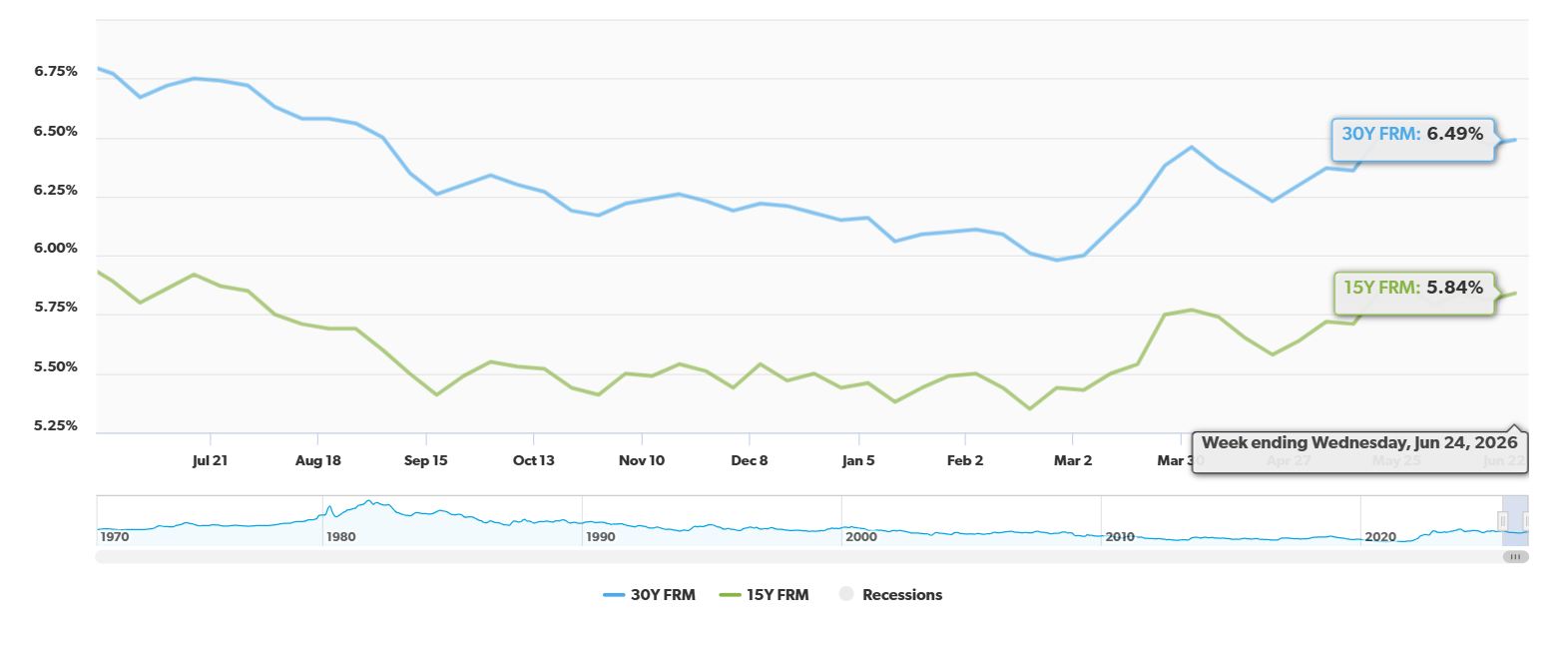

Well, it looks like those lower mortgage refinance rates many of us were hoping for have taken a step back. As of today, July 3, 2026, the average rate for a 30-year fixed refinance has nudged up by 8 basis points from last week, landing at 6.82%. This uptick, reported by Zillow, means that if you're thinking about refinancing your home to get a better deal on your mortgage, now might not be the most opportune moment.

Mortgage Rates Today, July 3, 2026: 30‑Year Refinance Rate Rises by 8 Basis Points

It’s a bit of a bummer, I know. Many of us were really looking forward to that “refi boom” that seemed to be on the horizon. Back in late February and early March, we saw rates dip to their lowest point in three years, just shy of 6.0%. That felt like a golden ticket for homeowners looking to save some serious cash on their monthly payments. But as we're seeing now, rates can be quite jumpy, and the relief we felt was shorter-lived than we’d hoped.

Why Are Rates Going Up Again?

It’s never just one thing, is it? Several factors are playing a role in pushing these rates higher and keeping them from falling back down.

- Global Jitters: Sadly, there's a lot of unrest in the world right now. The ongoing conflict in Iran, for example, has really messed with supply chains and sent oil prices soaring. When oil prices go up, it often fuels inflation fears, which, in turn, can make lenders a bit nervous.

- Inflation Won't Quit: Speaking of inflation, it’s proving to be quite stubborn. Even though it’s been a while, inflation is still a bit higher than what economists consider ideal. When inflation is high, it puts upward pressure on interest rates for longer-term loans, like mortgages.

- The Fed's Cautious Approach: Remember when the Federal Reserve cut rates a few times back in late 2025? Well, they've been holding steady on those cuts this year. They seem to be taking a very careful, “wait-and-see” approach, and this caution means borrowing costs are staying elevated.

- Treasury Yields: The 10-year Treasury yield is like a big signpost for mortgage rates. Lately, lenders have been feeling a bit anxious about the economy, and this has caused the difference – what we call the “spread” – between Treasury yields and mortgage rates to widen. It's currently sitting at a pretty large 2.0 percentage points, which also pushes mortgage rates up.

Is Refinancing Still a Good Idea Right Now?

This is the big question on everyone's mind. With rates climbing again, it’s trickier to figure out if refinancing makes sense for your specific situation. It’s not a one-size-fits-all answer anymore.

Here’s what I look at when I’m helping folks decide:

Key Factors to Consider Before Refinancing

| Factor | What to Aim For | Why It Matters |

|---|---|---|

| Current Loan Rate | Needs to be higher than your current rate. | To actually save money each month. |

| Home Equity Level | More than 20% equity is ideal. | Helps you avoid paying Private Mortgage Insurance (PMI). |

| “1% Rule” Savings | At least a 1% drop in your interest rate. | Historically, this is a good benchmark for seeing real savings. |

| Break-Even Point | You can recoup closing costs quickly. | Make sure your monthly savings outweigh the upfront fees. |

| Credit Score | Mid-to-high 700s or better. | Lenders are picky, and good credit gets the best rates. |

Calculating Your Savings: The Break-Even Point

Refinancing isn't free. There are always closing costs, which can add up to anywhere from 2% to 5% of your loan amount. My advice? Take those closing costs and divide them by how much you'll save each month with a new, lower rate. That number tells you how many months you need to stay in your home to get your money back. If that number is really high, and you’re thinking of moving soon, it might not be worth it.

The “1% Rule” and Who Benefits Most

You might have heard of the “1% rule.” It basically says that refinancing is usually a good move if you can lower your interest rate by at least 1 whole percentage point. Given how many of us locked in super low rates during the pandemic (think below 5%), refinancing right now to lower your rate even further isn't likely to benefit most people.

However, if you happened to take out a loan when rates were at their peak last year, maybe around 7.5% or 8%, then refinancing to today’s 6.82% (or potentially even lower if you have stellar credit and a good loan scenario) could absolutely make financial sense. You're in a much better position to see significant savings.

Your Credit Score Matters More Than Ever

Lenders are definitely tightening things up in this uncertain market. The lowest advertised rates? They’re really reserved for folks with top-notch credit scores, usually in the mid-to-high 700s. If your credit score has taken a hit, those extra fees lenders might add because of lower creditworthiness could wipe out any potential savings you were hoping to get from refinancing.

Cash-Out Refi vs. Other Options

Sometimes, people don’t just want to lower their rate; they want to pull some cash out of their home equity for other needs.

- Cash-Out Refinance: If you do a cash-out refinance, you're essentially trading in your current mortgage, even if it has a low rate, for a brand new, higher-rate loan. With rates hovering around 6.82% for a 30-year fixed, this might not be the most cost-effective way to access your equity right now.

- Home Equity Line of Credit (HELOC) or Home Equity Loan: These options are often a much smarter choice in today's environment. A HELOC or a home equity loan lets you borrow against your home's value without touching your primary mortgage. This means you can keep that lower rate on your main loan while still getting the funds you need. The rates on these can sometimes be more favorable than a full cash-out refinance.

Current Refinance Rates (as of July 3, 2026)

Here's a quick look at what Zillow reported for national averages today:

| Loan Type | Average Rate | Change from Last Week |

|---|---|---|

| 30-Year Fixed Refinance | 6.82% | Up 8 basis points |

| 15-Year Fixed Refinance | 5.90% | Up 11 basis points |

| 5-Year ARM Refinance | 6.00% | No change noted |

Looking Ahead

The experts, like those at Fannie Mae, are predicting that rates will likely stay “sticky” – meaning they won't drop dramatically – and will probably hover above 6% for the rest of the year. This suggests that the window for super-low refinance rates might have closed for now.

It’s a dynamic market, and staying informed is key. Keep an eye on economic news, inflation reports, and what the Federal Reserve is saying. And most importantly, always run the numbers for your own situation before making any big decisions about refinancing.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?