As we move through 2026 and look ahead to 2027, the question on many minds is: where are mortgage rates headed? For those dreaming of homeownership or considering a refinance, understanding the trajectory of mortgage rates is absolutely key. Based on current trends and expert forecasts, I anticipate that average 30-year fixed mortgage rates will likely remain in the low to mid-6% range over the next two years, with potential for modest dips rather than dramatic drops. This stability, while not the record lows of a few years ago, offers a more predictable environment for planning.

Mortgage Rate Predictions for Next 2 Years: 2026 to 2027

Now, as of late May 2026, the average 30-year fixed mortgage rate is sitting comfortably in the mid-6% range, around 6.5%. This isn't a sudden shock; rates have been dancing in the high 6% range for a while now, influenced by a mix of persistent inflation, global uncertainties, and the Federal Reserve's careful approach to monetary policy.

A Quick Look Back: How Did We Get Here?

To understand where we're going, it helps to remember where we've been. Mortgage rates have been on quite a rollercoaster in recent decades. After hitting rock-bottom lows near 3% during the pandemic in 2020 and 2021, fueled by massive stimulus and super-easy money policies, rates took a sharp upward turn in 2022 and 2023.

The Federal Reserve aggressively raised its benchmark rates to fight inflation, pushing 30-year fixed rates above 7% and even 8% at times. While they've pulled back a bit since their peak, they're still significantly higher than the roughly 4% average we saw throughout the 2010s.

This creates what experts call the “lock-in effect.” Millions of homeowners who secured mortgages at rates below 4% are understandably hesitant to sell and move, as doing so would mean taking on a new loan at a much higher rate. This has kept the supply of homes on the market quite low, which in turn has helped prop up home prices even as borrowing costs remain elevated.

What's Really Moving the Needle on Mortgage Rates?

It’s important to remember that the 30-year fixed mortgage rate isn't directly set by the Federal Reserve, unlike their federal funds rate. Instead, it's primarily driven by the market, closely following the yield on the 10-year U.S. Treasury note.

To that yield, lenders add a “spread” to cover their risk, account for how likely borrowers are to pay off their mortgages early, and factor in the demand for mortgage-backed securities. This spread is currently hovering around 2 percentage points.

Looking ahead to 2026 and 2027, several key factors will continue to influence these rates:

- Federal Reserve Policy: The Fed's benchmark interest rate is currently in the 3.5–3.75% range as of May 2026. Their projections suggest only modest rate cuts are likely in the near future, perhaps one or two reductions of 0.25% each. This cautious approach is largely due to inflation that’s proving stubborn. We might see rates stabilize or even edge slightly higher again by 2027 if inflation doesn't cool down sufficiently.

- Inflation and the Economy: Both overall inflation and “core” inflation (which excludes volatile food and energy prices) are still above the Fed's target of 2%. Factors like energy costs, lingering supply chain issues, and government spending all play a role. If the economy continues to show strength, with robust job growth and solid GDP figures, it could put upward pressure on interest rates.

- 10-Year Treasury Yields: These yields are currently around 4.5%. Forecasts suggest they might tick up slightly or stay relatively flat, perhaps in the 4.2–4.7% range through 2027. This is partly due to the significant amount of Treasury debt the government is issuing and ongoing budget deficits.

- Global and Fiscal Risks: Unforeseen geopolitical events, potential trade disputes, and the ever-increasing U.S. national debt can all add to the pressure pushing Treasury yields higher.

- Housing Supply and Demand: The ongoing shortage of homes for sale, coupled with resilient home prices (which are expected to see modest growth or flat performance), will continue to influence how lenders price their loans and the appeal of mortgage-backed securities.

What the Experts Are Saying: Predictions for 2026–2027

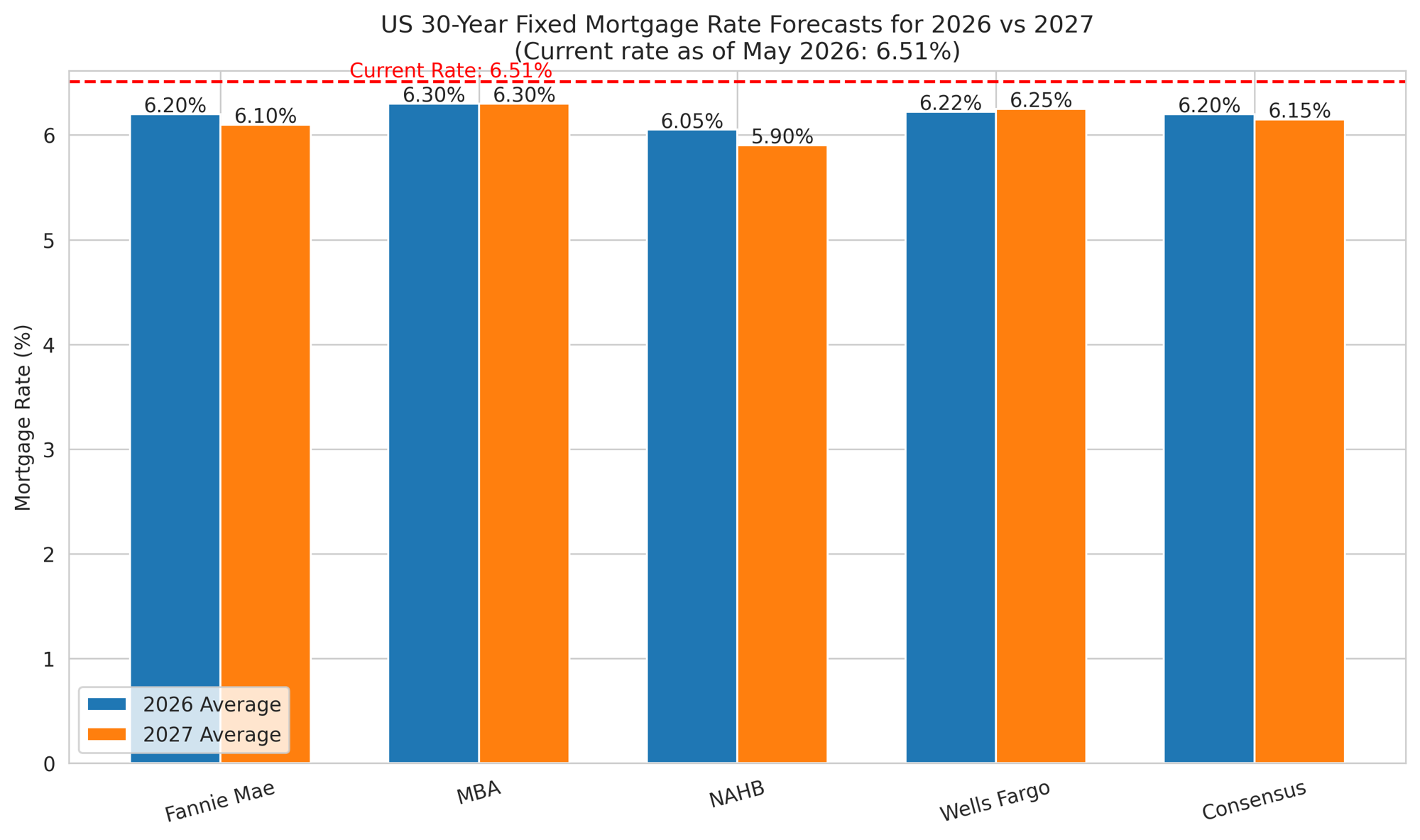

When I look at the major forecasting institutions – like Fannie Mae, the Mortgage Bankers Association (MBA), and the National Association of Home Builders (NAHB) – there’s a general consensus: don't expect mortgage rates to plunge back below 6% anytime soon in most likely scenarios. Instead, the prevailing outlook points towards rates stabilizing in the low to mid-6% range. A slight easing might occur if inflation cooperates and the Fed decides to cut rates further.

Here’s a snapshot of what some prominent organizations are projecting for average annual mortgage rates:

| Source | 2026 Average Projection | 2027 Average Projection | Key Assumptions/Notes |

|---|---|---|---|

| Fannie Mae | ~6.2% | ~6.1% | Gradual decline if inflation cools; potential dip below 6% late 2026. |

| Mortgage Bankers Association (MBA) | ~6.3–6.4% | ~6.3% | Stable rates, conservative outlook due to inflation. |

| National Association of Home Builders (NAHB) | ~6.17% | ~6.01% | Optimistic view, expecting housing supply to aid affordability. |

| Wells Fargo | ~6.2% | ~6.2% | Balanced view, factoring in economic and fiscal risks. |

| Consensus Median | ~6.2% | ~6.1% | Rates expected in the low-to-mid 6% range; minimal volatility. |

These projections, whether from Fannie Mae or the MBA, generally show a picture of rates remaining relatively steady or declining only slightly. Some quarterly forecasts do hint at potential dips later in 2026 if the Fed follows through with expected interest rate adjustments.

Considering Different Scenarios

While the “base case” of rates staying in the 6.0–6.4% range seems most probable, it’s always wise to consider other possibilities:

- Base Case (Most Likely): As mentioned, rates hover in the low to mid-6% range. Modest rate cuts from the Fed, combined with cooling inflation, could lead to a slight easing by late 2026 or early 2027. This should translate into a gradual pickup in home sales as affordability improves just a bit, with home prices seeing modest growth of 1–3% annually.

- Optimistic Scenario: If inflation surprises us by falling much faster towards the 2% target, the Fed might feel comfortable making more significant rate cuts. In this scenario, we could see rates dip into the high 5% range by mid-2027. This would likely reignite refinancing activity and give buyer demand a significant boost.

- Pessimistic Scenario: On the flip side, if inflation flares up again (perhaps due to energy shocks or new tariffs) or if the economy remains unexpectedly strong, the Fed might delay or halt rate cuts. This could push rates back towards the 6.5–7% mark. Such a scenario would continue to limit housing inventory and sales, while the scarcity of homes could keep prices supported.

What This Means for You and the Housing Market

Let's talk practical terms. A mortgage rate of 6.5% on a $400,000 loan means a principal and interest payment of roughly $2,528 per month. Compare that to a rate of 3% from a few years ago, where the same loan would cost around $1,690 per month – that's a difference of over $800! This affordability challenge continues to be a major hurdle for first-time homebuyers. However, for those who can manage it or have existing home equity, it's still possible to navigate the market. If rates do dip below 6%, opportunities for homeowners with higher-rate loans to refinance could certainly emerge.

Looking at the broader housing market, predictions suggest:

- Home Sales: The MBA forecasts a modest increase in single-family home loan originations, reaching about $2.2 trillion in 2026. Existing home sales are expected to climb by 6–7% as more inventory slowly becomes available.

- Home Prices: Nationally, prices are anticipated to remain stable or see slight increases, though regional differences will undoubtedly persist.

- Foreclosures: While higher costs for homeownership (like insurance and property taxes) have led to a slight uptick in foreclosure filings, most homeowners still have significant equity, which is preventing widespread distress.

The Road Ahead

The era of ultra-low mortgage rates seen in 2020–2021 is very likely behind us for the foreseeable future. The consensus from experts points to a more stable environment in the coming two years, with rates likely settling in the low to mid-6% range. This isn't a period of dramatic change, but rather one of gradual adjustment. It will continue to favor well-prepared buyers and support a steady, albeit not booming, housing market.

The precise path mortgage rates take will ultimately depend on how inflation evolves, the Federal Reserve's actions, and global economic developments. Staying informed with regular updates from sources like Freddie Mac and monitoring economic data releases will be crucial. Whether you're a first-time buyer, looking to refinance, or simply planning your financial future, the next two years offer opportunities within a landscape of measured expectations.

Invest Smartly in Turnkey Rental Properties

Savvy investors are locking in financing to maximize cash flow and long-term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income for life.

🔥 HOT NEW investment LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rate Predictions for the Next 5 Years: 2026 to 2030

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?