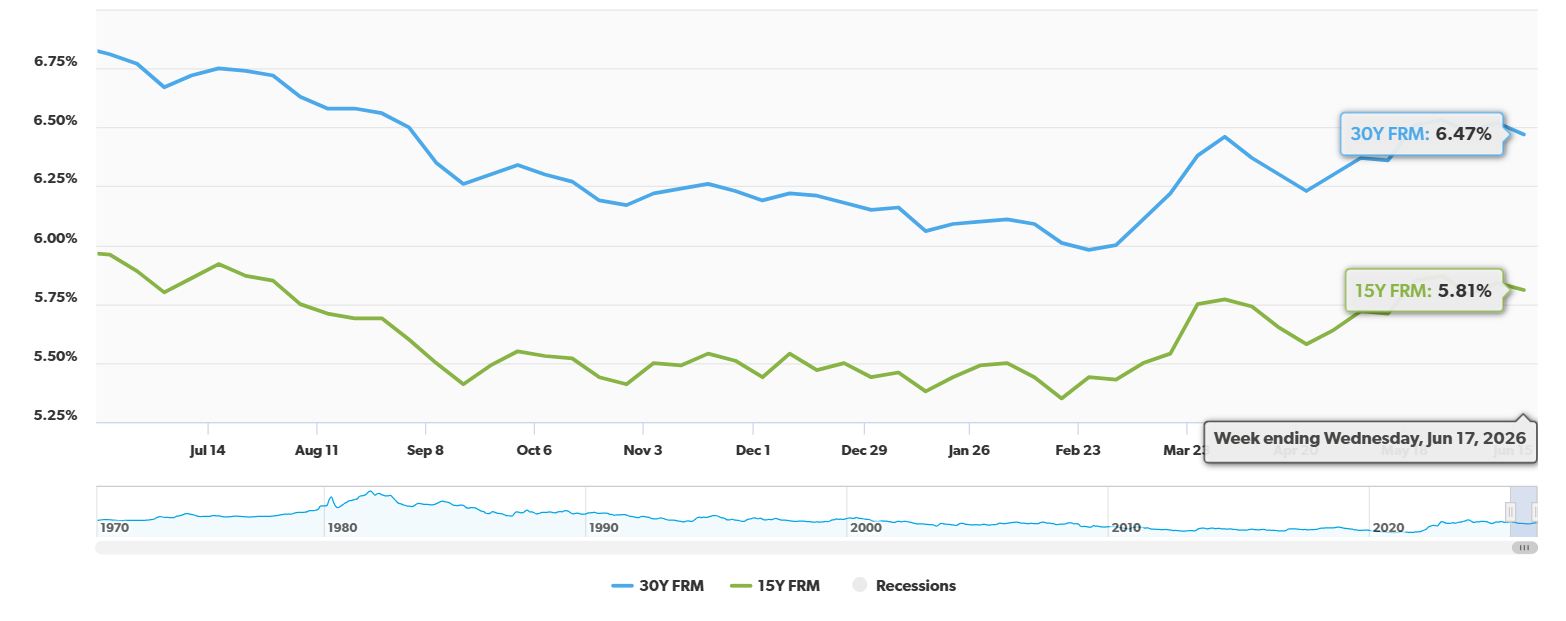

It's a bit of a mixed bag out there for homebuyers and homeowners looking to refinance today, June 24, 2026. If you're eyeing a new home or thinking about a mortgage refinance, you'll want to know that fixed mortgage rates have seen a slight uptick compared to yesterday. Specifically, the popular 30-year fixed-rate purchase loan has climbed, while the 15-year fixed and 5/1 ARM also moved higher, according to Zillow's latest data.

I can tell you that these daily shifts, while sometimes small, are part of a bigger picture. They're influenced by a lot of factors – from what's happening with inflation and the Federal Reserve to global events. Understanding these drivers can help you make more informed decisions about when to lock in a rate.

Today's Mortgage Rates, June 24: Fed Policy and Inflation Push Rates Higher Across Loan Types

Let's break down the numbers as of Wednesday, June 24, 2026, based on Zillow's data:

| Loan Type | Rate | Change from Yesterday |

|---|---|---|

| 30-year fixed | 6.43% | +8 basis points |

| 20-year fixed | 6.08% | N/A |

| 15-year fixed | 5.88% | +2 basis points |

| 5/1 ARM | 6.56% | +7 basis points |

| 7/1 ARM | 6.33% | N/A |

| 30-year VA | 5.87% | N/A |

| 15-year VA | 5.39% | N/A |

| 5/1 VA | 5.66% | N/A |

As you can see, the 30-year fixed mortgage rate is hovering around 6.43%, marking an increase. The 15-year fixed, often a go-to for those looking to pay off their home faster, also nudged up to 5.88%. Adjustable-rate mortgages (ARMs), like the 5/1 ARM, have also seen a rise to 6.56%.

Why Are Rates Moving Today? Unpacking the Key Influences

It’s never just one thing that moves mortgage rates. Think of it like a complex recipe – many ingredients contribute to the final taste. Here’s what I see as the main ingredients influencing today’s rates:

- Stubborn Inflation and a Strong Job Market: The economy is showing resilience, and that's a double-edged sword for mortgage rates. The latest Consumer Price Index (CPI) report showed inflation at a faster pace than we’ve seen in over three years, coming in at 4.2% annually. On top of that, the job market remains robust, with a solid number of new jobs added in May. While good for the economy, this strength suggests that consumer demand is still high, making it tough for inflation to cool down to the Federal Reserve's target of 2%.

- The Federal Reserve's New Stance: The Federal Reserve, under its new leadership, has signaled a significant shift. While they decided to keep their benchmark interest rate steady at their recent meeting, the tone has changed. They've removed language that suggested a potential for rate cuts, and more importantly, their updated projections (“dot plot”) show that a majority of officials now anticipate a rate hike by the end of 2026. This hawkish pivot means the Fed is more focused on fighting inflation, which generally pushes borrowing costs, including mortgage rates, higher. Big banks are even revising their forecasts to predict multiple rate hikes this year.

- Treasury Yield Volatility: It's crucial to understand that mortgage rates don't directly follow the Fed's short-term rates. Instead, they tend to track the yield on the 10-year U.S. Treasury note. This yield has been a bit of a rollercoaster lately, fluctuating around 4.45% to 4.51%. When investors become concerned that the Fed might raise rates, they often sell off bonds, which drives bond prices down and yields up. This directly translates to higher mortgage rates.

- Global Geopolitical Ripples: The ongoing conflict involving Iran has certainly added to market uncertainty this spring. Initially, it disrupted global energy supplies, sending oil prices up and contributing to the inflation we're seeing. However, there’s a glimmer of positive news today: reports suggest that the U.S. and Iran have agreed on a plan to negotiate an end to the conflict. This de-escalation in geopolitical tensions has helped calm investor nerves, leading to a slight dip in the 10-year Treasury yield. This is a welcome development that might offer some temporary relief on the rate front.

My Take: What Does This Mean for You?

From my perspective, today's mortgage rates reflect a market that's still trying to find its footing. We're seeing the tug-of-war between a strong economy and the persistent challenge of inflation. The Federal Reserve's more assertive stance against inflation is a key factor to watch.

For those looking to buy a home, it means that affordability could become a greater concern if rates continue to climb. It underscores the importance of getting pre-approved and understanding your budget thoroughly. If you were hoping for rates to drop significantly in the short term, today's data suggests that might not be on the immediate horizon.

If you're considering refinancing, the slight uptick might make you pause. However, it’s always worth comparing current rates to your existing mortgage. Even a small decrease can lead to significant savings over the life of a loan. Don't get discouraged by a small daily fluctuation; look at the broader trend and your personal financial goals.

The good news is that the recent easing of geopolitical tensions is a positive sign. If this trend continues, it could provide some stability to the markets and potentially put a lid on rapidly rising rates.

Key Takeaways:

- Rates are up slightly today, particularly for 30-year fixed mortgages.

- Inflation and the Fed's actions are the primary drivers pushing rates higher.

- Global events can have a direct impact on mortgage rates.

- Stay informed and consult with a mortgage professional to understand how these changes affect your specific situation.

VS

Out‑of‑State investors can compare Tennessee’s newer rental with higher NOI vs Florida’s A+ property with strong yield. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?