If you're keeping an eye on mortgage rates, especially for a 15-year fixed-rate mortgage, here's the scoop: As of today, August 9, 2025, the average 15-year mortgage rate today increased from 5.78% to 5.80%. While a slight increase, even small fluctuations can impact your monthly payments and overall borrowing costs. Let's dive deeper into what this means for you and the broader housing market.

Mortgage Rates Today: 15-Year FRM Jumps to 5.80% – August 9, 2025

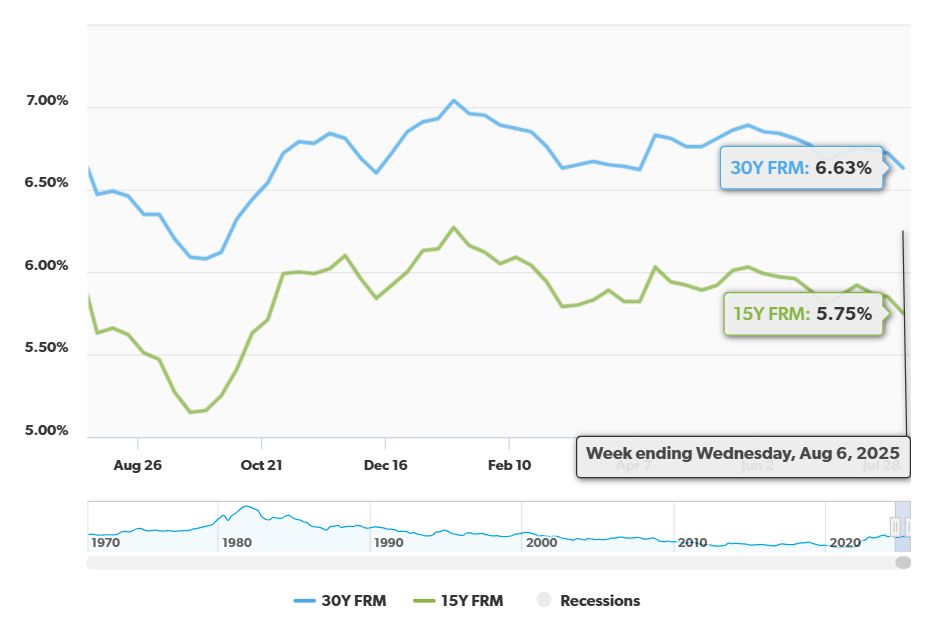

What's Happening with Mortgage Rates in General?

It's not just the 15-year rate that's moving. Here’s a quick snapshot of where other key mortgage rates stand:

- 30-Year Fixed Rate: 6.71% (up 1 basis point)

- 5-Year ARM: 7.34% (up 3 basis points)

To give you a complete picture, here is a tabular representation:

| Loan Program | Rate | 1 Week Change | APR | 1 Week Change |

|---|---|---|---|---|

| 30-Year Fixed Rate | 6.71% | Down 0.12% | 7.20% | Down 0.08% |

| 20-Year Fixed Rate | 6.65% | Up 0.19% | 6.93% | 0.00% |

| 15-Year Fixed Rate | 5.80% | Down 0.08% | 6.12% | Down 0.06% |

| 10-Year Fixed Rate | 5.48% | Down 0.26% | 5.84% | Down 0.28% |

| 7-year ARM | 7.08% | Down 0.14% | 7.59% | Down 0.29% |

| 5-year ARM | 7.34% | Down 0.21% | 7.87% | Down 0.04% |

| 3-year ARM | — | 0.00% | — | 0.00% |

Table: Conforming Loans – Source: Zillow

Why Focus on the 15-Year Fixed-Rate?

The 15-year fixed-rate mortgage is popular for a few key reasons:

- Faster Equity Building: You pay off your home in half the time compared to a 30-year mortgage, which means you build equity much faster.

- Lower Interest Rate: Historically, 15-year mortgages have lower interest rates than their 30-year counterparts. This can save you a significant amount of money over the long term.

- Higher Monthly Payments: The trade-off is that your monthly payments are higher. You need to be comfortable with a larger payment to take advantage of the shorter term and lower rate.

I have personally seen many families benefit from the 15-year mortgage option, especially when they are in a financially stable position to handle the higher monthly payments. The long-term savings and quicker path to full homeownership are significant advantages.

The Federal Reserve and its Impact

The Federal Reserve (the Fed) plays a HUGE role in determining where mortgage rates go. To provide some background, let's review their recent activities:

- 2021-2023: The Fed aggressively increased interest rates (by 5.25 percentage points!) to fight inflation, causing mortgage rates to climb to 20-year highs.

- Late 2024: After over a year of holding steady, the Fed cut rates three times, lowering the federal funds rate by 1 percentage point.

- 2025 (So Far): The Fed has paused rate adjustments, keeping rates steady through July.

So, What’s the Fed Doing Now?

This is where things get interesting. The Fed is in a bit of a tricky spot.

- Inflation is Still a Concern: They want to keep inflation under control. It’s sitting around 2.7%, which is a bit higher than they'd like.

- Economic Growth is slowing: The economy isn't growing as fast as it used to.

This has led to some internal disagreements within the Fed. Some members want to cut rates to boost the economy, while others are worried about fueling inflation.

For the mortgage market, this means rates are kind of stuck in limbo. 30-year fixed rates have been hovering around 6.8%, and the Fed's actions (or inactions) are a major reason why.

Related Topics:

Mortgage Rates Predictions for the Next 60 Days

Mortgage Rates Predictions for the Next 6 Months: August to December 2025

What to Expect in the Near Future Here’s what I am watching out for:

- September 16-17 Meeting: The Fed will release updated economic forecasts. This meeting will be crucial for setting expectations.

- December Meeting: If the Fed doesn't act in September, this is likely their last chance to cut rates in 2025.

The Fed is projecting two rate cuts in 2025. If these cuts happen, we could see mortgage rates fall towards 6% by the end of the year. However, it's all about timing.

What Does This Mean for You?

- If You're Buying Now: Understand that rates are still relatively high. Shop around for the best deals and consider all your options. The signals from the Fed suggests some relief is on the horizon.

- If You're Thinking of Refinancing: Keep a close eye on the Fed's decisions in September and December. If you currently have something greater than 7%, these meetings could present opportunities.

In Conclusion

The 15-year mortgage rate moving up slightly to 5.80% is part of a bigger picture influenced by the Federal Reserve's decisions and the overall economic climate. Keep informed, stay flexible, and talk to a financial advisor to make the best decisions for your situation.

Capitalize Amid Rising Mortgage Rates

With mortgage rates expected to remain high in 2025, it’s more important than ever to focus on strategic real estate investments that offer stability and passive income.

Norada delivers turnkey rental properties in resilient markets—helping you build steady cash flow and protect your wealth from borrowing cost volatility.

HOT NEW LISTINGS JUST ADDED!

Speak with a seasoned Norada investment counselor today (No Obligation):

(800) 611‑3060

Also Read:

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?