If you're thinking about buying a home or refinancing your current one, you'll be happy to hear that today, July 7, mortgage rates are showing a slight dip, making things a little more affordable. The average 30-year fixed mortgage rate is currently sitting at 6.36%, a small drop from yesterday. This little bit of good news comes as a welcome change for many looking to make their housing dreams a reality.

Today's Mortgage Rates, July 7: Rates Drop Slightly as Market Reacts

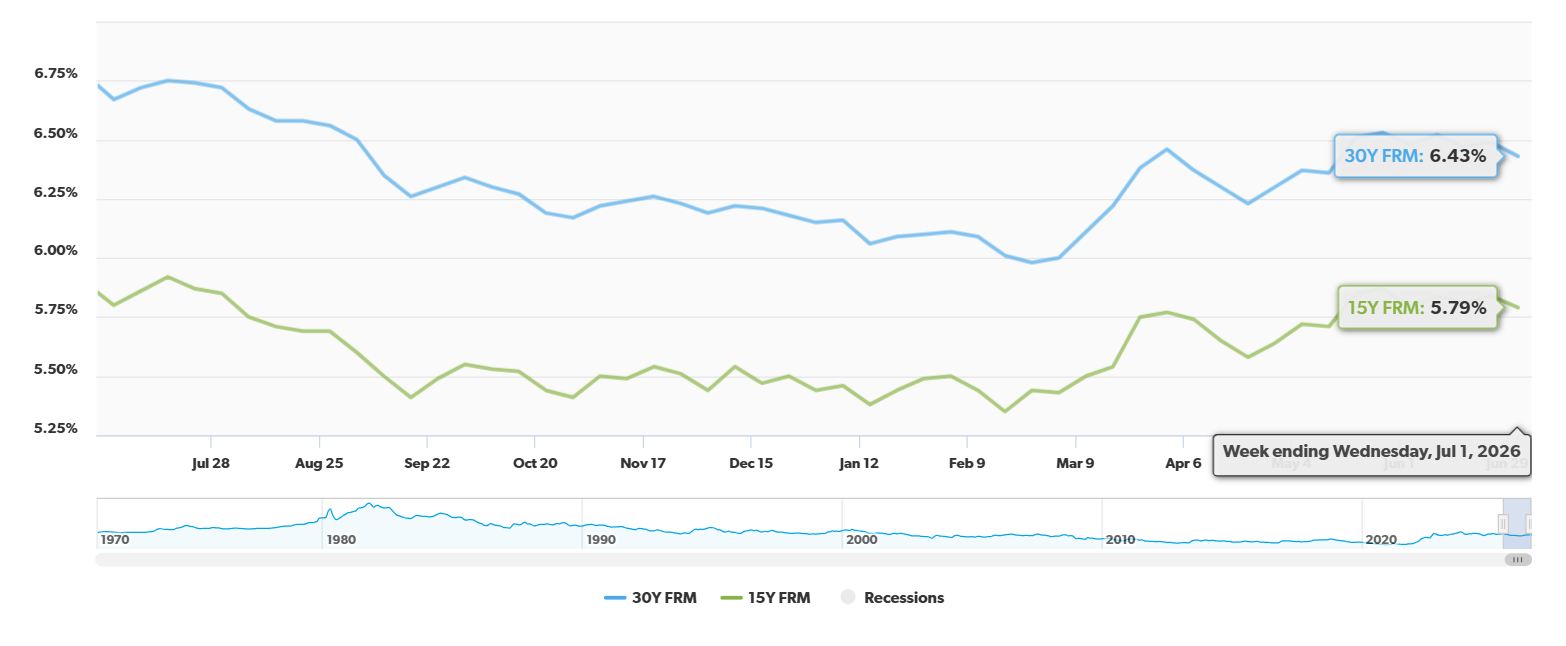

It’s always good to have the numbers handy, right? Here’s a snapshot of what mortgage rates are looking like today, according to the latest data from Zillow:

| Loan Type | Current Rate | Change from Yesterday |

|---|---|---|

| 30-year fixed | 6.36% | Down 4 basis points |

| 20-year fixed | 6.24% | – |

| 15-year fixed | 5.83% | Down 3 basis points |

| 5/1 ARM | 6.31% | Down 21 basis points |

| 7/1 ARM | 6.24% | – |

| 30-year VA | 5.76% | – |

| 15-year VA | 5.49% | – |

| 5/1 VA | 5.82% | – |

You might be wondering, why the small drop? Well, it seems like some recent economic news has made lenders a bit more willing to offer slightly lower rates. The jobs report from June came out a little cooler than expected, which has helped bring down what are called 10-year Treasury yields. Think of Treasury yields as a kind of guide for how much it costs lenders to borrow money. When those go down, mortgage rates can often follow suit.

Why Rates Are Still Higher Than We'd Like

Even though we’re seeing a tiny bit of relief, it’s important to remember that long-term trends are still keeping mortgage rates higher than they were a couple of years ago. There are a few big reasons for this, and understanding them can help you make smarter decisions about your home buying or refinancing plans.

- Global Worries: We’ve had some tricky situations around the world with military conflicts. When these things happen, it can make oil prices jump up, and that makes everything more expensive. This global uncertainty makes lenders a bit nervous, and they tend to charge more for loans.

- Prices Still Climbing: You’ve probably noticed that things cost more at the grocery store or the gas pump. This is what we call inflation. The government’s goal is to keep prices growing slowly and steadily, but right now, prices are going up faster than they’d like. The Consumer Price Index (CPI), which is a way to measure this, is running pretty high.

- The Fed's Steady Hand: Because inflation is still a concern, the Federal Reserve (that’s the big bank for banks in our country) has decided to keep its main interest rate from going down. They’ve been holding it steady at recent meetings. When the Fed keeps its rates high, it usually means other borrowing costs, like mortgages, will also stay elevated.

As someone who’s been following the housing market for a while, I can tell you that these bigger economic forces have a huge impact. It's not just about one day's numbers; it's about the overall picture.

Is It Time to Refinance? Let's Figure It Out.

Seeing rates dip can make you think, “Should I refinance my mortgage?” It's a great question, and the answer really depends on your personal situation. Here's a simple way I like to look at it.

The 1% Rule: A Simple Test

A good rule of thumb is the 1% rule. If you can refinance your mortgage and get an interest rate that's at least 1 percentage point lower than what you have now, it usually makes sense financially. For example, if you got your mortgage when rates were really high, maybe near 8% back in late 2023, refinancing now at 6.36% could save you a significant amount of money over the life of your loan.

Finding Your Break-Even Point

Refinancing isn't free. There are always closing costs involved. To figure out how long it will take for your monthly savings to pay off those costs, you can do a quick calculation:

- Divide your total refinancing closing costs by your projected monthly savings.

Let's say your closing costs add up to $6,000, and you expect to save $200 each month on your mortgage payment. In this example, you would need to stay in your home for 30 months (that's 2.5 years) to make back the money you spent on closing costs. If you plan to stay in your home for longer than that, refinancing is likely a good move.

Consider a Shorter Loan Term

If your budget allows, have you thought about switching to a 15-year fixed mortgage? Even though the monthly payments might be higher, the interest rate on a 15-year loan is often lower than on a 30-year loan. Right now, the 15-year fixed rate is 5.83%, which is a great deal! By choosing a shorter term, you'll pay off your home much faster and save a huge amount of money on interest over the years. I've seen many homeowners make this switch and feel so much better about their financial future.

Shop Around! It Really Matters

This is perhaps the most important advice I can give you: don't just go with the first lender you talk to. Getting quotes from at least three different lenders is crucial. Rates and fees can vary quite a bit, and comparing offers can save you tens of thousands of dollars over the life of your loan. It takes a little extra effort, but the payoff is well worth it. I always tell people to think of it like getting quotes for car insurance – you wouldn't just take the first price you see, right?

What This Means for You

Today's mortgage rates offer a glimmer of hope for those looking to buy or refinance. While rates are still influenced by broader economic factors that keep them from dropping dramatically, the slight decline is a positive sign. My advice? If you're considering a move or looking to lower your monthly payments, now is a good time to research your options, run the numbers, and start comparing offers. Understanding the forces at play will empower you to make the best decision for your financial well-being.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?