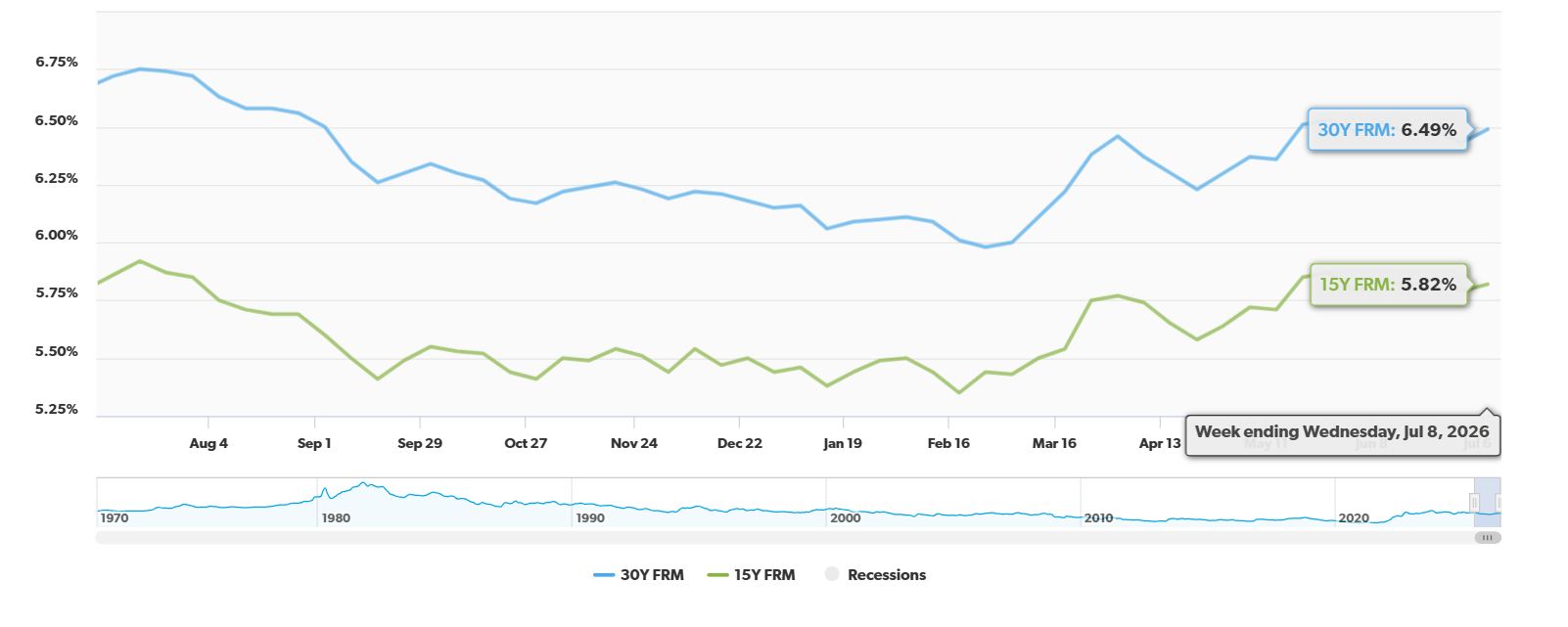

The mortgage world is always buzzing with news, and today, July 16, 2026, brings a welcome shift for those looking to refinance. The average 30-year fixed refinance rate has dipped by a notable 19 basis points, now sitting at 6.81%, according to Zillow. While this is good news, it's important to remember where we've been and where we might be heading.

Mortgage Rates Today, July 16, 2026: 30-Year Refinance Rate Drops by 19 Basis Points

A Little Relief in the Refinance Market

For homeowners hoping to snag a better deal on their mortgage, this drop is a breath of fresh air. We saw the 30-year fixed refinance rate fall from 7.00% to 6.81%. It's a small step, but in the world of mortgages, even a few basis points can make a difference over the life of a loan. It's worth noting that this rate is just a tiny bit higher, up by 1 basis point, from last week's average of 6.80%.

But it's not all good news across the board. The 15-year fixed refinance rate saw a slight tick up, now at 6.00%, a 1-basis point increase from last week. And for those considering an adjustable-rate mortgage (ARM), the 5-year ARM refinance rate is holding steady at 6.12%.

Here's a quick look at how things stack up today, according to Zillow:

| Loan Type | Current Average Rate (July 16, 2026) | Change from Previous Week |

|---|---|---|

| 30-Year Fixed Refinance | 6.81% | -0.19% |

| 15-Year Fixed Refinance | 6.00% | +0.01% |

| 5-Year ARM Refinance | 6.12% | 0.00% |

Why Are Rates Doing This Dance?

It might feel like mortgage rates are on a rollercoaster, and honestly, they kind of are right now. Several big factors are playing a role in keeping these rates higher than many of us would like.

First, there's the geopolitical tension. Conflicts involving the U.S. and places like Iran have sent global oil prices soaring. When gas prices go up, everything tends to get more expensive.

This leads directly to the next point: inflation pressures. All that high energy cost is making consumer prices jump, and inflation is moving further away from the Federal Reserve's goal of keeping it around 2%.

The Federal Reserve is watching this closely. They recently decided to keep their main interest rate steady, between 3.50% and 3.75%. But they've also hinted that they might have to raise rates later this year if inflation doesn't start to calm down. This possibility always casts a shadow over mortgage rates.

And then there's the bond market. When things get uncertain, like when a ceasefire breaks down, investors get nervous. This nervousness drives up the yield on the 10-year Treasury note, which has a direct impact on mortgage rates, pushing them higher. It’s a complex web, and it’s why we see these fluctuations.

Thinking About Your Refinance Strategy

Now, let's talk about what this means for you. Many of us locked in incredibly low rates during the pandemic, somewhere between 2% and 4%. If you're one of the many who have a rate in that sweet spot, a simple rate-and-term refinance probably doesn't make much sense right now. You'd likely be trading a great rate for a slightly less great one, and that often doesn't save you money in the long run.

However, there are still smart reasons to consider refinancing.

- FHA/VA Streamlines: If you bought a home recently when rates were really high, maybe close to 7% or even more, you might want to look into FHA Streamline or VA IRRRL options. These are special programs that allow for a quick, easy refinance with less paperwork and often without needing a new appraisal. They can be a good way to lower your rate without a lot of hassle.

- Cash-Out Refi Wisely: Home values are still pretty high, which means many homeowners have built up a good amount of equity in their homes. If you need cash for something important, like a big home renovation or to pay off high-interest credit card debt, a cash-out refinance could be a good move. You could also consider a Home Equity Line of Credit (HELOC), which is currently around 7.04%. It's all about weighing the costs and benefits.

- Shorten Your Loan Term: If your financial situation has improved and you're feeling more secure, you might consider switching from a 30-year mortgage to a 15-year fixed refinance. This can often get you a rate below 6% and will save you a massive amount of money on interest over the life of the loan. Yes, your monthly payments will go up, but you'll pay off your home faster and pay less overall.

- Shop Around, Seriously! This is probably the most important piece of advice I can give. Rates can vary a lot from one lender to another. Don't just go with the first bank you talk to. Get quotes from at least three different lenders. You could save thousands of dollars over time just by doing a little comparison shopping. I’ve seen clients save an incredible amount just by taking the time to get multiple offers.

Refinancing isn't always about chasing the absolute lowest rate. It's about making the right financial move for your specific situation. Today's drop in the 30-year rate is a positive sign, but it's just one piece of the puzzle. Keep an eye on those economic indicators, understand your own financial goals, and always, always shop around.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?