As the year draws to a close, today’s mortgage rates on December 24, 2025, by Zillow show a delightful stillness, offering a much-needed breather for anyone looking to buy a home or refinance their current mortgage. The average 30-year fixed mortgage rate is holding steady at 6.11%, and the 15-year fixed rate is at 5.50%. This lack of significant movement means borrowers have the perfect opportunity to navigate the market, compare offers, and potentially lock in a rate that truly works for them without the pressure of sudden changes.

Today’s Mortgage Rates, Dec 24: With Rates Steady, Borrowers Gain Leverage

For those of us who follow the housing market, this period of stability isn't just about numbers; it's about providing a sense of predictability that's been a bit rare lately. It feels like the market is taking a collective deep breath before diving into whatever the new year holds.

Where Do Rates Stand Today?

Let's break down the national averages as of Wednesday, December 24, 2025, rounded to the nearest hundredth. It’s important to remember these are averages, and your personal rate might be slightly different based on your unique financial picture.

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.11% |

| 20-year fixed | 6.03% |

| 15-year fixed | 5.50% |

| 5/1 ARM | 6.19% |

| 7/1 ARM | 6.35% |

| 30-year VA | 5.56% |

| 15-year VA | 5.31% |

| 5/1 VA | 5.44% |

(Source: Zillow, December 24, 2025)

When I look at these numbers, I see a market that’s not causing undue stress. The slight difference between the 30-year fixed and 20-year fixed, for instance, suggests that borrowers willing to shorten their loan term by a decade can indeed see some savings. And the VA loan rates remain incredibly competitive, which is fantastic for our service members and veterans.

Refinancing: Is Now the Time?

For homeowners considering a refinance, the picture looks very similar, with rates remaining remarkably stable. Here are the average refinance rates:

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.13% |

| 20-year fixed | 6.04% |

| 15-year fixed | 5.59% |

| 5/1 ARM | 6.42% |

| 7/1 ARM | 6.63% |

| 30-year VA | 5.65% |

| 15-year VA | 5.42% |

| 5/1 VA | 5.43% |

You'll notice refinance rates are typically a hair higher than purchase rates, which is normal. However, with the current stability, it's a great time to see if refinancing can help you lower your monthly payments, shorten your loan term, or tap into your home's equity.

The Gift of Stability: What It Means for You

This period of calm in mortgage rates is like finding an unexpected gift under the tree. Here’s what it translates to for you as a borrower:

- Predictable Planning: No need to constantly check rates. You can make your financial decisions with confidence, knowing that major rate hikes or drops aren't likely to catch you off guard today. This allows for more solid budgeting and less anxiety.

- Time to Shop Smart: When rates are stable, lenders often become more competitive. This means you have the perfect window to reach out to multiple lenders, compare their specific offers—not just rates, but also fees and closing costs—and negotiate for the best deal. Don't be afraid to ask questions and get quotes from at least three to four different places.

- Reduced Urgency: You can take your time to review all the paperwork, understand your loan options, and make sure you're comfortable with the terms. This is crucial for such a significant financial commitment.

Choosing Your Perfect Mortgage Fit

Deciding on the right loan type is as important as finding the right rate. Here’s a quick refresher on what works best for different needs:

- 30-Year Fixed Mortgage: This is the classic. It’s ideal if you prioritize predictable monthly payments and want to spread out the cost of your home over a long period, making your monthly housing expense more manageable.

- 15-Year Fixed Mortgage: If you're financially comfortable and want to be mortgage-free sooner, this is your go-to. You’ll pay more each month, but you'll save a significant amount in interest over the life of the loan and build equity much faster.

- Adjustable-Rate Mortgages (ARMs): These loans start with a lower interest rate for a set period (like 5 or 7 years) before the rate adjusts based on market conditions. Today, with the ARM rates shown being higher than fixed options, they are less appealing for most buyers unless you have a very specific, short-term plan for the home.

- VA Loans: For our veterans and active-duty military, these loans are a fantastic benefit. They often come with no down payment requirement and very competitive interest rates, making homeownership more accessible.

Putting the Numbers into Perspective: A Real-World Example

Sometimes, seeing the actual dollar impact makes all the difference. Let’s look at a hypothetical $300,000 loan for a 30-year fixed mortgage.

- If the rate were 6.04% (like last week): Your monthly principal and interest payment would be approximately $1,805.

- At today’s rate of 6.11%: Your monthly principal and interest payment would be about $1,819.

This might seem like a small difference, but:

- That’s about $14 more per month.

- Over a year, it adds up to roughly $168 more.

- And over the entire 30-year loan, that’s over $5,000 in extra interest paid.

While this illustrates that even small rate changes matter, the $5,000 difference is a tiny fraction of the overall loan cost. The stability we’re seeing offers a better chance to secure a rate you're comfortable with today, rather than worrying about a sudden jump that could cost you far more over time.

Recent Trends and the Road Ahead

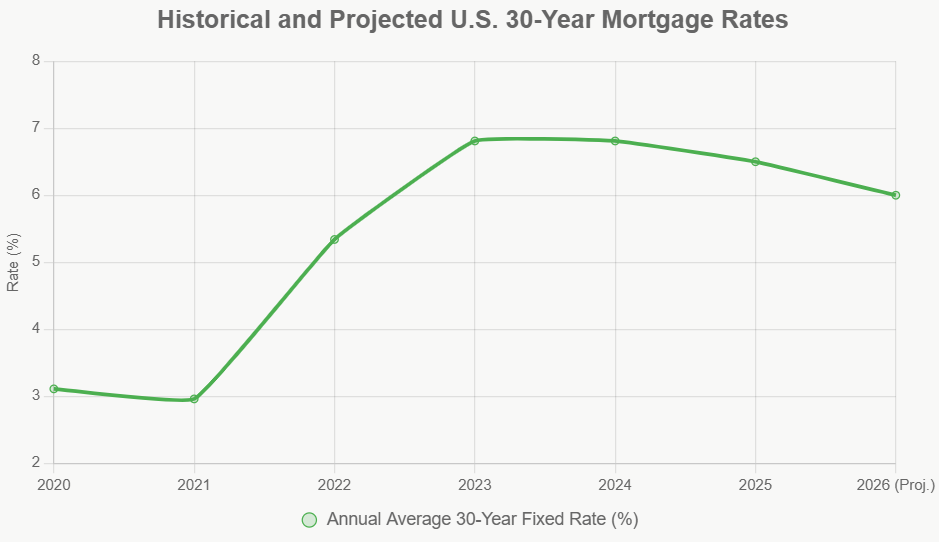

Looking back, mortgage rates have been in a bit of a holding pattern for the past few months. They’ve hovered within a relatively narrow range, certainly lower than the peaks we saw earlier in 2025, which has been a welcome relief.

What drives these rates? Primarily, it’s the yield on the 10-year Treasury notes, our collective expectations about inflation, the overall health of the economy, and, of course, actions from the Federal Reserve. While the Fed has been making adjustments to its benchmark rate, mortgage rates don't always move in perfect lockstep. Often, the market has already priced in anticipated changes.

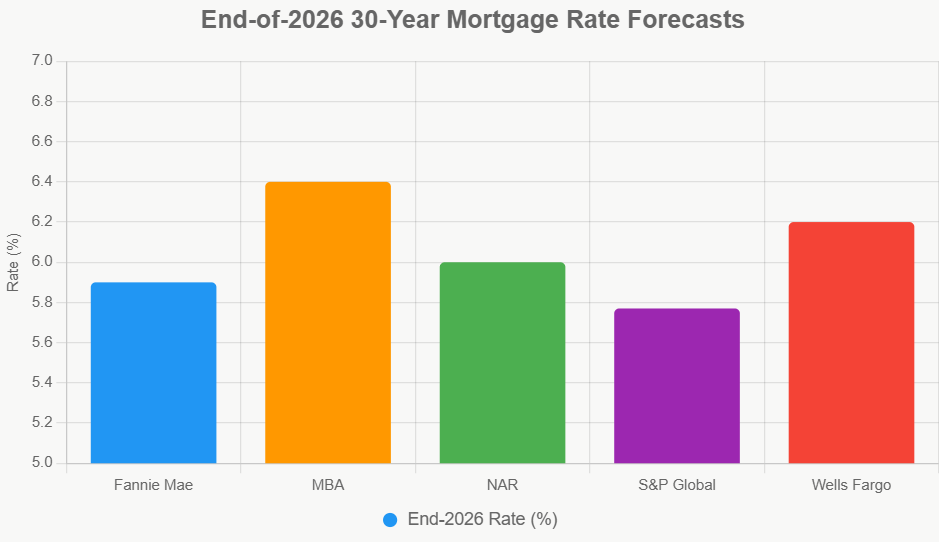

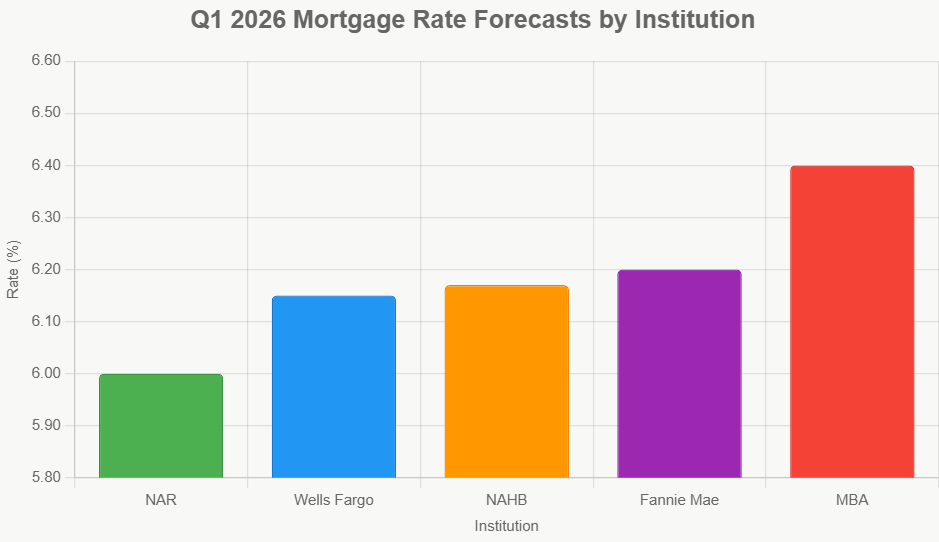

As for the outlook into 2026, most experts I’ve spoken with and read about anticipate that rates will likely remain above the 6% mark for the foreseeable future. A gradual decline is possible if inflation continues to cool and the job market softens a bit, but a return to the super-low rates of the pandemic era (think sub-3%) is pretty much off the table.

Strategies for Securing a Better Rate

Even in a stable market, there are always ways to potentially snag a better mortgage rate. My advice is always focused on making yourself the most attractive borrower possible:

- Boost Your Credit Score: Aim for that magic number of 740 or higher. This is the golden ticket for the best rates. Make sure all your bills are paid on time—that’s the most significant factor affecting your score. Also, try to keep your credit card balances low, using ideally less than 30% of your available credit.

- Increase Your Down Payment: A bigger down payment reduces risk for the lender and can help you avoid Private Mortgage Insurance (PMI), saving you money both upfront and over time.

- Lower Your Debt-to-Income Ratio (DTI): Lenders love borrowers with low DTI. Try to keep your total monthly debt payments below 36% of your gross monthly income. This can involve paying down debt or increasing your income.

- Shop Around and Negotiate: This is huge! Don't choose the first lender you talk to. Get quotes from several different banks, credit unions, and mortgage brokers. Compare not just the interest rate but also the annual percentage rate (APR), which includes fees, and the closing costs. You have leverage when rates are stable, so don't be afraid to ask for a better deal.

The Bottom Line on December 24th

As we wrap up this day, December 24, 2025, the mortgage and refinance rate picture is reassuringly unchanged. The 30-year fixed purchase rate stands at 6.11%, the 15-year fixed purchase rate is at 5.50%, and the 30-year fixed refinance rate is at 6.13%.

This period of calm is, in my opinion, a fantastic opportunity. It’s the ideal time to do your homework, compare offers from various lenders, and confidently secure a mortgage that aligns perfectly with your dreams and financial stability. Happy house hunting or refinancing!

VS

Two solid options: Alabama’s affordable new build with steady returns vs Tennessee’s larger home with higher cash flow. Which fits YOUR investment strategy?

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Invest in Fully Managed Rentals for Smarter Wealth Building

With mortgage rates dipping to their lowest levels in months, savvy investors are seizing the opportunity to lock in financing.

By securing favorable terms now, you can also maximize immediate cash flow while positioning yourself for stronger long‑term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income while borrowing costs remain historically low.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?