averting deeper downturns by cutting rates, but sometimes fueling bubbles.

The impact on you, businesses, and the market

Let's break down the potential effects of these rate cuts on different parts of the economy:

- The Consumer.

- Mortgages: Mortgage rates could dip below to around the low 6%, creating savings for borrowers.

- Savings and Investments: Savings accounts and CDs might not earn as much, so people might look for other investments.

- Everyday Spending: Big purchases might go up, but fear of job loss could keep spending under control.

- The Business

- Financing: Lower rates make it cheaper to borrow, which would encourage investment.

Financial Markets:

- Stocks: Sectors such as Housing and Consumer spending are likely to jump and give a boost to investments in these segments. Bonds and housing would also likely see good times ahead.

The Fed's own Signals and Future Plans

Even the people involved like the head guys at the FED have grown to be “dovish” or more considerate of lowering the rates. What's more, they see gradual cuts being plausible for the period ahead.

Final Thoughts: Bank of American's shift to now include rate cuts encapsulates the uncertainties as well as the vulnerabilities of the US economy. What is most important that as things progress, you must consistently monitor all data and information along the way to make informed decisions.

Position Your Portfolio Ahead of the Fed’s Next Move

The Federal Reserve’s next rate decision could shape real estate returns through the rest of 2025. Whether or not a rate cut happens, smart investors are acting now.

Norada Real Estate helps you secure cash-flowing properties in stable markets—shielding your investments from volatility and interest rate swings.

HOT NEW LISTINGS JUST ADDED!

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Recommended Read:

- Fed Holds Interest Rates Steady for the Fifth Time in 2025

- Fed Projects Two Interest Rate Cuts Later in 2025

- Interest Rate Predictions for the Next 3 Years: 2025, 2026, 2027

- When is Fed's Next Meeting on Interest Rate Decision in 2025?

- Interest Rate Predictions for the Next 10 Years: 2025-2035

- Will the Bond Market Panic Keep Interest Rates High in 2025?

- Interest Rate Predictions for 2025 by JP Morgan Strategists

- Interest Rate Predictions for Next 2 Years: Expert Forecast

- Fed Holds Interest Rates But Lowers Economic Forecast for 2025

- Fed Indicates No Rush to Cut Interest Rates as Policy Shifts Loom in 2025

- Fed Funds Rate Forecast 2025-2026: What to Expect?

- Interest Rate Predictions for 2025 and 2026 by NAR Chief

- Market Reactions: How Investors Should Prepare for Interest Rate Cut

- Impact of Interest Rate Cut on Mortgages, Car Loans, and Your Wallet