As of November 14, 2025, today's mortgage rates are holding remarkably steady, lingering close to the lowest points we've seen so far this year. This stability is welcome news for many hoping to buy a home or refinance an existing mortgage, even if it doesn't signal a dramatic drop.

Today's Mortgage Rates November 14: 30-Year FRM Drops to 6.10%, Close to Lowest Point

According to the latest data from Freddie Mac, the national average for a 30-year fixed mortgage has nudged up just two basis points to 6.24%, which is still a significant improvement, coming in more than half a percentage point lower than this time last year. For those eyeing shorter loans, the 15-year fixed rate saw a slight dip of one basis point to 5.49%, putting it a solid 49 basis points below its 2024 mark.

From my perspective, seeing these rates hover in the low 6% range is a sign of a market trying to find its footing. After the rollercoaster ride of the past few years, this kind of predictability, while not thrilling, is what many buyers and homeowners need to make informed decisions. It suggests that the forces influencing mortgage rates are in a more balanced state, a welcome change from the rapid shifts we've experienced.

What the Numbers Are Saying Today

To get a clearer picture of where things stand right now, I've pulled together the most recent figures from Zillow. These national averages give us a solid benchmark, but remember that your individual rate can vary based on your credit score, down payment, and other factors.

Here’s a look at the current national average mortgage rates:

| Loan Type | Interest Rate |

|---|---|

| 30-year fixed | 6.10% |

| 20-year fixed | 6.08% |

| 15-year fixed | 5.60% |

| 5/1 ARM | 6.39% |

| 7/1 ARM | 6.51% |

| 30-year VA | 5.55% |

| 15-year VA | 5.33% |

| 5/1 VA | 5.44% |

As you can see, the 30-year fixed rate is just slightly below the Freddie Mac figure, sitting at 6.10%. The 15-year fixed is also a bit lower at 5.60%. It’s interesting to note the slight difference between the 20-year fixed and the 30-year fixed rate, with the 20-year being just a hair lower at 6.08%. This can sometimes happen as lenders price different loan terms.

Refinancing: Still a Mixed Bag

For folks looking to refinance their current mortgage, the picture is a bit more nuanced. Many homeowners who stood to benefit significantly from refinancing have already locked in lower rates during previous periods.

Here are the current national average refinance rates, again from Zillow:

| Loan Type | Interest Rate |

|---|---|

| 30-year fixed | 6.25% |

| 20-year fixed | 6.04% |

| 15-year fixed | 5.73% |

| 5/1 ARM | 6.56% |

| 7/1 ARM | 6.84% |

| 30-year VA | 5.78% |

| 15-year VA | 5.57% |

| 5/1 VA | 5.39% |

Notice that the average refinance rates are generally a touch higher than the rates for purchasing a new home. For example, the 30-year fixed refinance rate is at 6.25%, which is higher than the 6.10% purchase rate. This difference is often due to how lenders structure refinance loans and the associated fees. While these rates are still much better than year-ago levels, they might not be compelling enough for many to make the move, especially if they already have a very low rate locked in from a few years ago. Refinance applications did see a small dip last week, which supports this observation.

Why Are Rates Not Dropping More? Affordability and Market Influences

It's easy to look at these rates and wish they were even lower, especially after the historically low rates we saw during the pandemic. But it's crucial to remember that those sub-3% rates were an anomaly, and it's highly unlikely we'll see them again anytime soon.

The main challenge right now isn't just mortgage rates; it's also home prices. Even with rates in the low 6% range, the combination can still make homeownership a stretch for many. This persistent affordability concern is a major factor keeping the market from heating up too quickly.

However, even small movements in rates can make a difference. Last week, we saw a notable increase in mortgage applications to buy a home, up by nearly 6%. This clearly indicates that when rates hover near the year's lows, buyers start to get more active. It’s a powerful reminder of how sensitive the housing market is to interest rate fluctuations.

Related Topics:

Mortgage Rates Trends as of November 13, 2025

Mortgage Rate Predictions for the Next 30 Days: Nov 10 to Dec 10, 2025

Mortgage Rates Predictions for the Next 12 Months: Nov 2025 to Nov 2026

Mortgage Rates Predictions for Next 90 Days: October to December 2025

What's Next? Fed Watch and Policy Ideas

The economic picture continues to be influenced by the Federal Reserve's monetary policy. After making rate cuts in September and October, speculation is mounting about what will happen at their December meeting. While the Fed doesn't directly set mortgage rates, their decisions on the federal funds rate ripple through the economy and influence things like the 10-year Treasury yield, which is a key benchmark for mortgage rates.

Currently, Wall Street traders are less confident about another rate cut happening in December. This uncertainty can contribute to the stability we're seeing in mortgage rates.

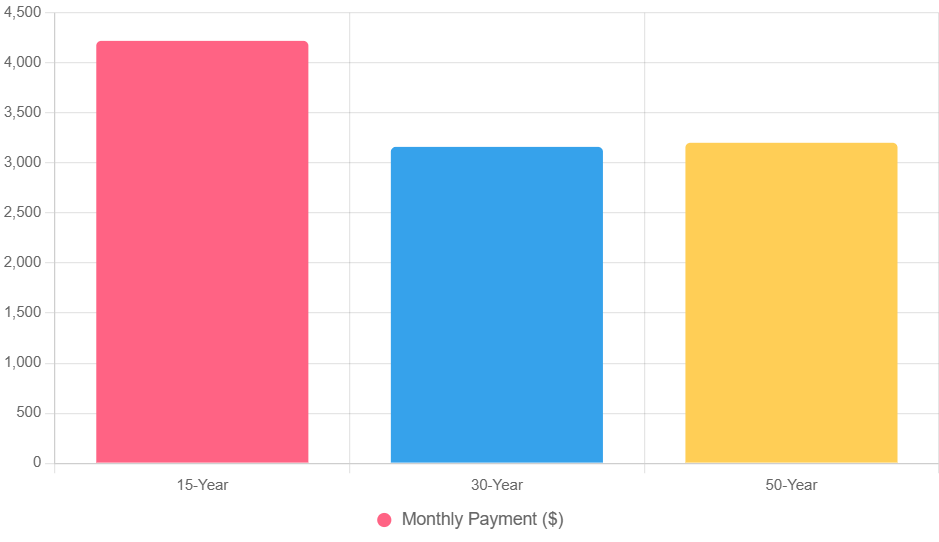

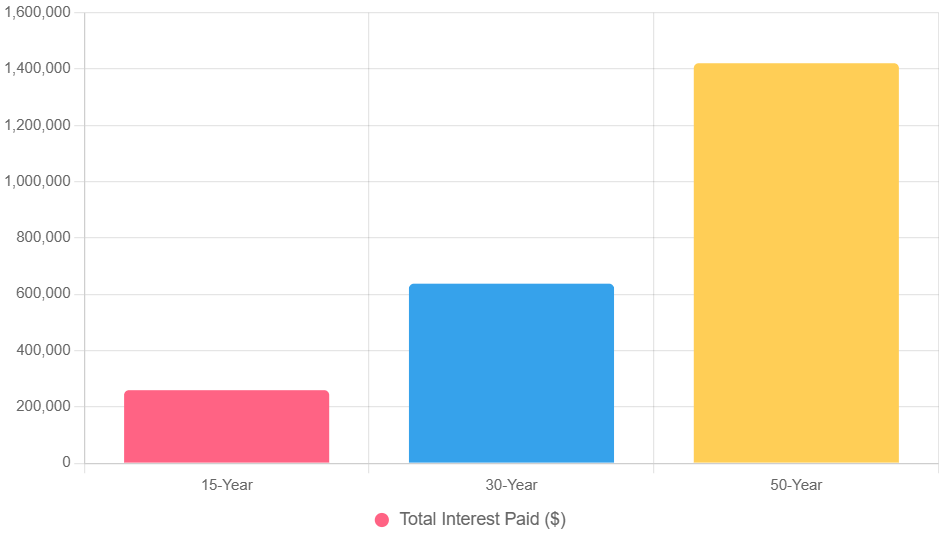

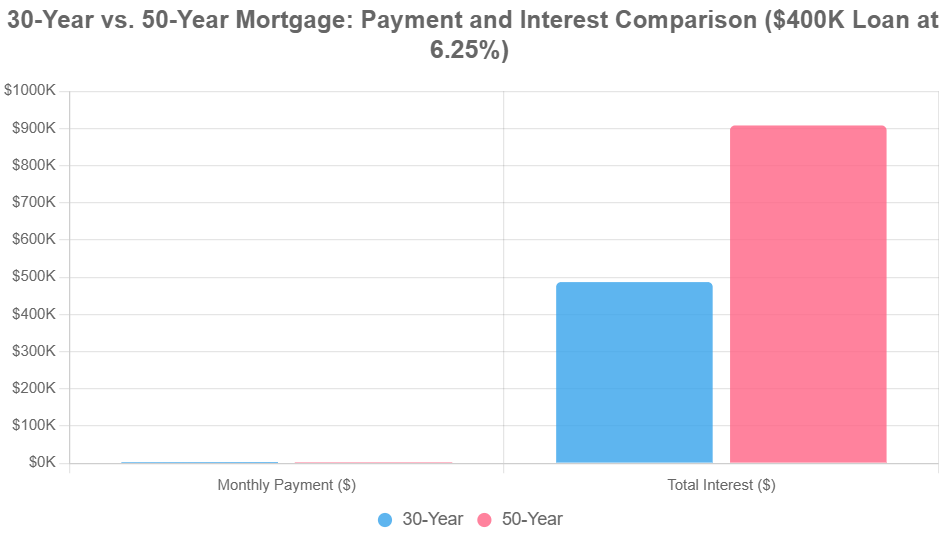

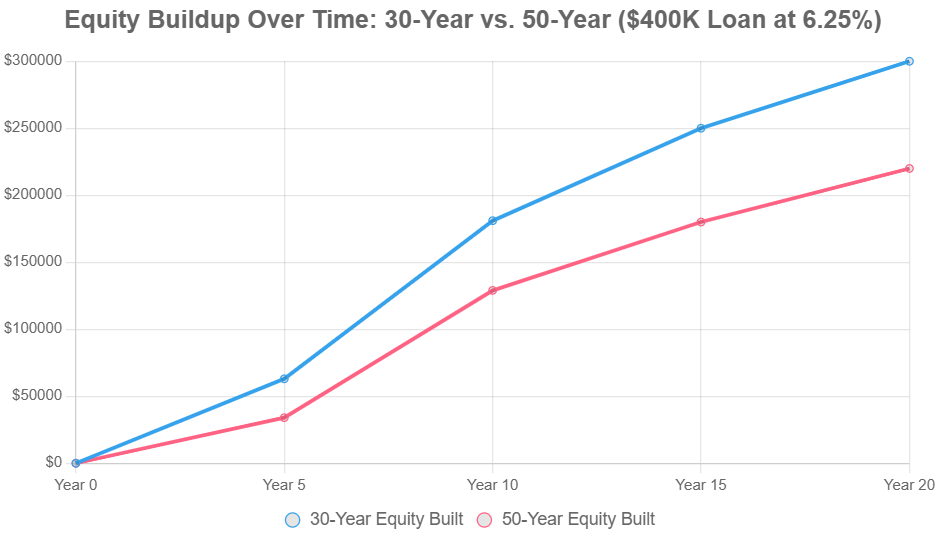

On the policy front, there's been discussion about proposals like the Trump administration considering 50-year mortgages to tackle housing affordability. While this idea aims to reduce monthly payments by extending the loan term, it also means paying more interest over time. Experts like Logan Mohtashami suggest that such a long-term mortgage might not fundamentally alter the market and that current rates in the low 6% range are more critical for market stability. I personally believe that while innovative solutions are worth exploring, focusing on sustainable home prices and accessible rates is paramount. Stretching payments over 50 years carries its own set of risks and could lead to homeowners being underwater on their mortgages for longer periods.

Looking Ahead: Forecasts for 2025 and Beyond

So, what do the experts predict for the rest of 2025 and into 2026? Forecasts from major housing organizations like Fannie Mae and the Mortgage Bankers Association generally agree that we'll likely see rates stay above 6% through the end of this year and well into next year.

Fannie Mae offers a slightly more optimistic outlook, suggesting that rates could potentially dip below 6% by the end of 2026. This indicates a gradual return to more balanced conditions rather than a sharp decline. Personally, I see this as a realistic expectation. The era of ultra-low rates is behind us, but the market is adapting to a new normal where rates are higher but more stable, allowing for more predictable planning for buyers and sellers.

In summary, today, November 14, 2025, offers a stable albeit slightly higher mortgage rate environment compared to the very recent past, holding near 2025 lows. While affordability remains a concern, the current rates are a catalyst for buyer activity and a point of consideration for homeowners contemplating refinancing.

Secure Your Retirement with Cash-Flowing Rental Properties

Turnkey real estate offers a low-hassle way to generate passive income and build long-term financial security—perfect for retirement-focused investors.

Norada Real Estate helps you invest in stable, high-demand markets that deliver consistent monthly cash flow and equity growth over time.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?