The good news for anyone hoping to buy a home or refinance their existing mortgage is that mortgage rates are predicted to drop to the high 5% range by the end of 2026. This anticipated decline, supported by a consensus of expert forecasts, offers a much-needed glimmer of hope in a housing market that has felt increasingly out of reach for many. While the exact path remains subject to economic winds, the general direction appears headed toward more affordable borrowing.

Mortgage Rates Set to Drop to the High 5% Range by Late 2026

As we wrap up 2025, the average 30-year fixed mortgage rate is sitting around a more manageable 6.21%, a welcome step down from the 6.72% we saw just a year ago. This feels like a breath of fresh air after the volatility of recent years, where rates averaged roughly 6.5% in 2025, down from 6.8% in 2024.

For years, soaring home prices combined with high interest rates have made owning a home feel like a distant dream for many families. The thought of monthly payments on a median-priced home exceeding $2,200—a shocking 50% jump from pre-pandemic levels—has been a source of major stress. But this prediction of rates in the high 5s by the end of 2026 suggests relief may be on the horizon. It's not just about getting a better deal; it's about re-opening the doors to homeownership for a significant portion of the population.

A Look Back: The Rollercoaster of Recent Rates

To understand where we're going, it pays to look at how we got here. The last five years have been a wild ride for mortgage rates, influenced by everything from the global pandemic to surges in inflation and shifts in Federal Reserve policy.

Remember those incredible, near-zero rates during the pandemic? They fueled a buying spree that was, frankly, unsustainable. Then came the rapid rate hikes aimed at taming inflation, which definitely cooled things down but also created significant affordability challenges.

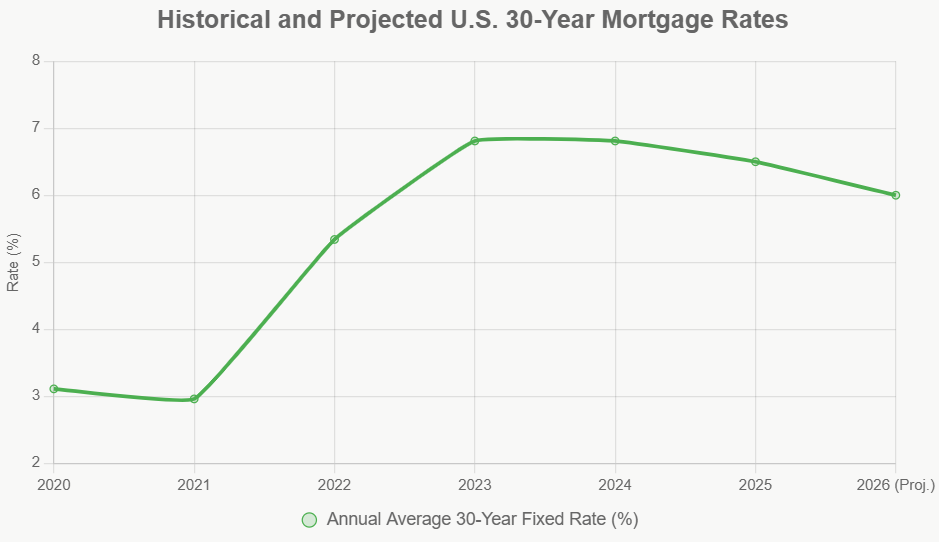

Here's a quick recap of the annual average rates for a 30-year fixed mortgage:

| Year | Annual Average 30-Year Fixed Rate | Key Events |

|---|---|---|

| 2020 | 3.11% | Pandemic stimulus; rates hit historic lows. |

| 2021 | 2.96% | Continued easy money; home sales boomed. |

| 2022 | 5.34% | Fed hikes to combat inflation; rates doubled. |

| 2023 | 6.81% | Peak inflation; affordability crisis deepened. |

| 2024 | 6.81% | Stubborn inflation kept rates elevated. |

| 2025 | ~6.50% (estimated) | Modest Fed cuts; rates begin easing. |

Data sourced from Freddie Mac and Fannie Mae reports for historical periods; estimates for recent years.

This history shows just how sensitive mortgage rates are to what's happening in the broader economy. The current dip from the peak isn't the end of the story; it's more like the beginning of a slow, steady descent that experts believe will continue into 2026.

What's Driving the Predicted Drop?

So, what's behind this optimistic forecast for lower rates? It's a confluence of several key economic factors that are expected to play out over the next year and a half. If these trends hold, we should see mortgage rates moving into that desirable high 5% range.

- Federal Reserve Rate Cuts: The Federal Reserve has been using interest rates as its main tool to control inflation. As inflation shows signs of cooling, the Fed is expected to start cutting its benchmark interest rate. We’ve already seen some cuts, and the consensus is that there will be more in 2025 and into 2026. When the Fed cuts rates, it usually makes borrowing money cheaper across the board, including for mortgages. Expert projections suggest the federal funds rate could be around 2.9% by 2026, which is a significant shift from where it has been. This typically translates into lower mortgage rates, as they tend to follow the yields on longer-term government bonds, like the 10-year Treasury note.

- Moderating Inflation: This is arguably the biggest driver. Inflation has been a concern for a while, pushing rates up to combat rising prices. However, forecasts from institutions like Fannie Mae project inflation to cool down to around 2.7% by the end of 2026. When inflation is under control, there's less pressure on the Fed to keep interest rates high, and creditors become more willing to lend money at lower rates over longer periods.

- Stable Economic Growth: The ideal scenario for lower rates is a “soft landing”—where the economy slows down just enough to curb inflation without tipping into a full-blown recession. Projections for GDP growth in 2026 are around 1.9%, which is robust enough to keep things humming but not so strong that it fuels runaway price increases. Unemployment is expected to rise slightly to around 4.2%, which could further encourage the Fed to lower rates.

- Housing Supply Increasing (Slowly): While home prices have been a major hurdle, there's a hopeful sign that housing inventory might increase. Projections suggest a 10%–15% rise in available homes. This could help ease some of the intense price pressure we've seen, making affordability a bit better even if rates don't drop dramatically.

Expert Forecasts: A Consensus with Nuances

While the general trend is optimistic, it's always wise to look at what different experts are saying. There's a good amount of agreement that we'll see rates ease, but the exact number and the speed of the decline can vary.

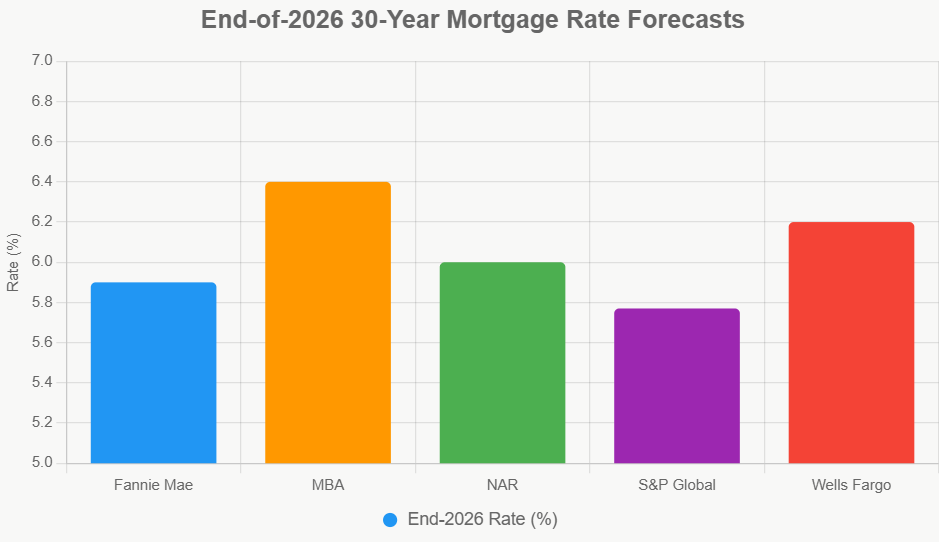

Here’s a snapshot of some forecasts for the 30-year fixed mortgage rate:

| Forecaster | Q1 2026 | Q2 2026 | Q3 2026 | Q4 2026 | Annual Avg. (2026) |

|---|---|---|---|---|---|

| Fannie Mae | 6.2% | 6.1% | 6.0% | 5.9% | 6.0% |

| Mortgage Bankers Assoc. (MBA) | 6.4% | 6.4% | 6.4% | 6.4% | 6.4% |

| National Assoc. of Realtors (NAR) | 6.0% | 6.0% | 6.0% | 6.0% | 6.0% |

| S&P Global | —- | —- | —- | —- | ~5.77% |

| Wells Fargo | 6.15% | 6.15% | 6.20% | 6.20% | 6.2% |

Note: Freddie Mac has indicated a general expectation for rates to be below 6% for the year, but specific quarterly predictions are not as granular.

As you can see, Fannie Mae and NAR are quite optimistic, predicting rates to touch the high 5% range by the end of 2026. The MBA is a bit more cautious, holding steady at 6.4%, and Wells Fargo falls in the middle. S&P Global's annual average prediction is the most aggressive, suggesting rates could dip into the mid-5% range.

What causes these differences? It often comes down to how quickly different economists believe inflation will fall, how aggressively the Fed will cut rates, and how resilient the overall economy remains. For instance, the MBA might be factoring in stronger economic growth or stickier inflation than Fannie Mae.

What This Means for You: Buyers and Refinancers

This projected drop in mortgage rates isn't just an abstract economic indicator; it has real, tangible impacts on people looking to buy a home or refinance their existing mortgage.

For Homebuyers:

- Increased Affordability: A rate dip to, say, 5.9% could make a significant difference. The National Association of Realtors estimates this could add over 1.5 million households who now qualify for a mortgage that they couldn't before. This means more people can enter the market.

- Boost in Home Sales: With improved affordability, sales could see a noticeable bump. NAR predicts existing home sales could rise by 14% to about 4.3 million units by late 2026. Imagine more homes changing hands as buyers take advantage of better borrowing costs.

- Offsetting High Home Prices: While lower rates are great, home prices have been stubbornly high. While the pace of price increases is expected to slow (perhaps to 2%–3% annually), they might still climb, meaning the savings from lower rates might not completely negate the cost of the home itself. Even so, lower monthly payments on a larger loan amount still offer significant relief.

- First-Time Buyers: Lower rates are particularly crucial for first-time homebuyers who often have tighter budgets. Programs like FHA and VA loans, which track conventional mortgage rates, could become even more attractive.

For Refinancers:

- Significant Savings: If you have a mortgage with a rate above, say, 6.5%, dropping to 5.9% could lead to substantial monthly savings. For a $300,000 loan, that could mean saving around $110 per month, adding up to over $39,000 across the life of the loan.

- Refinance Boom: Fannie Mae projects a 37% surge in refinance volume, reaching approximately $724 billion. This indicates that a lot of people will likely look to lock in these lower rates and reduce their monthly housing costs.

- Breaking Even: It's important for those considering refinancing to look at the closing costs involved. While the monthly savings are enticing, you'll want to make sure you plan to stay in your home long enough for the savings to outweigh the upfront expenses.

Navigating the Road Ahead: What Should You Do?

Knowing that rates are predicted to drop is one thing; acting on it is another. Here are a few thoughts from my experience:

- If You're Buying Soon: If you're already in the market and have found a home you love, don't necessarily wait indefinitely for rates to hit rock bottom, especially if your current rate options are much higher. You might consider locking in a rate now if you find a deal that works for you. Mortgages are long-term commitments, and securing a good rate now, even if it's a bit higher than the projected future low, could still be better than waiting and risking rising rates or missing out on a home. Sometimes, the best time to buy is when you find the right home and it fits your budget today.

- If You're Planning to Refinance: Keep a close eye on rate movements. As rates fall into the high 5% range, it might be the perfect time to evaluate your current loan. Reach out to a lender, get quotes, and do the math to see if refinancing makes sense for your financial situation. Even a small drop can be significant over time.

- Stay Informed: This isn't a static situation. Follow economic news, particularly reports on inflation and Federal Reserve announcements. Resources like Freddie Mac's Primary Mortgage Market Survey and reports from Fannie Mae and NAR are excellent for staying up-to-date.

While the prediction of mortgage rates falling to the high 5% range by the end of 2026 is cause for optimism, it's essential to remember that these are forecasts. Economic conditions can change, and unforeseen events can impact rate movements. However, the current data and expert opinions provide a strong indication of a more favorable lending environment in the not-too-distant future. This could be the break many have been waiting for to achieve their homeownership dreams or improve their financial situation through refinancing.

VS

Two affordable rentals with solid returns: Birmingham’s steady performer vs St. Louis’s higher cap rate. Which fits YOUR investment strategy?

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Invest in Fully Managed Rentals for Smarter Wealth Building

With mortgage rates dipping to their lowest levels in months, savvy investors are seizing the opportunity to lock in financing.

By securing favorable terms now, you can also maximize immediate cash flow while positioning yourself for stronger long‑term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income while borrowing costs remain historically low.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?