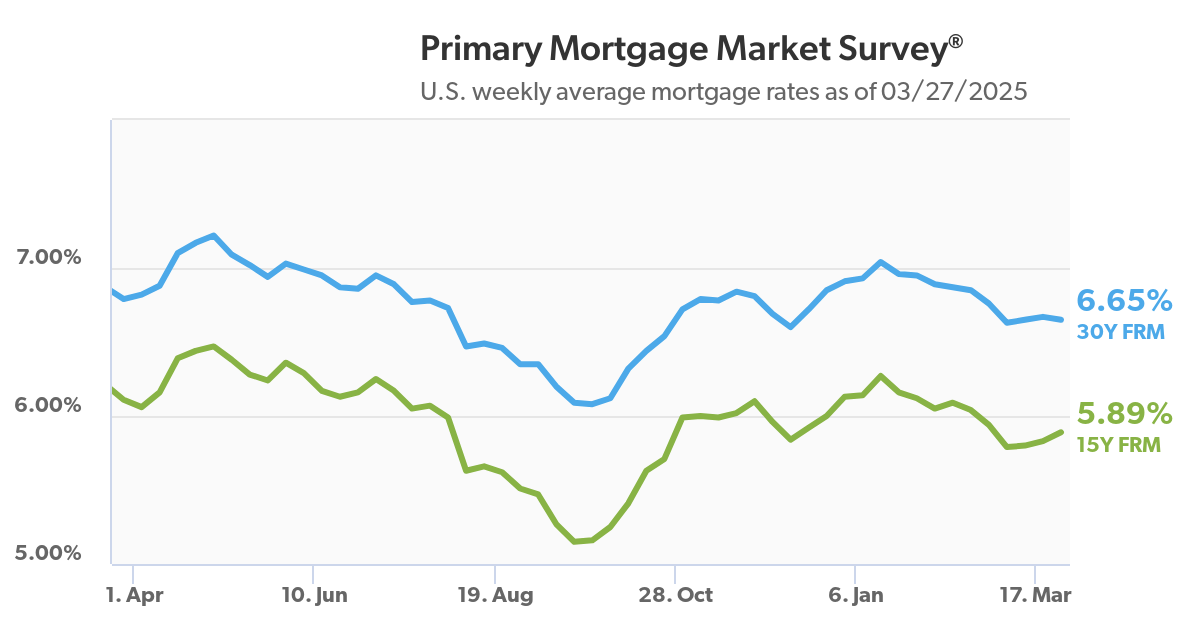

If you're like me, keeping an eye on mortgage rates feels like watching the weather – constantly changing and impacting big decisions. So, let's get straight to it. Based on current expert analysis, it looks like mortgage rates are likely to remain in the mid-6% range for much of 2025, hovering around 6.4% to 6.6%. This isn't just a hunch; it's what the folks at the National Association of REALTORS® (NAR), Fannie Mae, and Freddie Mac are predicting.

Now, I know what you might be thinking: “Didn't we hear about potential rate cuts?” And you're right. But the story with mortgage rates is a bit more complex than just following the Federal Reserve's moves. I've spent years watching these trends, and what I've learned is that several factors play a crucial role in where those interest rates on your potential home loan land.

Expert Predictions Show Mid-6% Mortgage Rates Likely to Stay in 2025

Mortgage rates aren't set in stone by a single entity. Instead, they're influenced by a whole mix of economic factors. Think of it like a tug-of-war, with different forces pulling in different directions. Here are some of the main players:

- The Federal Reserve (The Fed): The Fed sets the federal funds rate, which is the rate banks charge each other for short-term loans. While this doesn't directly dictate mortgage rates, it has a ripple effect on borrowing costs throughout the economy. As of late March 2025, the Fed has kept this rate steady at around 4.5%, with talk of maybe two rate cuts later in the year.

- Inflation: This is a big one. When the cost of goods and services goes up (that's inflation), lenders want a higher return on their loans to make up for the fact that the money they get back in the future will be worth less. Right now, even with potential Fed moves, there are still concerns about inflation, partly due to ongoing trade policies.

- Economic Growth: A strong economy usually means more demand for borrowing, which can push interest rates up. Forecasts show continued job growth in 2025, which is good for the economy overall but can contribute to those higher mortgage rates.

- The Bond Market (Specifically the 10-Year Treasury Yield): This is a key benchmark. Mortgage rates tend to closely follow the yield on the 10-year Treasury bond. Think of this bond yield as representing what investors are willing to accept for lending their money over a 10-year period. Currently, this yield is floating around 4.3% to 4.5%. Since mortgage loans are long-term investments, their rates typically have a spread (a bit extra) on top of this Treasury yield.

Why the Mid-6% Range Feels Likely for 2025: My Take

Looking at all these pieces, it makes sense to me why the experts are predicting mortgage rates will stick in that mid-6% area for a good chunk of 2025. Even if the Fed does cut rates a couple of times, those cuts might not translate directly into big drops in mortgage rates. Here’s my thinking:

- Persistent Inflation: From what I'm seeing, even with potential Fed action, there's still an underlying worry about inflation not cooling down as quickly as some might hope. Global events and trade dynamics can keep those price pressures alive, which in turn keeps bond yields higher.

- The Bond Market's Reaction: Investors in the bond market are the ones who ultimately set the 10-year Treasury yield. They look at the overall economic picture, including inflation expectations and the government's fiscal health. If they're not convinced that inflation is truly under control, they'll likely demand a higher yield, which then puts a floor under mortgage rates.

- A Resilient Economy: While some sectors might be feeling the pinch, the overall job market is projected to remain relatively strong. That's a good thing for people's financial security, but it also means there's still decent demand for borrowing, preventing rates from falling sharply.

What This Means for the Housing Market: More Activity Ahead?

Now, here's an interesting twist. Even with these relatively higher mortgage rates, the forecasts suggest we might actually see an uptick in home sales in 2025. NAR is predicting a 6% increase in existing home sales and a 10% jump in new home sales. This might sound counterintuitive, but here's why I think it could happen:

- The “Rate Lock-In” Effect Cooling Down: For the past couple of years, many homeowners who locked in super-low mortgage rates during the pandemic have been hesitant to sell. Why would they give up a 3% interest rate to buy a new home at 6% or higher? However, life happens. People need to move for jobs, family reasons, or simply because their current home no longer fits their needs. As time goes on and people build more equity in their homes, the sting of those higher new rates might become a little less painful, leading to more inventory coming onto the market.

- Buyers Adjusting to the New Normal: Let's be honest, the ultra-low mortgage rates we saw a few years ago were somewhat of an anomaly. Historically, rates in the mid-6% range aren't wildly out of the ordinary. Potential homebuyers who have been on the sidelines might start to realize that waiting for rates to plummet might not be the best strategy, and they might decide to move forward with their plans.

- Continued Job Growth: With projections of 1.6 million new jobs in 2025, more people will have the financial stability to consider buying a home. A steady job provides the confidence needed to take on a mortgage.

And what about prices? NAR is forecasting a 3% rise in the median home price for 2025. This suggests that while affordability might still be a concern for some, the demand in the market is expected to remain firm enough to push prices up moderately.

Recommended Read:

2025 Mortgage Rate Volatility Sparks Home Buyer Anxiety

How Much Lower Can Mortgage Rates Drop in 2025?

Mortgage Rates Drop: Can You Finally Afford a $400,000 Home?

Expect High Mortgage Rates Until 2026: Fannie Mae's 2-Year Forecast

A Look Back: Putting Things in Perspective

It's always helpful to remember where we've come from. Mortgage rates have seen some significant swings throughout history. We touched a high of over 18% in the early 1980s and a low of around 2.65% just a few years ago. So, while the mid-6% range might feel high compared to those recent lows, it's important to remember that it's still below the historical average. This broader perspective can sometimes make the current situation feel a bit less daunting.

My Final Thoughts: Staying Informed is Key

Based on what I'm seeing and the analysis from these leading organizations, it does seem quite likely that mortgage rates will remain in that mid-6% territory for a significant portion of 2025. Of course, the economy is a dynamic beast, and unexpected events can always throw a wrench in the works. That's why it's so crucial to stay informed, keep an eye on the economic news, and talk to real estate and mortgage professionals who can provide personalized advice based on your individual situation.

For potential homebuyers, this likely means factoring these rates into your budget and understanding what you can comfortably afford. For sellers, it suggests that while demand might be picking up, realistic pricing will still be important.

Ultimately, navigating the housing market requires understanding these underlying trends. While we can't predict the future with absolute certainty, looking at the data and expert opinions gives us a pretty good idea of what to expect in the year ahead.

Work With Norada, Your Trusted Source for

Real Estate Investments

With mortgage rates fluctuating, investing in turnkey real estate

can help you secure consistent returns.

Expand your portfolio confidently, even in a shifting interest rate environment.

Speak with our expert investment counselors (No Obligation):

(800) 611-3060

Also Read:

- Are Ultra-Low 2% and 3% Mortgage Rates Ever Coming Back?

- Will Mortgage Rates Go Down in 2025: Morgan Stanley's Forecast

- Mortgage Rate Predictions 2025 from 4 Leading Housing Experts

- Mortgage Rates Forecast for the Next 3 Years: 2025 to 2027

- 30-Year Mortgage Rate Forecast for the Next 5 Years

- 15-Year Mortgage Rate Forecast for the Next 5 Years

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?

- Mortgage Interest Rates Forecast for Next 10 Years