Have you ever wondered how much houses will cost in 2050? This intriguing question is more than just a casual inquiry for many; it’s a vital consideration for potential homebuyers, investors, and anyone watching the housing market. The average American is faced with skyrocketing home prices and ever-increasing rent rates, making the prospect of future home costs a pressing topic.

As we navigate through a period of economic fluctuations, societal changes, and evolving technology, understanding the trajectory of housing costs is essential. So, let’s dive deep into the historical context and possible predictions to answer the pressing question: how much will houses cost in 2050?

So, How Much Will Houses Cost in 2050?

Key Takeaways

- Current Average Home Value: The typical U.S. home is now worth approximately $362,156.

- Surge in Monthly Payments: The average mortgage payment has skyrocketed, up 111.1% since pre-pandemic levels, reaching around $1,900.

- Future Price Predictions: By 2050, experts anticipate that the average home price could reach between $600,000 and $700,000 in the United States.

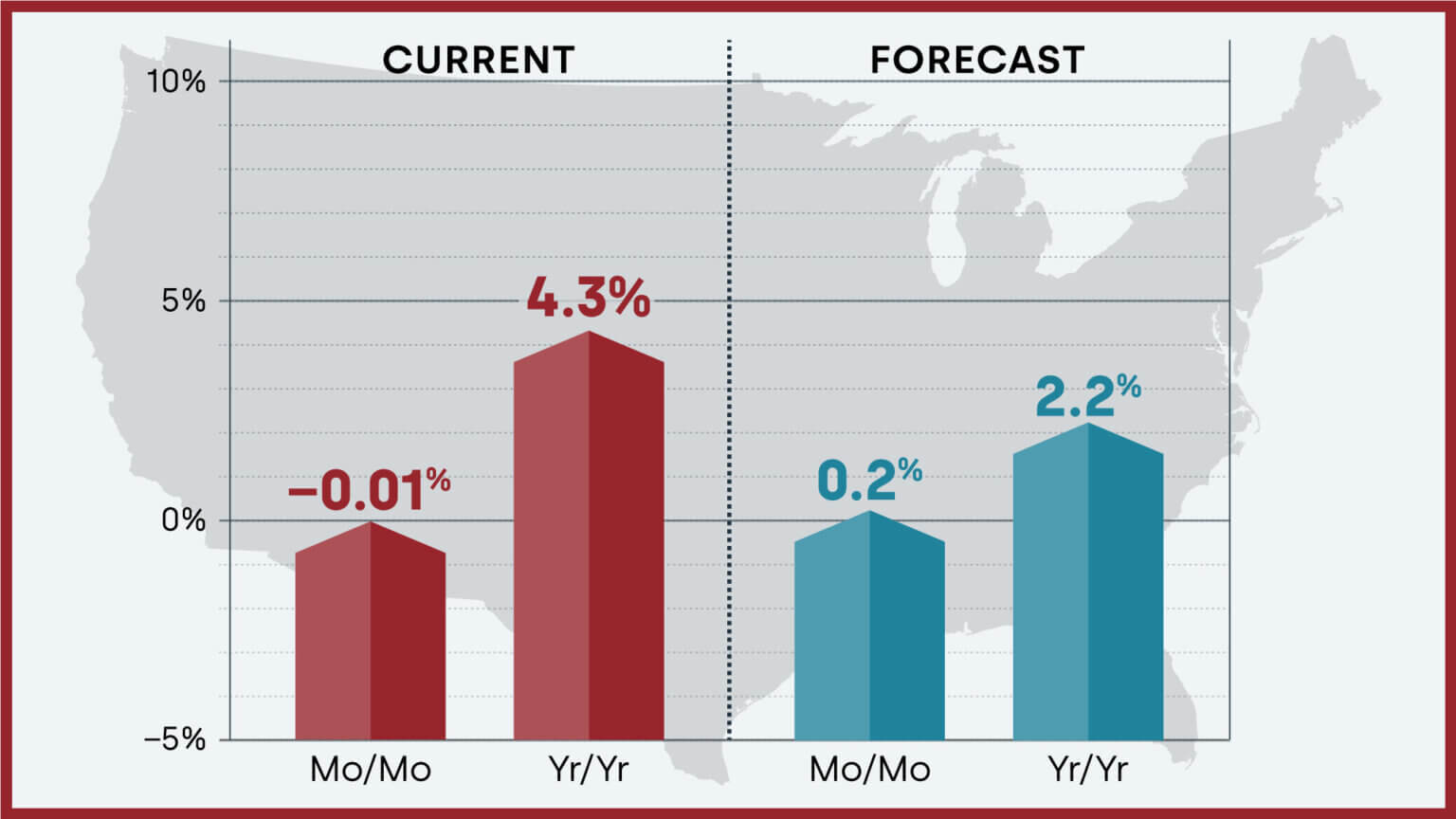

- Market Variability: Home values rose month-over-month in 34 of the 50 largest metro areas, with San Jose experiencing the highest annual price gain of 10.6%.

- Outlook on Future Values: Experts anticipate sustained increases in housing costs, influenced by demand, limited housing supply, and broader economic factors.

- Impact of Societal Changes: Urban living trends, technological advancements, and climate considerations will significantly shape the housing market by 2050.

Recommended Read:

Housing Market Predictions for the Next 4 Years: 2024 to 2028

A Glimpse into Historical Home Prices

To forecast how much houses will cost in 2050, it’s crucial to examine the historical trends of home prices. Over the decades, U.S. home values have seen periods of significant growth, sharp declines, and slow recoveries.

In the late 1990s and early 2000s, home prices surged, driven by low-interest rates, speculative investing, and a booming economy. This era of appreciation was followed by a catastrophic downturn after the 2008 financial crisis, where housing prices plummeted, and many homeowners found themselves underwater on their mortgages. For instance, the national average home price fell from approximately $229,000 in 2007 to about $174,000 in 2012 (source: Zillow).

Historically, the real estate market has shown resilience. After hitting rock bottom, it began to bounce back. By 2012, home prices started climbing again, largely supported by a recovering economy, a resurgence in consumer confidence, and low mortgage rates. As of late 2024, the typical home price is nearing $362,156, highlighting a remarkable recovery and a renewed interest in homeownership.

Current Market Trends: What’s Driving Prices Up?

Understanding the current market is critical in predicting how much houses will cost in 2050. The housing market today reflects a unique combination of factors that continue to push home prices upward. Here are some of the most significant trends at play:

1. Interest Rates: The Double-Edged Sword

Interest rates have long been a pivotal factor in influencing the housing market. The Federal Reserve's increasing rates to combat inflation have made borrowing more expensive. This often puts a strain on potential buyers, as higher mortgage rates lead to higher monthly payments. Currently, the typical monthly payment sits at around $1,900—a hefty sum that can deter many buyers from entering the market. If inflation persists, we may see continued hikes in interest rates, which could have a cooling effect on home prices in the short term.

2. Urban Exodus and Suburban Boom

Since the pandemic, there's been a noticeable shift in where people choose to live. Many individuals and families are leaving crowded urban centers for the suburbs, seeking affordable housing and more space. This trend can potentially drive prices up in suburban areas while urban centers may see a stabilization or decline in home values. According to Zillow, many suburban areas are witnessing a competitive housing market, further stressing the low inventory situation.

3. Limited Housing Supply

The construction industry is facing significant challenges. Supply chain disruptions and labor shortages have led to a slowdown in new home construction. The scarcity of available homes has intensified competition among buyers, leading to bidding wars that push prices even higher. With new home construction struggling to meet demand, this imbalance is expected to continue influencing home prices over the next several years.

Future Predictions: Housing Prices by 2050

So, how much will houses cost in 2050? This question is difficult to answer definitively, but forecasts can offer valuable insights. Based on current trends, economic principles, and historical data, experts predict that home costs could substantially increase by 2050.

Inflation and Economic Growth

Historically, home values have appreciated at a rate of about 3% annually, which often surpasses the general inflation rate. If we apply a similar model moving forward, a home currently priced at $362,156 could be valued between $600,000 and $700,000 by 2050, assuming a consistent appreciation pattern. This projection takes into account expected inflation rates of 2% to 3% and demographic trends that will continue to support demand.

Technological Evolution in Real Estate

The real estate market is evolving at an unprecedented pace due to technological advancements. Virtual reality tours, blockchain transactions, and smart home technologies are becoming increasingly prevalent, making the buying and selling process more efficient. As a result, homes that incorporate modern technology may see an increase in market value as buyers are willing to pay a premium for such conveniences. For prospective homeowners, this means that homes with outdated technology could see diminished value over time, creating a stark contrast between older properties and newer, tech-savvy builds.

Climate Change and Its Effects

As climate change becomes a more pressing issue, how homes are valued may also shift dramatically. Regions that are prone to natural disasters—such as hurricanes, floods, and wildfires—may experience devaluation in the coming decades. In contrast, areas deemed “climate-resilient,” where communities have put measures in place to combat environmental issues, could see stable or increasing home values. It’s crucial to consider that homebuyers will likely weigh environmental factors heavily when making purchasing decisions, potentially leading to substantial differences in real estate prices across the country.

Partner with Norada, Your Trusted Source for Turnkey Investment Properties

Discover high-quality, ready-to-rent properties designed to deliver consistent returns. Contact us today to expand your real estate portfolio with confidence.

Societal Changes Impacting Housing Demand

Understanding the current and future societal landscape is critical in our prediction of home prices.

Demographic Shifts

The millennial generation is now in its prime home-buying years. As they seek to establish families and settle down, demand for housing will likely remain high, especially in urban and suburban areas. This demographic shift means that builders must innovate and create homes that meet the needs and preferences of these younger buyers, which may influence the costs of various housing options.

Remote Work and Lifestyle Changes

The flexibility afforded by remote work has allowed people to live farther from their workplaces. This trend is pushing many buyers to explore areas that offer better quality of life at lower prices. While this can lead to price drops in congested urban areas, it can create ultimates challenges for suburban regions that suddenly experience high demand. Consequently, looking forward to 2050, homes in desirable regions within reasonable commuting distance from major employment hubs are likely to see the greatest appreciation.

Conclusion: Preparing for a Changing Housing Market

As we ponder over how much houses will cost in 2050, it’s clear that a multitude of factors will shape the market over the coming decades. From economic conditions to technological advancements and societal changes, the landscape of homeownership will likely evolve dramatically.

By understanding these trends and considering the data, calling for careful thought and reflection, it becomes evident that predicting the future of home costs isn’t just speculation; it’s about recognizing the patterns from our past and present to better foresee what lies ahead.

Also Read:

- Housing Market Predictions for the Next 4 Years: 2024 to 2028

- Real Estate Forecast Next 5 Years: Top 5 Predictions for Future

- Is the Housing Market on the Brink in 2024: Crash or Boom?

- 2008 Forecaster Warns: Housing Market 2024 Needs This to Survive

- Housing Market Predictions for the Next 2 Years

- Real Estate Forecast Next 10 Years: Will Prices Skyrocket?

- Housing Market Predictions for Next 5 Years (2024-2028)

- Housing Market Predictions 2024: Will Real Estate Crash?

- Housing Market Predictions: 8 of Next 10 Years Poised for Gains

- Trump vs Harris: Which Candidate Holds the Key to the Housing Market (Prediction)