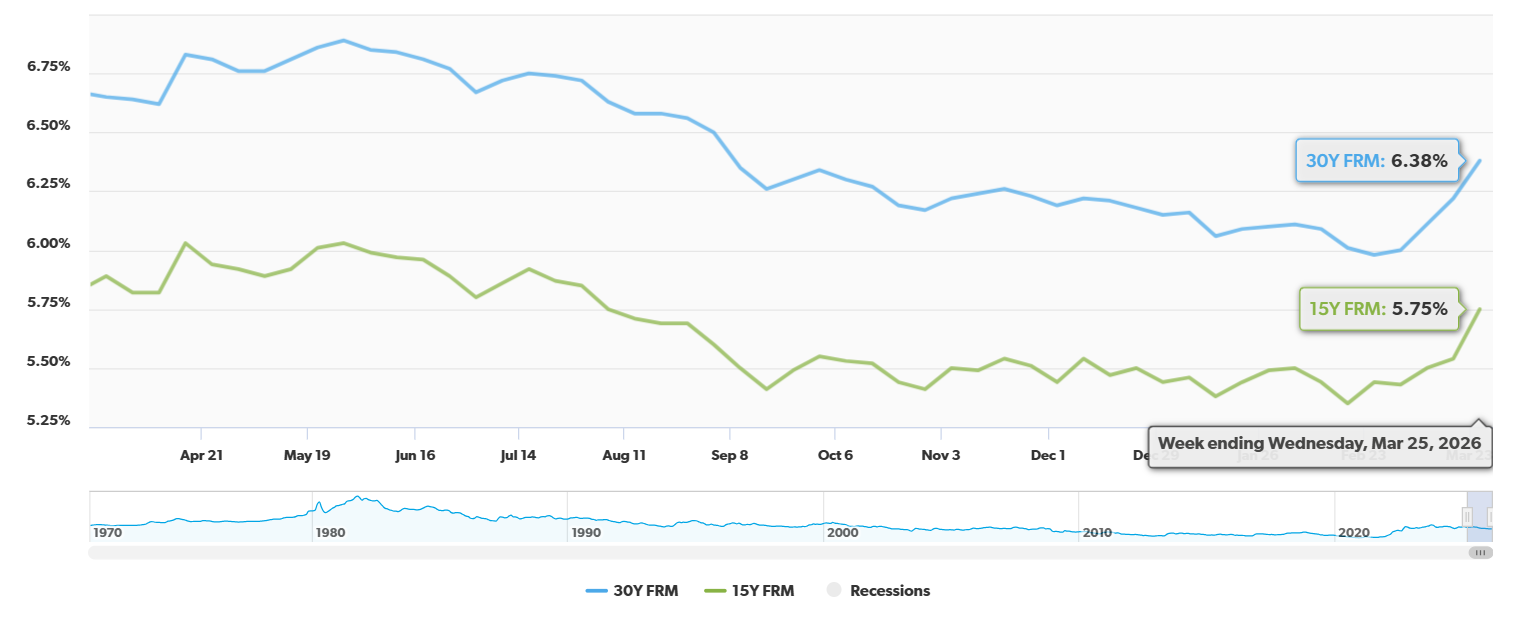

If you've been thinking about buying a home or refinancing your current mortgage, you've likely noticed that borrowing money just got a bit more expensive. For the week ending March 26, 2026, the average rate for a 30-year fixed mortgage jumped up by a significant 16 basis points, hitting 6.38%. This is the highest we've seen this particular rate since way back in September of last year. This isn't just a small blip; it's a noticeable uptick that could impact many people's homeownership dreams and financial plans.

30-Year Fixed Mortgage Rate Rises Steeply by 16 Basis Points

As someone who's spent years following the housing market, I can tell you that these kinds of moves, especially when they're sudden and substantial, always get my attention. It's easy to get lost in the numbers, but I believe it's crucial to understand the “why” behind these changes and, more importantly, “what it means for you and me.”

What's Driving This Rate Jump?

It feels like just yesterday we were celebrating slightly lower rates, and now we're seeing this upward trend. So, what's causing this sudden climb? Quite a few things, it turns out, and they're all interconnected, creating a bit of a ripple effect.

One of the biggest hats being thrown into the ring is the ongoing geopolitical situation. The continued conflict involving Iran has unfortunately thrown the global economy into a state of uncertainty. This “war outlook” tends to make lenders nervous, and when lenders get nervous, borrowing costs tend to go up. It's a classic case of supply and demand, with a healthy dose of fear thrown in.

Then there's the immediate impact of this conflict on energy prices. We've seen oil prices surge, topping $100 a barrel. When oil gets this expensive, it has a domino effect on almost everything else. It fuels inflation, making the cost of goods and services go up. Financial markets have to react to this, and one of their reactions is to reassess how high interest rates might need to go to keep inflation in check.

This brings us to the bond market, specifically the 10-year Treasury yield. This is a really important benchmark that mortgage rates often follow. Right now, the 10-year Treasury yield has also climbed, reaching its highest point since July 2025. Why? Again, it's tied to inflation fears and those unsettling headlines coming out of the Middle East. When investors demand a higher return for lending their money to the government (which is essentially what buying a Treasury bond is), it signals that interest rates are likely to move higher across the board, including for mortgages.

And of course, we can't forget about the Federal Reserve. While they decided to keep interest rates steady in March 2026, the persistent inflation-related concerns mean that any hopes of quick rate cuts in the near future are fading. The current projection for inflation for the year is around 4.2%, which is still a bit higher than what the Fed typically aims for. This steady stance from the Fed, combined with other inflationary pressures, naturally pushes mortgage rates upward.

A Closer Look at the Numbers

To really understand the shift, let's break down the numbers a bit. Freddie Mac, a major player in the housing finance world, collects this data, and their most recent report sheds some light:

Key Mortgage Rate Data (Freddie Mac) – As of March 26, 2026

| Mortgage Type | Current Average Rate | Last Week's Average | One Year Ago Average |

|---|---|---|---|

| 30-Year Fixed-Rate Mortgage (FRM) | 6.38% | 6.22% | 6.65% |

| 15-Year Fixed-Rate Mortgage (FRM) | 5.75% | 5.54% | 5.89% |

As you can see, both the 30-year and 15-year fixed rates have seen increases from the previous week. While the current 30-year rate is still lower than it was a year ago, that jump from last week is definitely something to note.

To give you a clearer picture of the weekly and yearly changes, and a hint at how these shifts can impact your wallet, here's a table:

Mortgage Rate Changes and Potential Savings Impact

| Metric | 30-Year Fixed-Rate Mortgage (FRM) | 15-Year Fixed-Rate Mortgage (FRM) |

|---|---|---|

| 1-Week Change | +0.16% | +0.21% |

| 1-Year Change | -0.27% | -0.14% |

| Monthly Avg. | 6.18% | 5.56% |

| 52-Week Avg. | 6.42% | 5.65% |

| Savings Impact | A 0.16% increase on a $300,000 loan over 30 years translates to roughly an extra $27 per month in payments. Over the life of the loan, that adds up to nearly $10,000 more in interest. | A similar percentage increase on a 15-year mortgage, while perhaps a smaller absolute dollar amount monthly, still means more interest paid over time. |

Note: Savings impact is an approximation and can vary based on loan principal and other factors.

It's these numbers that make me pause. While the one-year change for the 30-year fixed is still a bit of a relief, that recent 16 basis point jump feels like a step backward, especially if you were just about to pull the trigger on a home purchase.

The Impact on the Housing Market

What does all of this mean for the actual housing market? Well, it's not exactly good news for those hoping for a robust spring buying season. The data shows a clear consequence:

- Application Slowdown: We've seen a 10.5% drop in total mortgage application volume just this week. When rates go up, it tends to make people hesitant. Buyers might put their search on hold, and homeowners considering refinancing might decide to wait it out, hoping for better rates down the line.

- Affordability Barrier: Experts from Realtor.com have pointed out that these rising rates are now the “primary barrier” to a smooth spring homebuying season. Even though there might be more homes on the market and some prices might be coming down, the increased cost of borrowing can effectively cancel out those benefits for many potential buyers.

From my perspective, this creates a bit of a tricky situation. We have factors like increased inventory and some price moderation, which should be good for buyers. But when the cost of getting that loan spikes, it can really dampen enthusiasm. It's like having a great sale on a car, but then the financing rates suddenly shoot up – it makes the overall deal less attractive.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?