It's a busy market out there for homeowners looking to refinance their mortgages. On May 10, 2026, the headline news for many is that the popular 30-year fixed refinance rate has nudged up by 3 basis points, now sitting at 6.59%. This might seem like a small change, but in the world of mortgages, every tenth of a percent can add up to significant savings over the life of a loan, or conversely, represent a missed opportunity.

Mortgage Rates Today, May 10, 2026: 30-Year Refinance Rate Rises by 3 Basis Points

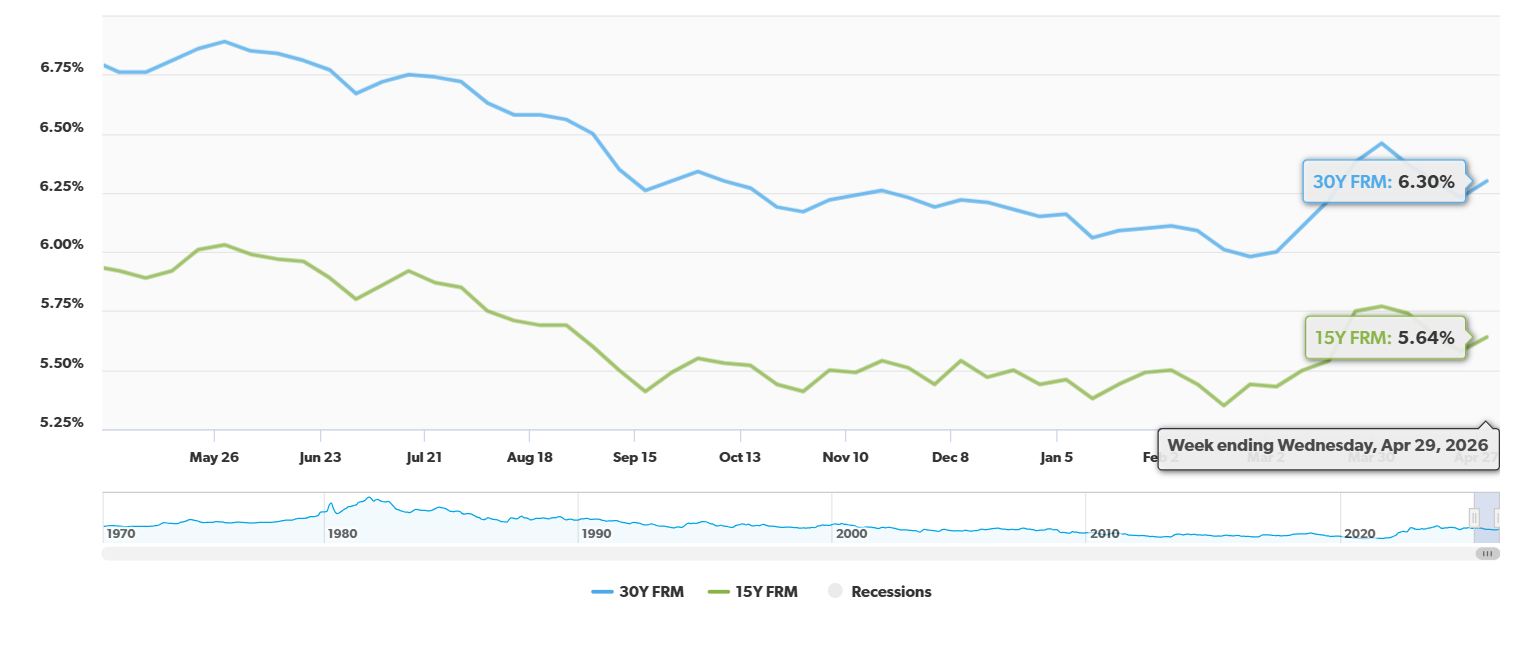

Let's dive into what's happening with mortgage rates today, according to data from Zillow, a source I've come to rely on for tracking these kinds of shifts.

- The 30-year fixed refinance rate is now at 6.59%. This is a slight tick up from yesterday's 6.56%, a change of 3 basis points.

- On the flip side, the 15-year fixed refinance rate is showing some love to borrowers, dropping by 4 basis points to 5.60%. This shorter-term option is becoming more attractive.

- Perhaps the most dramatic shift is in the 5-year Adjustable-Rate Mortgage (ARM) refinance rate, which has seen a significant drop of 138 basis points, settling at 5.88%, down from yesterday's 7.26%. This suggests lenders are eager to move this type of product.

What's interesting is that the 30-year rate is holding steady week-over-week at 6.59%. While today's small increase might catch headlines, the bigger picture shows a surprising level of stability for this particular loan type over the past seven days.

What's Driving These Mortgage Rate Movements?

As someone who's been following the housing market for a while, I can tell you that mortgage rates don't just move on their own. They're influenced by a complex mix of economic factors. Right now, in May 2026, we're seeing a market that's definitely feeling the pressure of inflation concerns and, unfortunately, some geopolitical instability.

Think of it this way: when the economy is uncertain, investors get nervous. They often move their money to safer places, which can drive up the yields on government bonds. Mortgage rates tend to follow these bond yields. So, even though rates are a far cry from the sky-high peaks we saw back in late 2023, they are still quite a bit higher than the super-low rates we enjoyed during the pandemic years.

Despite the daily ups and downs, I'm seeing a strong underlying demand for refinancing. People are still looking to take advantage of their home equity, which has grown substantially over the last few years. However, these weekly fluctuations are causing some potential refinancers to pause and wait, which is understandable.

The Real Story: Equity and Economic Headwinds

Let's break down some of the key influences impacting refinance activity:

- A Dip in Application Activity: Zillow's data shows that refinance applications took a 5% dive just this past week. This is directly linked to rates hitting their highest point in about a month. It's a clear sign that even a small rate increase can make some homeowners think twice. However, it's crucial to remember that year-over-year, activity is still a robust 29% higher. People are still refinancing, just maybe a bit more cautiously.

- Homeowners Cashing In: A big driver for refinancing right now is the desire to tap into home equity. Many homeowners are opting for cash-out refinances. Why? To pay down high-interest credit card debt, tackle personal loans, or invest in much-needed home improvements. With property values holding strong in many areas, people are recognizing the power of the equity they've built.

- The Global Picture Matters: The ongoing tensions in the Middle East are having a ripple effect. Higher oil prices mean higher inflation fears, which, in turn, pushes bond yields up. This is a pretty direct cause-and-effect that translates into higher mortgage rates. It’s a stark reminder that our local housing market is connected to global events.

Are You Considering a Refinance? Here's What You Need to Know

If you're thinking about refinancing, it's not just about looking at today's rate. You need to have a solid strategy.

- The “1% Rule” is a Good Starting Point: A common guideline is that refinancing makes sense if you can lower your interest rate by about 1% to 2%. This usually ensures that the savings over time will outweigh the closing costs you'll have to pay.

- Don't Forget Closing Costs: These fees can add up. Expect to pay anywhere from 2% to 6% of the total loan amount. For a $300,000 loan, that could mean $6,000 to $18,000 out of pocket. It's essential to factor this into your savings calculations.

- Equity is Key for Cash-Outs: If you're looking to pull cash out of your home, most lenders will want you to keep at least 20% equity in your property after the refinance is complete. This protects both you and the lender.

- Your Credit Score is Your Best Friend (or Foe): The absolute best rates, the ones that might even dip into the mid-5% range for a 15-year term, are usually reserved for borrowers with excellent credit scores, typically 740 or higher. If your score is lower, you might not qualify for the lowest advertised rates.

- A Glimpse into the Future: Major financial institutions like Wells Fargo are predicting that mortgage rates will likely stay in the low-6% range for the rest of 2026. This “higher for longer” outlook suggests that locking in a rate now, if it's a good deal for you, might be a wise move.

The Bottom Line on May 10, 2026

So, as of May 10, 2026, the 30-year fixed refinance rate has moved up to 6.59%. While this week saw a slight cooling in refinance applications due to this rate increase, the overall year-over-year trend shows strong interest as homeowners tap into their equity. My advice? Always weigh the potential savings against those closing costs, understand your credit score's impact, and keep an eye on the Federal Reserve's efforts to manage inflation. Making an informed decision is more important than ever in this dynamic market.

VS

Georgia’s affordable rental with higher cap rate vs Florida’s A‑rated property with stability. Which fits YOUR investment strategy?

We have much more inventory available than what you see on our website – Let us know about your requirement.

📈 Choose Your Winner & Contact Us Today!

Speak to a Norada Investment Counselor (No Obligation):

(800) 611-3060

Mortgage rates remain high in 2026, but rental properties continue to deliver strong cash flow and appreciation. Savvy investors know that turnkey real estate is the path to passive income and long‑term wealth.

Norada Real Estate helps you secure turnkey rental properties designed for immediate cash flow and appreciation—so you can invest smartly regardless of interest rate trends.

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?