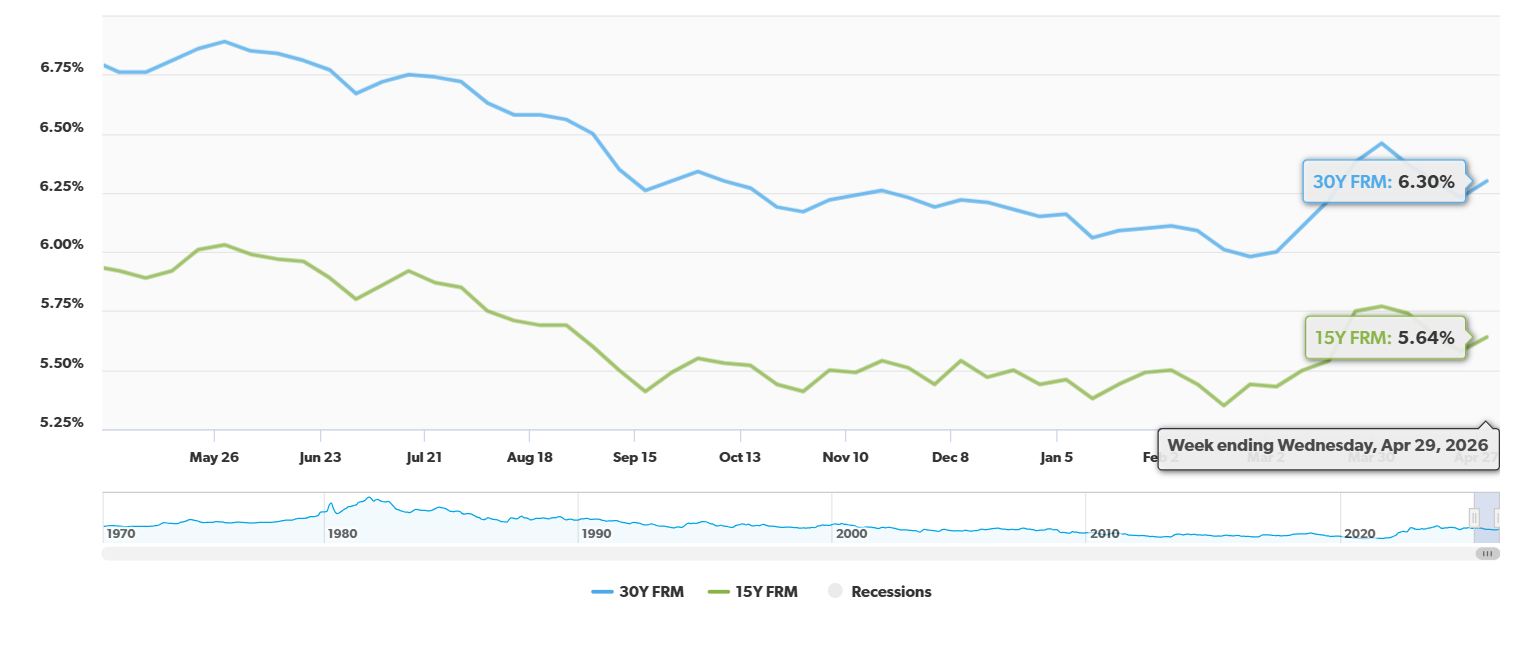

Let's talk about what's happening with mortgage rates today, Friday, May 1, 2026. If you're thinking about refinancing your home, you'll want to know that the 30-year fixed refinance rate has nudged up by 10 basis points compared to last week, settling at 6.62%. While this is a slight increase, it's important to remember that this rate is still a far cry from the peaks we saw not too long ago.

Today's rates show a little bit of mixed movement, with some loans going up and others down, but the big story for many is that key 30-year rate climbing a bit this week.

Mortgage Rates Today, May 1, 2026: 30‑Year Refinance Rate Inches Up

What the Numbers Are Telling Us

So, what exactly are the rates looking like today? According to the latest data from Zillow, here's a snapshot of the national averages for refinancing:

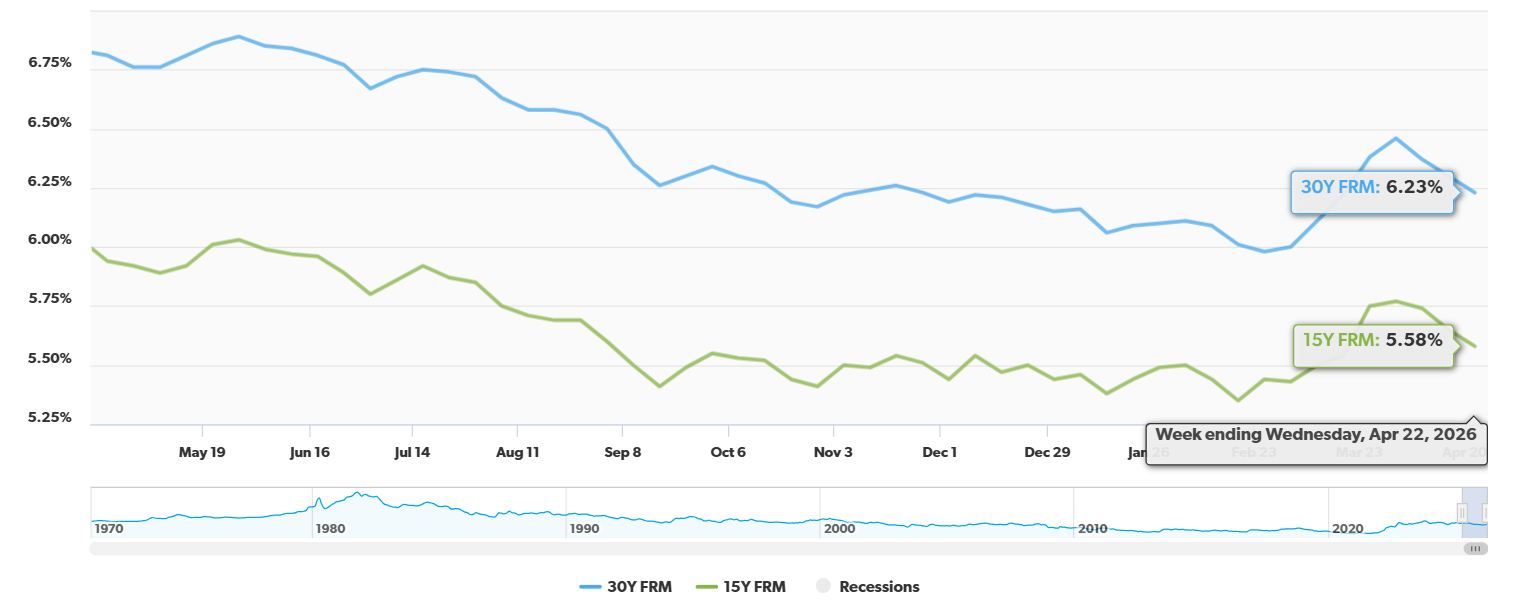

- 30‑Year Fixed Refinance: Currently at 6.62%. This is actually down by 2 basis points from yesterday's 6.64%, which is good news for a quick turnaround. However, looking back at last week, when it was 6.52%, we see that 10 basis point increase.

- 15‑Year Fixed Refinance: This rate is holding steady at 5.69%, just a tiny tick up from yesterday's 5.68%.

- 5‑Year Adjustable-Rate Mortgage (ARM) Refinance: This one is a real bright spot! It's down a notable 37 basis points from 7.25% down to 6.88%. This is a significant drop and could be a great opportunity for some borrowers.

The 30-year fixed rate's rise over the week is something many homeowners will be paying attention to, especially those looking to lower their monthly payments. It shows that the market isn't just going in one direction.

Refinance Activity: A Look at the Demand

It seems like the recent uptick in rates has cooled things down a little bit when it comes to how many people are applying to refinance. The Mortgage Bankers Association (MBA) reported that refinance application volume dipped between 1.7% and 4% for the week ending April 24th. This isn't a huge shocker, as borrowers often pause when they see rates starting to climb.

However, and this is a crucial point, things are still much busier than they were a year ago. Refinance activity is actually 51%–52% higher year-over-year. This tells me that even with these small bumps, current rates are still way more appealing than the really high rates we experienced towards the end of 2023. People are still taking advantage of the savings, even if they're being a little more cautious.

In terms of market share, refinancing now makes up 42.5% of all mortgage applications. This is down just a bit from 44.2% the week before, which again, shows that slight slowdown.

What's Driving These Rate Movements?

I often get asked, “Why are rates doing what they're doing?” It's a complex puzzle, but a few key pieces are really shaping today's mortgage rates.

- Bond Yields: The 10-year Treasury yield is currently at 4.404%, and it's been climbing. Think of Treasury yields as a benchmark for many other interest rates, including mortgages. When they go up, mortgage rates tend to follow.

- Global Events and Inflation: We're still seeing some uncertainty in the world, particularly tied to the Middle East. This has kept oil prices higher, around $104.82/barrel. Higher oil prices mean higher costs for transportation and many goods, which can fuel inflation. When inflation is a concern, lenders become more hesitant to offer lower rates because the money they get back might be worth less.

- The Federal Reserve's Stance: The Federal Reserve has been playing a careful hand. After making a few interest rate cuts late last year, they've decided to hold steady. Their current target rate is 3.50%–3.75%. This “wait-and-see” approach from the Fed signals that they're not rushing to lower borrowing costs significantly, which in turn puts a lid on how low mortgage rates can go.

What This Means for You

So, what’s the takeaway for homeowners and potential refinancers?

- For Homeowners with Higher Rates: If your current mortgage rate is above 7%, you are likely still in a very good position to benefit from refinancing. However, the recent slight increase means that timing is becoming more critical. You don't want to wait too long and miss out on the savings you could be getting.

- For Those Considering ARMs: That sharp drop in the 5-year ARM rate to 6.88% is definitely worth exploring. ARMs can be a great option if you plan to move or refinance again before the fixed period ends. But remember, these rates can go up after the initial period, so it's crucial to understand the long-term risks and your own financial situation.

- Looking Ahead: With Treasury yields showing an upward trend and inflation remaining a concern, I’m not expecting a dramatic drop in mortgage rates anytime soon. It seems likely that rates might hang out in the mid-6% range for a while. This means that opportunities to refinance at a significantly lower rate might be fewer and farther between. Being strategic and ready to act when you see a good rate window is key.

In Summary: On May 1, 2026, the 30-year fixed refinance rate is at 6.62%. It's up a bit from last week, even though it ticked down slightly today. Refinance demand has slowed a little, but it’s still way stronger than this time last year. With the Federal Reserve holding steady, oil prices staying up, and Treasury yields climbing, we’re likely to see continued ups and downs in rates. The best advice I can give is to stay informed, know your goals, and be ready to jump on a good rate when it appears.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?