It’s a moment many prospective homebuyers have been waiting for: the 30-year fixed mortgage rate, despite a slight uptick this week, is showing a robust 46 basis point decrease year-over-year, a significant drop that’s making homeownership feel more accessible again, even with the economic storms brewing. This is fantastic news for anyone looking to finance a home, as it represents a tangible improvement in affordability that we haven't seen in a while.

30 Year Fixed Mortgage Rate Drops Steeply by 46 Basis Points Year-Over-Year

A Welcome Downturn: What Those Numbers Really Mean

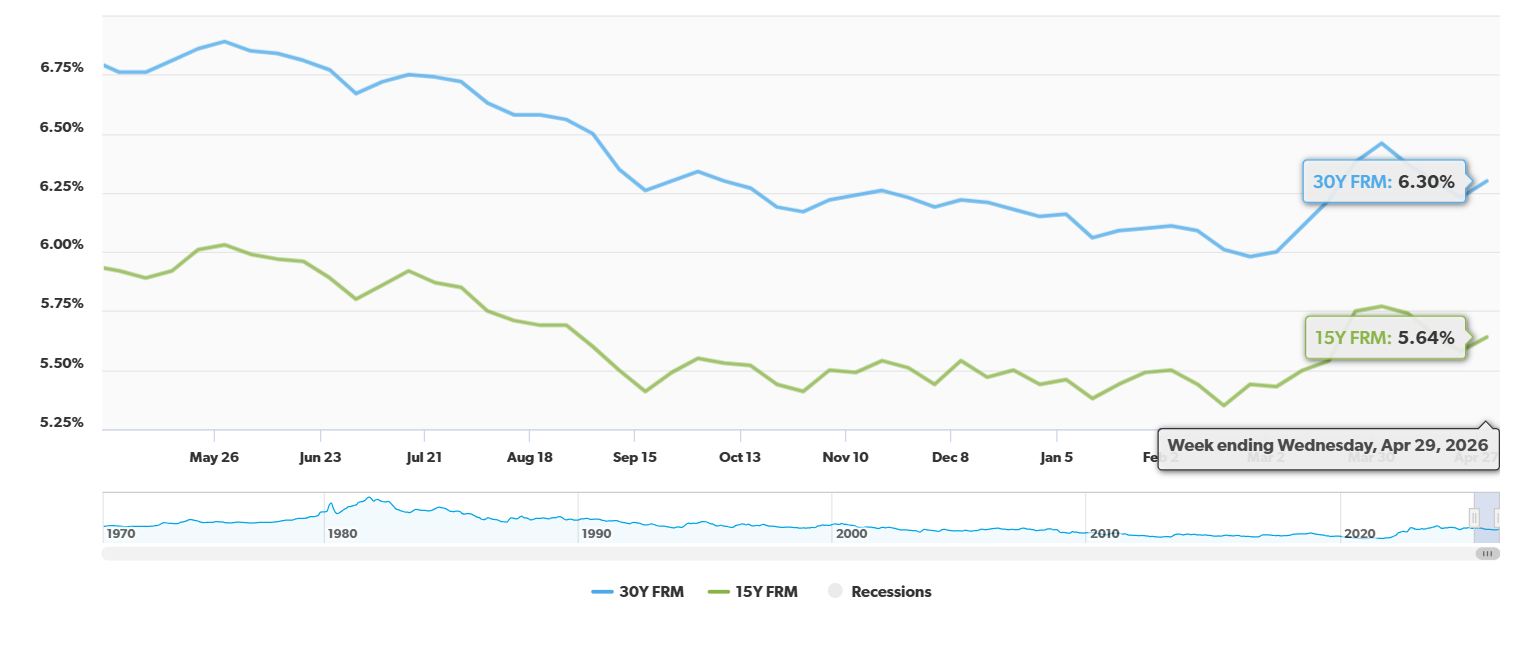

Let's break down what's happening. According to the latest data from Freddie Mac, for the week ending April 30, 2026, the average rate for a 30-year fixed mortgage landed at 6.30%. Now, you might notice that this is a slight jump – 7 basis points, to be exact – from the week prior (where it was 6.23%). On the surface, a small increase can sound discouraging.

But here’s where it gets interesting and, frankly, quite encouraging: when you zoom out and compare it to the same week last year, that figure stood at 6.76%. That means, while we saw a minor weekly wobble, the big story is the significant 46 basis point decline year-over-year. That’s a substantial chunk of percentage points, and it translates into real savings for borrowers. For me, this signals a market that's trying to find its footing, offering a much-needed lifeline to buyers.

Why the Seemingly Mixed Signals? Understanding Market Dynamics

This situation, where rates move up slightly one week but are down significantly over a longer period, isn't uncommon. The mortgage market is a bit like a boat navigating choppy seas. There are always waves (weekly fluctuations) and larger currents (year-over-year trends).

The Freddie Mac report itself highlights these nuances. While the average rate for a 30-year fixed mortgage is 6.30% as of April 30, 2026, it's important to remember this followed a three-week decline. The real win is that year-over-year, we're seeing a 6.76% rate from a year ago plummeting to 6.30% today. That's a definite step in the right direction.

The “Headwinds in 2026” and Their Impact

The headline mentions “headwinds in 2026,” and this is where the real insight comes in. What are these headwinds? Market watchers and analysts, including those cited by FOX Business and U.S. News, point to ongoing geopolitical tensions and the subsequent volatility in long-term Treasury yields. These are the bigger, more unpredictable forces that can cause rates to sway. Think of it like this: global events can make investors nervous about where their money is safest, and that nervousness directly impacts the cost of borrowing money for things like mortgages.

Even with these external pressures, the fact that we're still seeing such a significant annual rate decrease is a testament to the underlying economic forces at play, which are generally more favorable for borrowers than they were last year.

Buyer Demand Soars: A Direct Result of Lower Rates

Perhaps the most telling sign that this drop in rates is having a real impact is the surge in buyer demand. The report proudly states that purchase applications are currently running over 20% above year-ago levels. This isn't just a small bump; it's a strong indication that more people are actively looking to buy homes.

What's fueling this increased demand? Two key factors mentioned are improved inventory and, of course, those overall lower rates compared to previous spring buying seasons. For years, inventory has been a major bottleneck. When more homes become available, it eases competition and can help stabilize prices. Combine that with more affordable financing, and you have a recipe for increased buyer activity. From my perspective, this is the market responding positively to improved conditions. It's a cycle: lower rates make buying more attractive, which brings more buyers into the market, and that enthusiasm can encourage more sellers to list their homes.

Beyond the 30-Year: Trends in Other Mortgage Types

It's not just the iconic 30-year fixed-rate mortgage that's showing improvement. The 15-year fixed-rate mortgage is following a similar, welcome trend. For the week ending April 30, 2026, it averaged 5.64%. Like its longer-term counterpart, this is up slightly from 5.58% the previous week. However, the year-over-year picture is again the compelling story: it’s down from 5.92% recorded a year ago. This offers even more options for those looking for shorter repayment terms and lower overall interest paid over the life of a loan.

The Economic Forecast: What Freddie Mac and Analysts Predict

Looking ahead, the outlook, while acknowledging the “headwinds,” remains cautiously optimistic. Freddie Mac's own Q1 2026 report reveals a company in strong financial health, with a notable $3.6 billion in net income. This financial stability is crucial for the housing market. Furthermore, they forecast a 2.3% projected house price growth for the year. This suggests a balanced market, avoiding the rampant price increases of some past years, which is good for long-term stability.

The broader analysis points towards a gradual improvement in affordability throughout 2026. Factors contributing to this include a projected 7.1% increase in inventory and the expectation that mortgage rates will continue on a downward trajectory as inflation is anticipated to cool. This is the nuanced outlook that experienced market participants follow – a blend of short-term fluctuations and longer-term trends driven by fundamental economic indicators.

My Take: A Balanced Market Finding its Equilibrium

As someone who's followed the housing market for a while, this data tells me a story of recovery and stabilization. The 30-year fixed mortgage rate's impressive year-over-year drop of 46 basis points is the headline, and rightly so. It signifies a real shift towards affordability. The weekly uptick is just noise in the grand scheme, common in any dynamic market.

The strength in purchase demand, exceeding year-ago levels by over 20%, is the undeniable proof that buyers are responding. They're seeing an opportunity. While geopolitical issues and other economic “headwinds” are real and will continue to cause some bumps, the underlying trend seems to be one of cautious optimism. The fact that Freddie Mac is doing well and predicting growth, alongside a rise in inventory and a cooling inflation outlook, paints a picture of a housing market that is actively working towards finding a more sustainable equilibrium. For anyone considering a move, this period presents a potentially golden opportunity.

VS

Alabama’s new build with solid cap rate vs Georgia’s affordable rental with stronger NOI. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain near 6%, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Will Mortgage Rates Drop to 5% in 2026: Expert Forecast

- How to Get a 3% Mortgage Rate in 2026 With Assumable Mortgages?

- How to Get a 4% Interest Rate on a Mortgage in 2026?

- What Leading Housing Experts Predict for Mortgage Rates in 2026

- Mortgage Rate Predictions for 2026: What Leading Forecasters Expect

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?