Today, July 28, 2026, I've got some interesting news for homeowners looking to refinance. The average rate on a 30-year fixed refinance has dipped slightly, now sitting at 6.99%. This is a small but welcome drop of 6 basis points from yesterday. While it might seem like a tiny change, for those with big mortgages, even small shifts can mean saving a good chunk of money over time.

We saw them dip down to near 6.0% at the beginning of 2026, which felt like a real gift. But then, as the summer heated up, so did the rates, climbing back up and hovering just shy of 7% for a while. Now, this small decrease is a breath of fresh air.

Mortgage Rates Today, July 28, 2026: 30-Year Refinance Rate Drops by 6 Basis Points

What Does This Drop Mean for You?

A 6-basis point drop might not sound like a lot, but let me tell you, it can add up. Imagine you have a $300,000 mortgage. That 0.06% difference translates to about $180 less in interest over a year. Over the life of a 30-year loan, that's over $5,000! So, while you shouldn't rush into refinancing based on a single day's rate, it's definitely a good time to check if refinancing makes sense for your financial picture.

Current Refinance Rates (as of July 28, 2026)

Here’s a quick look at the national averages announced by Zillow today:

| Loan Term | Average Rate | Change from Previous Day | Change from Previous Week |

|---|---|---|---|

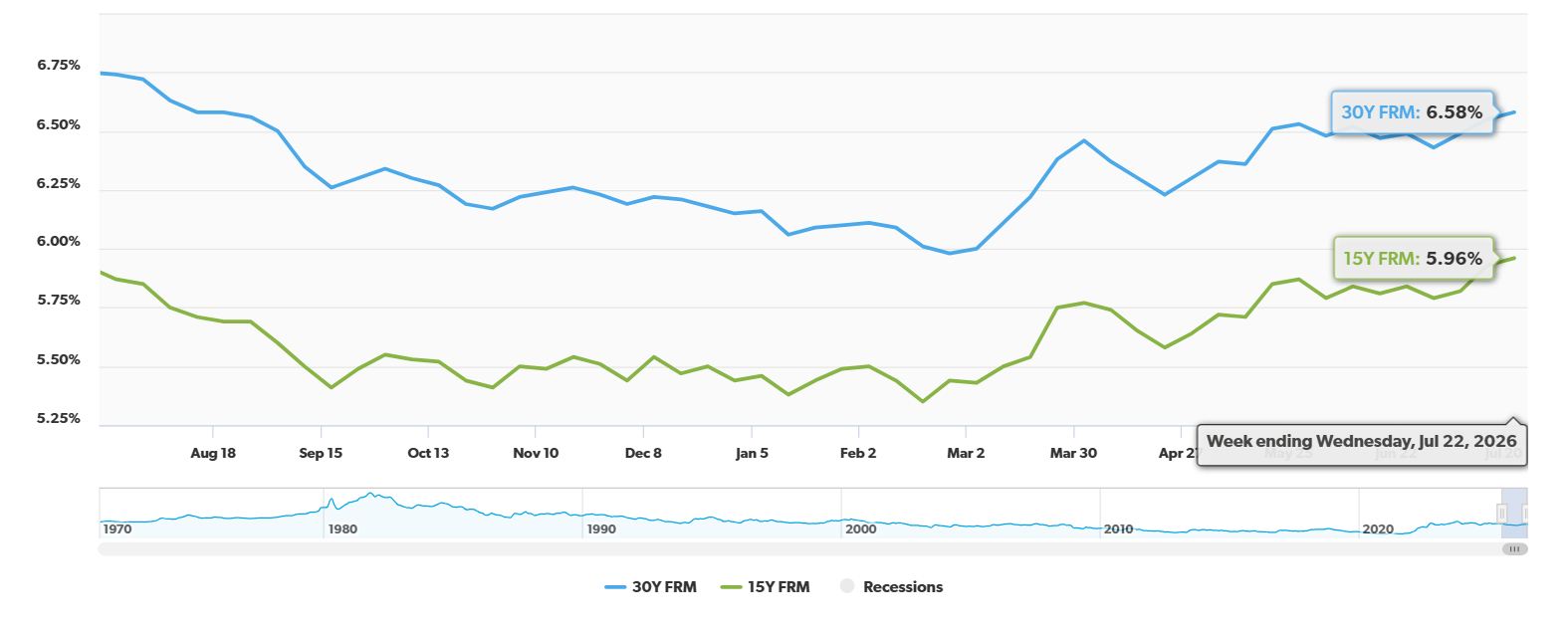

| 30-Year Fixed Refinance | 6.99% | Down 6 basis points | Down 5 basis points |

| 15-Year Fixed Refinance | 5.99% | Down 7 basis points | N/A |

| 5-Year ARM Refinance | 6.00% | N/A | N/A |

As you can see, the 15-year fixed refinance rate also saw a nice dip, dropping by 7 basis points to 5.99%. For those who can handle a higher monthly payment, switching to a 15-year loan can save you a huge amount of money on interest over the life of the loan.

Why Are Rates Doing This Dance?

Understanding why rates move is key to making smart financial decisions. Right now, a few big things are influencing mortgage rates:

- Global Unrest: Sadly, new tensions in the Middle East, particularly involving Iran, have caused a bit of a stir in the financial markets. When there's uncertainty in the world, investors often move their money to safer places, which can affect bond yields and, consequently, mortgage rates.

- Oil Prices and Inflation Worries: This global instability has also pushed oil prices above $100 a barrel. Higher energy costs can make prices for everything else go up, leading to fears of inflation. Lenders get nervous when inflation is high, and they tend to increase interest rates.

- A Strong U.S. Economy: On the flip side, our economy here in the U.S. is still chugging along. We're seeing good job numbers and people are still spending money. This strength, while good for the economy, can also keep inflation from cooling down too quickly.

- The Federal Reserve's Stance: Because inflation is still a concern, the Federal Reserve decided to keep its main interest rate steady at its July meeting. In fact, some Fed officials have even mentioned the possibility of raising rates later this year if inflation doesn't calm down. This keeps lenders cautious.

Should You Refinance Now? My Two Cents.

This is where my own experience comes in. I've seen people get so caught up in chasing the absolute lowest rate that they end up making a mistake. Refinancing isn't just about the rate you see advertised; it’s about your personal situation.

Here are the things I always tell people to consider:

- The Break-Even Point: Refinancing usually comes with costs, often 2% to 6% of your loan amount. You need to figure out how long it will take for the money you save on your monthly payments to cover these costs. If you plan to move or refinance again before you hit that break-even point, it might not be worth it.

- Shop Around, Seriously! I can't stress this enough. The difference in rates between lenders can be substantial. Don't just go with the first one you find. Get quotes from at least three different lenders – banks, online lenders, and even your local credit union. Data shows that borrowers who don't shop around can end up paying tens of thousands of dollars more over the life of their loan.

- Shorter Loan Terms: If you're considering moving from a 30-year to a 15-year loan, be prepared for a higher monthly payment. However, the interest savings are often incredible. You could pay off your home years earlier and save a fortune in interest.

- Home Equity Alternatives: If your goal is to pull cash out of your home for renovations or other big expenses, think carefully. A cash-out refinance means you're refinancing your entire first mortgage at today's rates. Sometimes, it’s smarter to get a Home Equity Line of Credit (HELOC) or a separate home equity loan. These options might let you keep your existing, lower first mortgage rate.

The Crystal Ball: What's Next?

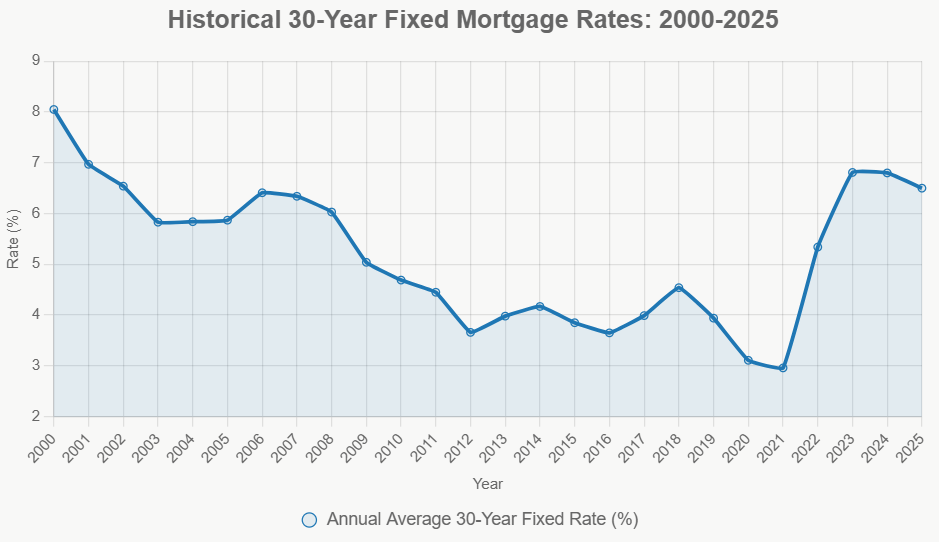

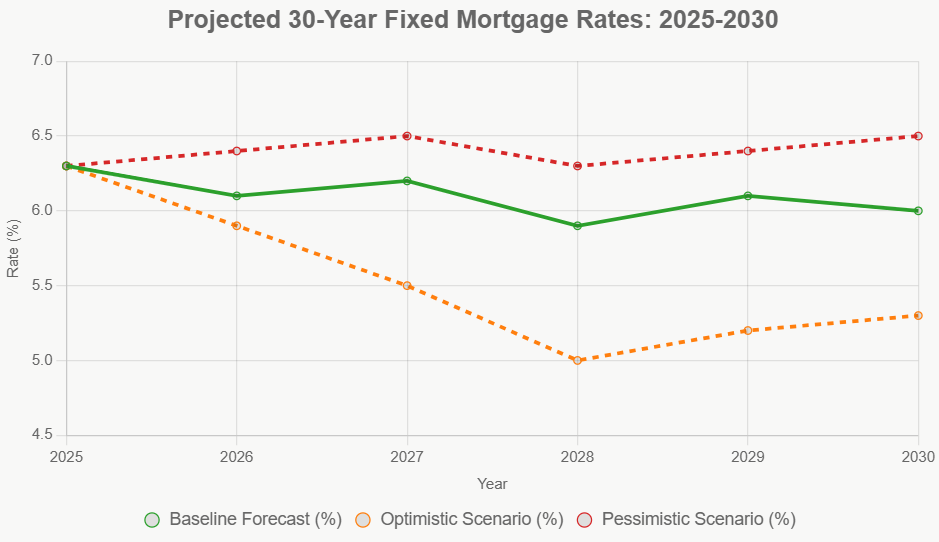

Looking ahead, the experts at Fannie Mae and the Mortgage Bankers Association are predicting that rates will likely stay in the 6.3% to 6.5% range for the rest of 2026 and into 2027. This means that while today's slight drop is nice, we're probably not going back to those super-low pandemic rates anytime soon.

Even with rates higher than they were a couple of years ago, about one-third of homeowners are still looking to refinance. Most of these are people who took out loans at 7% or higher recently and can still benefit from even a small rate decrease.

The Takeaway

Today's slight dip in mortgage rates is a positive sign, especially for the 30-year fixed refinance. It’s a good reminder to stay informed and evaluate your own financial situation. Whether or not refinancing is the right move for you depends on your specific loan, your financial goals, and how long you plan to stay in your home. Always do your homework, compare lenders, and understand all the costs involved.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?