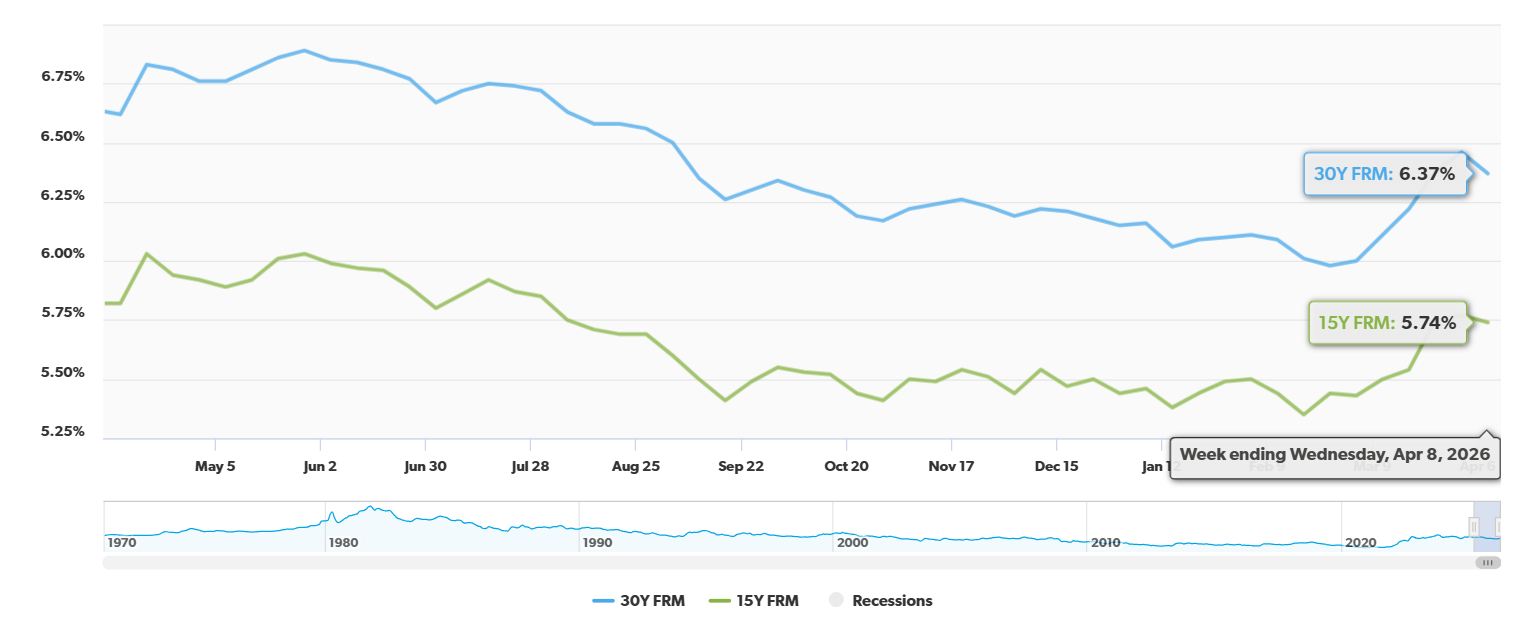

You've probably heard the whispers, and now it's official: the 30-year fixed-rate mortgage rate has dropped steeply, hitting an average of 6.37% for the week ending April 9, 2026. This significant tumble, a decrease of 9 basis points from the previous week, marks a welcome relief after a steady climb and offers a glimmer of hope for homebuyers and homeowners looking to refinance.

30-Year Fixed Mortgage Rate Drops Steeply – Here’s What It Means for You

Why the Sudden Plunge? The Driving Forces Behind the Drop

You might be wondering what’s behind this swift decline. Analysts, including those at the reputable Freddie Mac, are pointing to a rather significant geopolitical event: a tentative ceasefire between the U.S. and Iran. This development has had a ripple effect, most notably leading to a drop in oil prices. When oil prices fall, it often translates to lower inflation fears, which in turn tends to stabilize bond markets. For us, as potential borrowers, this means lenders can offer lower interest rates on mortgages.

Think of it like this: when there's less uncertainty in the world, investors feel more confident putting their money into bonds. Lower yields on bonds make mortgage-backed securities more attractive, and as demand for those rises, the rates they offer – which directly influence mortgage rates – tend to fall. It's a complex dance, but the end result for us is good news.

Sam Khater, Freddie Mac's Chief Economist, put it well, suggesting this could “spark a more favorable spring homebuying season.” I wholeheartedly agree. This kind of rate movement can be the nudge many buyers need to finally make their move, especially as we head into the traditionally busier spring market.

Digging into the Numbers: What the Data Tells Us

Let’s break down these figures from Freddie Mac’s Primary Mortgage Market Survey®, because the details are important:

Weekly Changes:

- 30-Year Fixed-Rate Mortgage: Dropped from 6.46% to 6.37% (a decrease of 0.09%). This ended a streak of five consecutive weeks where rates had been inching upwards. Imagine planning your budget based on one rate, only to see it increase week after week. This halt and reversal is a welcome change.

- 15-Year Fixed-Rate Mortgage: Also eased slightly, from 5.77% to 5.74% (down 0.03%). While not as dramatic as the 30-year, any decrease is a positive sign.

Year-Over-Year Comparison:

This is where the real savings start to become apparent.

- 30-Year Fixed-Rate Mortgage: Currently at 6.37%, it’s down a substantial 0.25% compared to this time last year (when it was 6.62%). That quarter-percent difference might not sound huge, but over the lifetime of a mortgage, it adds up to significant savings.

- 15-Year Fixed-Rate Mortgage: Is down 0.08% year-over-year, moving from 5.82% to 5.74%.

Potential Savings for Homebuyers and Refinancers

To really grasp the impact, let's look at how these rate drops can translate into tangible savings. For the sake of illustration, let's consider a hypothetical home purchase of $400,000.

| Mortgage Term | Rate Last Week | Rate This Week (04/09/2026) | Weekly Savings (P&I) | Rate Last Year (04/09/2025) | Year-Over-Year Savings (P&I) |

|---|---|---|---|---|---|

| 30-Year Fixed | 6.46% | 6.37% | ~$38 | 6.62% | ~$133 |

| 15-Year Fixed | 5.77% | 5.74% | ~$9 | 5.82% | ~$24 |

Note: These are approximate figures for Principal and Interest payments only and do not include taxes, insurance, or other fees.

As you can see, the weekly savings are modest but a pleasant surprise. The year-over-year savings, however, are where the power of this recent decline truly shines. For a 30-year fixed mortgage, that 0.25% drop means paying about $133 less per month on a $400,000 loan. Over 30 years, that’s nearly $48,000 back in your pocket!

For those looking to refinance, this could be an excellent opportunity to lower your monthly payments, pay down your loan faster, or even tap into your home's equity for other needs.

Beyond the Headlines: What This Means for the Spring Housing Market

I've seen markets ebb and flow for a long time, and what’s happening now is particularly interesting. The fact that this rate drop is happening right before the traditional spring selling season is crucial.

Typically, this is when demand for homes surges. If mortgage rates were continuing to climb, that surge would be met with affordability challenges for many buyers. But with rates falling, we could see increased buyer activity. This is a welcome sign for sellers too, potentially leading to quicker sales and perhaps even multiple offers in competitive areas.

It’s also worth noting that the average rate this week (6.37%) is very close to the monthly average of 6.36% and within the 52-week range (5.98% to 6.89%). This suggests that while this week's rate is good, it’s not an unprecedented low compared to the past year. However, the trend is what’s most important here – moving in the right direction.

From my perspective, this rate drop provides much-needed breathing room. It can help buyers who were priced out to re-enter the market and encourage those on the fence to move forward. The stability in bond markets, driven by the easing of geopolitical tensions, is a powerful catalyst.

What to Do Now: Taking Advantage of Lower Rates

If you're thinking about buying a home or refinancing your current mortgage, now is the time to act.

- Get Pre-Approved: If you're a buyer, securing a pre-approval will give you a clear understanding of your budget and show sellers you're a serious contender.

- Shop Around: Don't settle for the first rate you’re offered. Different lenders will have different rates and fees. Compare offers from multiple banks and mortgage brokers.

- Consider Your Long-Term Goals: Are you planning to stay in your home for a long time? If so, a 30-year fixed might still be the best option for predictable payments. If you plan to move in 5-7 years, or if you can comfortably afford higher monthly payments, a shorter term like the 15-year might save you more in interest overall.

- Talk to a Mortgage Professional: A good loan officer can help you understand your options, navigate the process, and find the best mortgage product for your unique situation.

This recent dip in 30-year fixed mortgage rates is a significant development. It’s a clear sign that the market is reacting to global events, and the outlook for the spring homebuying season looks considerably brighter. Whether you're a first-time buyer dreaming of homeownership or a seasoned homeowner looking to improve your financial standing, this is definitely a trend worth paying attention to.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?