The onset of a recession in the United States is officially determined by the National Bureau of Economic Research (NBER), which defines a recession as “a significant decline in economic activity spread across the economy, lasting more than two quarters which is 6 months, normally visible in real gross domestic product (GDP), real income, employment, industrial production, and wholesale-retail sales.”

When Did the Recession Start in the US?

The most recent recession, often referred to as the “Great Recession,” began in December 2007, according to the NBER. This was after two consecutive quarters of declining economic growth, marking the start of the worst economic downturn since the Great Depression.

The Great Recession's roots can be traced back to 2006 when housing prices started to fall, leading to a subprime mortgage crisis. By August 2007, the Federal Reserve had to intervene by adding liquidity to the banking system. The situation escalated, and by the end of 2007, the economy was in a full-blown recession.

Impact on the Job Market and Housing

Understanding the start dates of recessions is crucial for economic analysis and planning. It helps economists, policymakers, and the public to evaluate the health of the economy and to devise strategies for recovery. The NBER's role in this process is pivotal as it provides a historical record of the U.S. economic cycles based on a variety of economic indicators.

It's also important to note that the impact of such economic downturns extends beyond just financial markets and into the lives of everyday citizens. The Great Recession led to a significant increase in unemployment, with millions of Americans losing their jobs. The unemployment rate, which had been at 4.7% in November 2007, peaked at 10% in October 2009, reflecting the severity of the economic crisis.

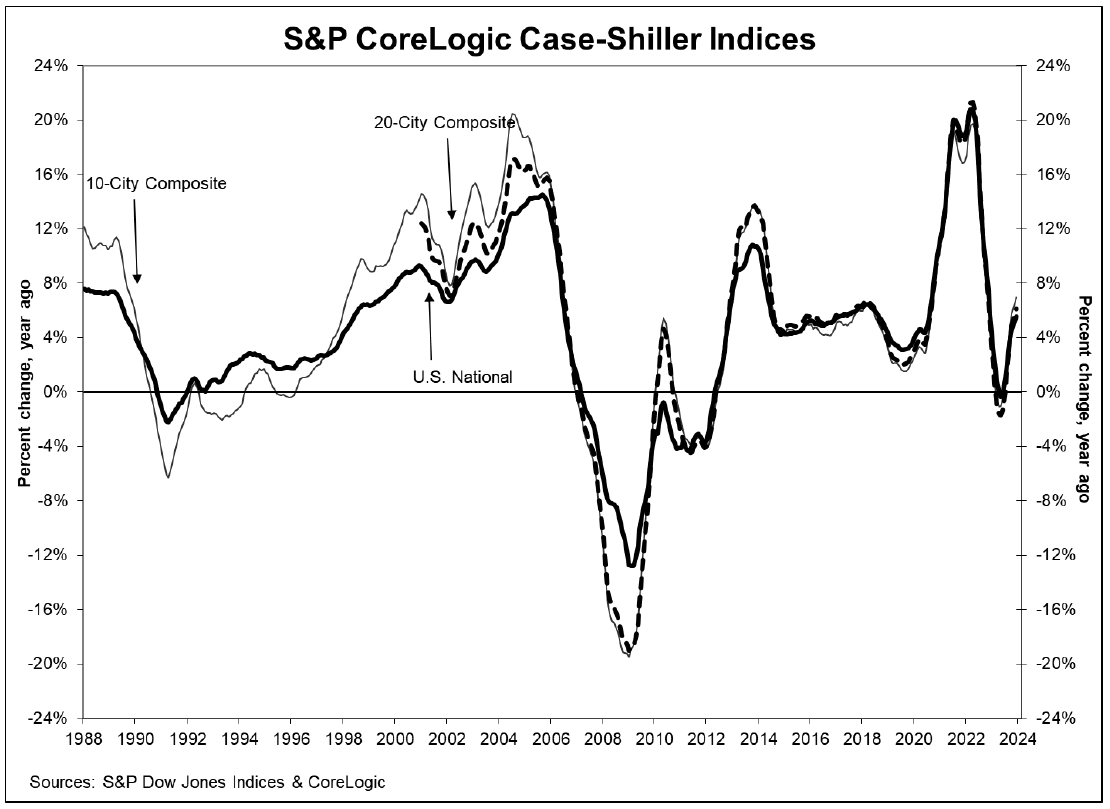

The housing market also suffered greatly. Home prices plummeted, leading to foreclosures and leaving many homeowners owing more on their mortgages than their properties were worth. This period saw a sharp decline in consumer spending, which further exacerbated the economic slump.

Government Response and Recovery

The government responded with various measures to stimulate the economy, including the controversial Troubled Asset Relief Program (TARP) and the American Recovery and Reinvestment Act (ARRA). These programs aimed to stabilize the banking system and provide economic stimulus through various forms of tax cuts, unemployment benefits, and funding for infrastructure projects.

The recession officially ended in June 2009, but the recovery was slow, and the effects were felt for many years after. The economic policies and regulations implemented in response to the recession have been the subject of much debate, with differing opinions on their effectiveness and long-term implications.

Long-Term Effects of Recession

Job Market and Housing

The long-term effects of the Great Recession, which spanned from December 2007 to June 2009, have been profound and enduring, reshaping the economic landscape in the United States and beyond. The recession's aftermath saw a range of social and economic shifts that have had lasting impacts.

One of the most significant long-term effects has been on the job market. The recession led to a sharp increase in unemployment, and while the job market has recovered, the nature of employment has changed. There has been a notable shift towards more part-time and contract work, often without the benefits and job security associated with full-time employment. This has contributed to what some economists call the “gig economy,” where short-term positions are common, and organizations contract with independent workers for short-term engagements.

The housing market, where the crisis originated, also faced long-lasting changes. Homeownership rates declined as many people lost their homes to foreclosure or were unable to afford to buy. This led to a surge in demand for rental properties, driving up rents and changing the dynamics of the housing market. The crisis also resulted in stricter lending standards and regulations, which have made it more challenging for some segments of the population to obtain mortgages.

Consumer Behavior and Government Policy

Another enduring effect of the recession has been on consumer behavior. The economic uncertainty prompted a shift towards saving rather than spending, which has persisted even as the economy has improved. This change in consumer behavior has had a dampening effect on economic growth, as consumer spending is a significant driver of the economy.

The Great Recession also had a lasting impact on government policy and public finances. In response to the crisis, the U.S. government implemented significant stimulus measures, which led to a substantial increase in public debt. This has had long-term implications for fiscal policy, with debates continuing over the best approach to managing the debt while supporting economic growth.

Education and Human Capital

Education and human capital have also been affected. The recession led to cuts in education funding and increased tuition costs, which have made higher education less accessible for some. This has potential long-term implications for the skill level of the workforce and economic productivity.

Lastly, the psychological impact of the recession should not be underestimated. Many individuals who lived through the financial crisis carry the memory of economic hardship, which can influence their financial decisions and risk tolerance for years to come.

Additional Resources

For more detailed information on the history of U.S. recessions and their impact, the Wikipedia page on the List of recessions in the United States offers a comprehensive overview. Additionally, the Federal Reserve Bank of St. Louis provides a GDP-based recession indicator that offers a mechanical assessment of recessions based on historical GDP data. These resources can provide further insights into the economic patterns that characterize recessions in the U.S. and help contextualize the economic challenges faced during these periods.