It's a good day for homeowners looking to refinance! Today, July 20, 2026, the national average for a 30-year fixed refinance rate has dipped to 6.77%, a welcome drop of 17 basis points from yesterday's 6.94%. This news, reported by Zillow, brings a little relief to many who have been watching rates closely.

While we're not quite at those super-low pandemic days, this move in the right direction is definitely worth paying attention to. For many of you who refinanced or bought a home when rates were higher, this could be the sign you've been waiting for to potentially lower your monthly payments.

Mortgage Rates Today, July 20, 2026: 30-Year Refinance Rate Drops by 17 Basis Points

What's Making Rates Dip Today?

So, why the sudden dip? While it might feel like a surprise, it's actually part of a larger, albeit bumpy, journey rates have been on this year. We've seen rates go up and down, kind of like a roller coaster, but this drop is significant.

Over the past few months, rates have mostly been playing a game of “staying put” or inching up a tiny bit. They’ve been well above the incredibly low rates we saw during the pandemic, but thankfully, they’re also a bit better than the nearly 8% highs we hit at the end of 2023.

Looking back, the first half of 2026 saw some interesting shifts. We had a little dip in early 2026, where rates touched a low of 6.09%. That was a happy time for homeowners who bought when rates were high, as they had a chance to refinance and save. But then, as the economy showed stronger signs of recovery, rates climbed back up into the mid-to-high 6% range by the middle of the year.

Now, this little drop today is a breath of fresh air. It’s important to remember that these changes often come from bigger economic factors. The Federal Reserve’s stance on keeping interest rates steady for a while longer, to fight stubborn inflation, plays a big role. When the Fed keeps rates higher, it makes borrowing money more expensive, which affects things like long-term bonds, and in turn, mortgage rates.

Also, global energy prices have been a bit unpredictable. When fuel costs go up, it can keep inflation higher than the Fed wants, and this also pushes bond yields up, influencing mortgage rates.

My take on this? It's a good reminder that mortgage rates are super connected to what’s happening in the wider economy. The 10-year Treasury yield, which is basically how much interest the government pays on its bonds, is a key indicator. When those yields go up or down because of economic news, mortgage rates tend to follow right along.

Current Refinance Rates You Should Know

Here's a snapshot of what the refinance rates look like today, Monday, July 20, 2026, according to Zillow:

| Loan Type | Average Rate |

|---|---|

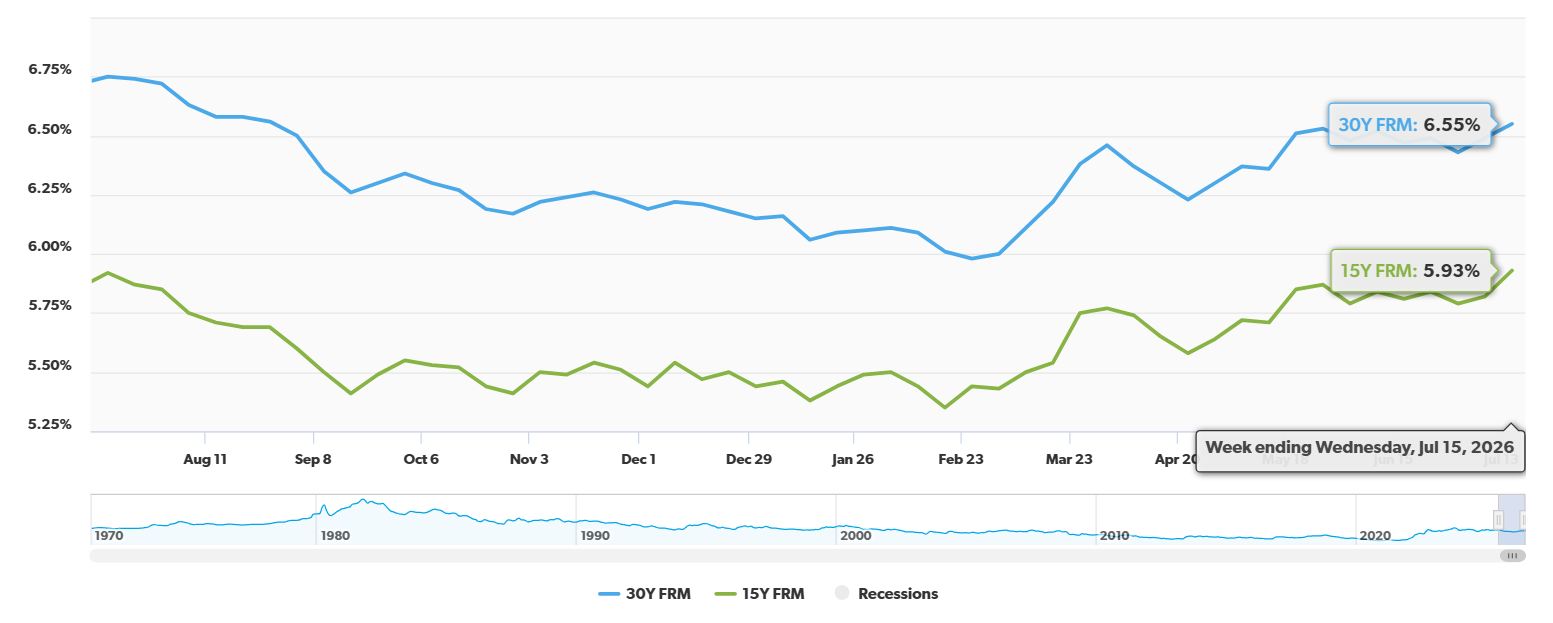

| 30-Year Fixed Refinance | 6.77% |

| 15-Year Fixed Refinance | 5.80% |

| 5-Year ARM Refinance | 6.12% |

It's interesting to see the difference between the 30-year and 15-year fixed rates. The 15-year is still quite a bit lower, which is typical, but the drop in the 30-year is the big story today. The 5-year ARM rate holding steady at 6.12% is also something to note if you're considering that option.

Is Refinancing Right for You Today?

This drop in rates makes it a great time to revisit your mortgage. But, as always, refinancing isn't a magic bullet for everyone. Here are some things I always tell people to think about before jumping in:

- How much will you really save? The most important thing is to look at the interest rate differential. If you locked in a rate that was, say, 7.5% or even 7%, then dropping to 6.77% could save you a good chunk of money each month. However, if your current rate is already lower, or close to it, the savings might not be worth the effort and cost.

- What are your closing costs? Refinancing isn't free. You'll likely have to pay closing costs, which can range from 2% to 5% of your loan amount. You need to figure out your break-even point. This is the number of months it will take for your lower monthly payments to add up to the amount you spent on closing costs. If you plan to move before you reach that point, it might not be a good deal.

- Beware of “No-Cost” Refis: These sound great, but they usually come with a catch. Often, the closing costs are rolled into your loan balance, meaning you'll pay interest on them, or the interest rate itself will be higher than on a refinance where you pay closing costs upfront. I always advise people to read the fine print very carefully on these.

- Your Credit Score and Home Equity Matter: Lenders look at these things very closely. If you have a credit score of 740 or higher and at least 20% equity in your home, you're more likely to get the best rates. If your credit score has dipped or your home value has decreased, you might not qualify for the lowest rates.

- Debt-to-Income Ratio (DTI): Lenders want to see that you can comfortably handle your mortgage payments. Your DTI is your total monthly debt payments divided by your gross monthly income. Most lenders want this to be below 43%. If it's higher, it might be harder to get approved.

Where Are Rates Heading Next?

Looking ahead, experts are predicting that rates will probably stay in the 6.3% to 6.5% range for the rest of 2026. They don't expect rates to drop significantly until late 2027. So, while this drop today is welcome, it might be a good idea to grab it if it makes sense for your finances.

This current rate environment, with its ups and downs, highlights the importance of staying informed. It's not just about the headlines; it's about understanding how these changes affect your personal financial situation.

Key Takeaways for Refinancers

- Today's 30-year fixed refinance rate is 6.77% (down 17 basis points).

- This is a positive sign after a period of relatively stable or rising rates.

- Consider your current rate, closing costs, and break-even point.

- Strong credit scores and home equity improve your chances of getting the best rates.

- Future rate predictions suggest a period of relative stability in the mid-6% range.

It’s a smart move to talk to a mortgage professional, run the numbers, and see if this current dip in rates is your opportunity to save money.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?