Is the economy slowing down? The August 2025 Jobs Report points suggests the answer is yes. The U.S. labor market is showing signs of weakness, with job growth falling far short of expectations and the unemployment rate creeping upward. This softening is likely to push the Federal Reserve to cut interest rates in September, which could give homeowners and investors some relief.

Will the Latest Jobs Report Influence Fed's Upcoming Interest Rate Cut Decision

The August 2025 U.S. Jobs Report, released by the Bureau of Labor Statistics (BLS) on September 5, 2025, painted a picture of a labor market under strain, with subdued job growth, rising unemployment, and downward revisions to prior months' data. Let's delve into the report's key metrics, historical context, sector-specific trends, and broader economic implications.

We also explore how these developments could influence the Federal Reserve's monetary policy decisions, particularly the widely anticipated interest rate cut at the September 17-18 FOMC meeting. As a real estate investment firm, we'll tie these insights to potential effects on the housing market, mortgage rates, and investment strategies.

Overview of the August 2025 Jobs Report

The numbers don't lie. The BLS report shows that hiring slowed down. Total nonfarm payroll employment increased by only 22,000 jobs, which is way less than the 75,000 jobs economists thought we'd get. That's the lowest increase we've seen in a while. The unemployment rate also went up to 4.3%, which is the highest it's been in nearly four years. That number used to be 3.7% at the start of the year.

And it's not just this month. The report also changed the numbers from the past few months, and they don't look good either. All of this makes it look like the labor market is in rougher shape than we thought. This isn't good news for anyone looking for a job or hoping for a strong economy.

Even though there are about 7.4 million on unemployment, the rate increase simply means that more people are becoming unemployed in the labor force. We're also seeing a decrease in wage growth now though we still have a long way to go. We're at 3.7% which can be expected to fall even farther.

The Labor Force Participation rate is just at 62.3% for now. We're still hoping for more to engage here because it affects our job rates severely.

Signs of Labor Market Weakening

So, what does this mean? It means the economy isn't as strong as we thought. Job growth is slowing down, unemployment is rising, and wages aren't growing as fast. That raises concerns about whether we'll see a recession. Let's dive deeper.

Here's a deeper look at some concerning trends:

- Rising Unemployment and Underemployment: The 4.3% unemployment rate is a worry. The broader U-6 measure, which includes part-time workers, stood at 8.1%—up from 7.4% a year ago. Long-term unemployment affected 1.9 million people, comprising 25.7% of the unemployed, and has risen by 385,000 over the year.

- Declining Job Openings and Hiring: Job openings are the lowest they've been since early 2021. People are quitting their jobs less often, which means they're less confident about finding a new one.

- Historical Context: The current weakening echoes pre-recession signals from 2007-2008, where gradual rises in unemployment preceded sharper downturns. However, unlike then, layoffs remain low, and the economy benefits from post-pandemic fiscal supports. Still, four consecutive months of subpar job growth in 2025—amid trade tariffs and immigration policies—has fueled debates about whether this is a “stall speed” or a temporary dip.

Experts are scratching their heads. Some believe this is just a temporary bump in the road, while others see it as a sign of bigger problems to come. I personally think it's a bit of both. Some industries are still doing well, but overall, the economy is losing steam. It's not quite time to panic, but it's definitely time to pay attention.

Sector-Wise Breakdown

Not all industries are created equal, and the August jobs report proves it. Some sectors are still adding jobs, while others are losing them.

Here's a quick breakdown:

| Sector | August Change | 12-Month Trend |

|---|---|---|

| Total Nonfarm | +22 | Little change since April |

| Total Private | +38 | +1,200 over year |

| Health Care | +31 | Below avg. +42/mo. |

| Social Assistance | +16 | Trending up |

| Leisure and Hospitality | +28 | +300 over year |

| Private Education and Health Services | +46 | Strong growth |

| Manufacturing | -12 | -78 over year |

| Federal Government | -15 | -97 since Jan. peak |

| Mining and Oil/Gas Extraction | -6 | Little change over year |

| Wholesale Trade | -12 | -32 since May |

| Professional and Business Services | -17 | Temp help -10 |

| Construction | -7 | Nonresidential +59 over year |

| Retail Trade | +11 | Mixed |

| Information | -5 | Declining |

| Financial Activities | -3 | Stable |

- Health Care and Social Assistance: These sectors are holding strong. They're adding jobs because people always need healthcare and support services — pandemic or not.

- Leisure and Hospitality: People are still wanting to enjoy themselves! But with growing prices, can it continue?

- Manufacturing: This sector is struggling and in fact, it's shedding jobs lately due to trade problems and other economic factors.

- Government Employment: The fed is just losing jobs.

This unevenness is a red flag. Some parts of the economy are doing alright, but others are struggling. It's like an engine sputtering – it might keep running for a while, but something needs to be fixed.

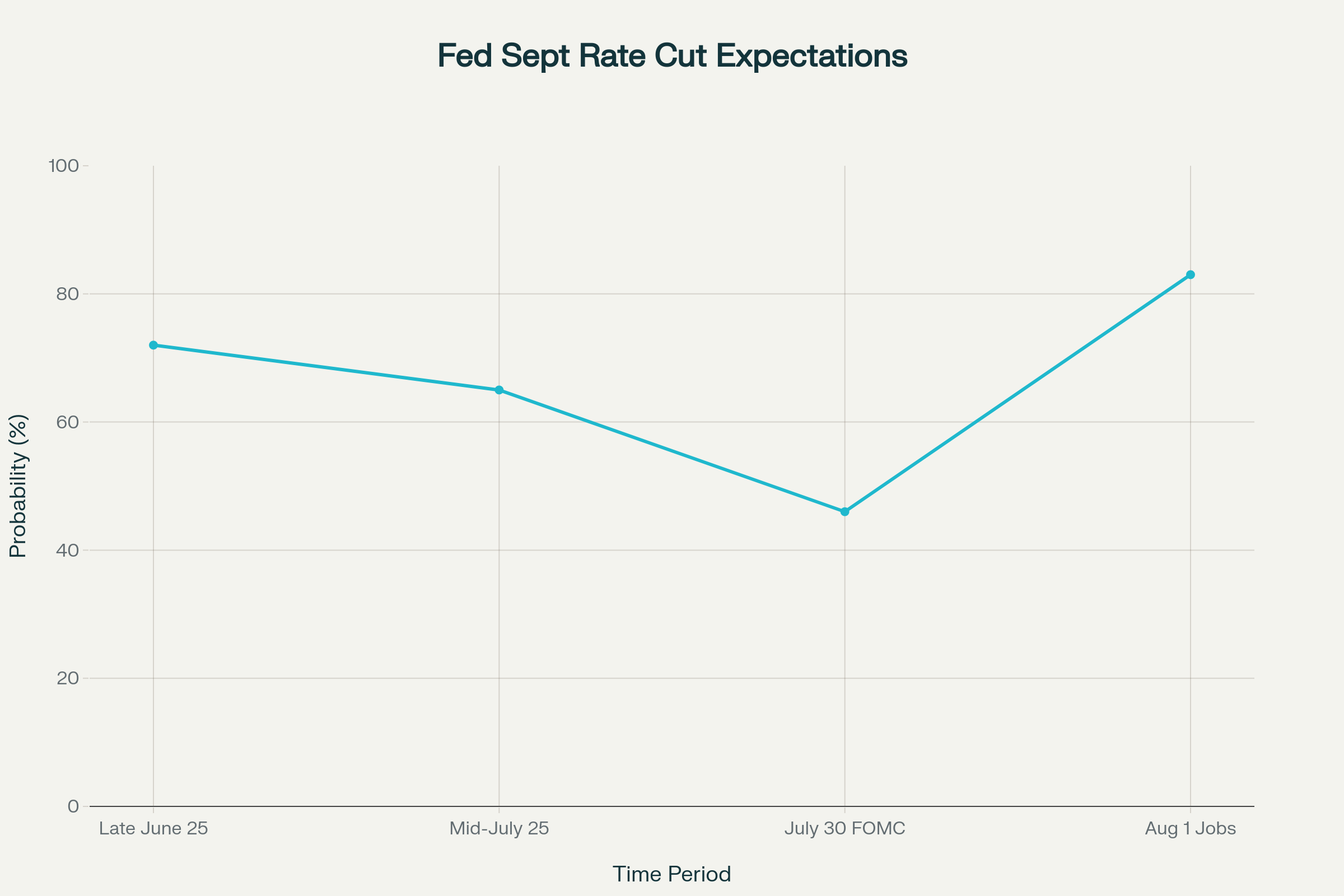

Potential Impact on Federal Reserve Interest Rate Cut

Here's where things get interesting. With the labor market looking shaky, the Federal Reserve is likely to cut interest rates soon. They're doing this to try and stimulate the economy – basically, make it cheaper for people and businesses to borrow money. That way, they will be encouraged to spend and invest, which can help boost economic growth.

The Federal Reserve is under a lot of pressure. Their job is to keep the economy stable, which means balancing inflation and employment. The recent jobs report gives them a reason to cut rates.

So what does that mean for you? If you are someone who takes loans, you can expect a lower rate. That's a good thing – cheaper borrowing.

Implications for Real Estate and Mortgage Markets

Now, let's talk real estate. As someone dedicated to real estate investment, I can say that interest rate cuts can impact the housing market and mortgage rates. When the Fed cuts rates, mortgage rates tend to follow. That means it becomes more affordable to buy a home.

Here's how it plays out:

- Lower Mortgage Rates: This is the most direct impact. Lower rates mean lower monthly payments, making homeownership more accessible.

- Increased Demand: Cheaper mortgages will drive up demand for housing. More people will want to buy, creating more competition.

- Potential Price Increases: If demand goes up and supply stays the same, prices rise. It's basic economics.

However, it's not all sunshine and roses. If the labor market continues to weaken, people might lose their jobs or become afraid of losing them. That can dampen demand, even if interest rates are low.

As always, the real estate market doesn't have a cut and dry answer.

Broader Economic and Policy Considerations

The U.S. jobs market report is arriving just as the discussions about tariffs and immigration are becoming more heated. Tariffs on imports can make it more expensive for businesses to produce goods and services, which can lead to job losses.

Keep in mind that there isn't going to be ONE solution here. Everyone is going to have to work together to create the best strategy.

In short, the latest jobs report sends a mixed signal. The labor market is showing signs of weakening, which could prompt the Federal Reserve to cut interest rates. That could boost the housing market and provide some relief to consumers and businesses. But it's not a guaranteed fix, and there are still plenty of risks on the horizon.

As a real estate investor, I keep my eye on these developments. I believe in finding cash-flowing rentals while monitoring employment trends. We have to be ready for whatever the economy throws our way. We’ll come out on the other side!

Work With Norada – Build Wealth

With economists warning of stagflation and weak GDP due to tariffs, now is the time to invest in stable, income-generating real estate for financial security.

Norada’s turnkey rental properties provide consistent cash flow and long-term wealth, no matter the economic climate.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Read More:

- Bond Market Today and Outlook for 2025 by Morgan Stanley

- The Risk of New Tariffs: Will They Crash the Stock Market and Economy?

- Stagflation Alert: Economist Survey Predicts Weak Q1 GDP Due to Tariffs

- Goldman Sachs Significantly Raises Recession Probability by 35%

- 2008 Crash Forecaster Warns of DOGE Triggering Economic Downturn

- Stock Market Predictions 2025: Will the Bull Run Continue?

- Stock Market Crash: Nasdaq 100 Tanks 3.5% Amid AI Concerns

- Stock Market Crash Prediction With Huge Discounts on Bitcoin, Gold, Houses

- S&P 500 Forecast for the Next Year: What to Expect in 2025?

- Stock Market Predictions for the Next 5 Years

- Echoes of 1987: Is Today’s Stock Market Crash Leading to a Recession?

- Is the Bull Market Over? What History Says About the Stock Market Crash

- Wall Street Bear Predicts a Historic Stock Market Crash Like 1929

- Economist Predicts Stock Market Crash Worse Than 2008 Crisis

- Next Stock Market Crash Prediction: Is a Crash Coming Soon?

- Stock Market Crash: 30% Correction Predicted by Top Forecaster