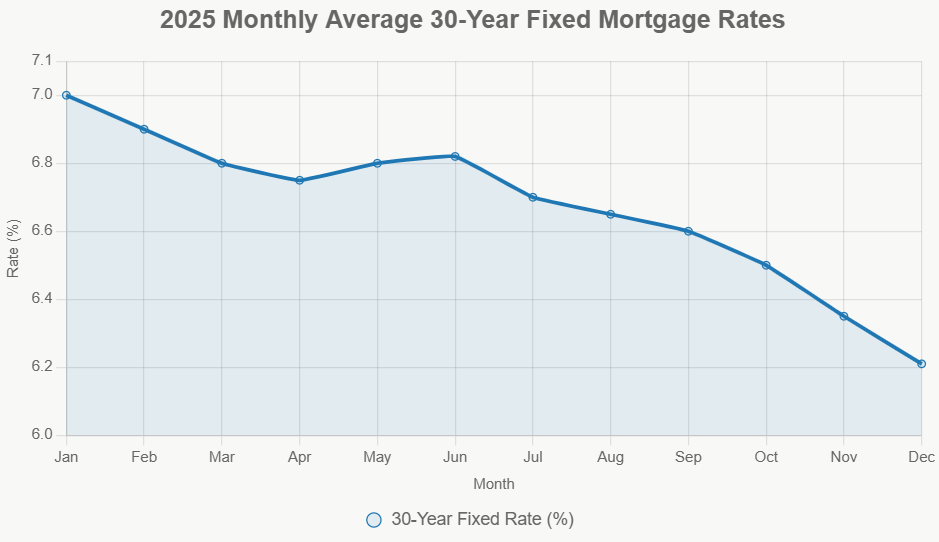

As 2025 draws to a close, if you're looking to buy a home or refinance your current mortgage, you'll find today's mortgage rates hover just a hair above 6%. This steady interest is a key point to grasp if you're navigating the housing market right now. According to Zillow's latest data for December 27th, the benchmark 30-year fixed mortgage rate is sitting at 6.01%, with the 15-year fixed rate at 5.47%. For us everyday folks trying to figure out our finances, this means borrowing costs have found a relatively stable rhythm, which can actually be a good thing for planning purposes.

Today’s Mortgage Rates, Dec 27: 30-Year Fixed Edges Past 6%, Refinance Rates Hold Steady

Where Do Today's Mortgage Rates Stand?

Let's break down the national averages as of December 27th, 2025, courtesy of Zillow:

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.01% |

| 20-year fixed | 5.93% |

| 15-year fixed | 5.47% |

| 5/1 ARM | 6.11% |

| 7/1 ARM | 6.34% |

| 30-year VA | 5.59% |

| 15-year VA | 5.19% |

| 5/1 VA | 5.24% |

Just a quick note: these are national averages and might be rounded slightly. Your actual rate will depend on many personal factors.

And What About Refinancing Today?

If you're a homeowner who's been eyeing a refinance, here’s how the numbers are looking for that side of the market:

| Loan Type | Average Rate |

|---|---|

| 30-year fixed | 6.09% |

| 20-year fixed | 5.80% |

| 15-year fixed | 5.60% |

| 5/1 ARM | 6.35% |

| 7/1 ARM | 6.77% |

| 30-year VA | 5.54% |

| 15-year VA | 5.35% |

| 5/1 VA | 5.39% |

What Does This Mean for You? A Deeper Dive.

Looking at these numbers, my professional opinion is that we're in a period of cautious optimism. Rates are stable near the holidays, which is a consistent trend. You might see slight daily fluctuations, but the broader picture is one of predictability.

On the flip side, we have to acknowledge the underlying economic forces. If we see strong economic news – things like higher-than-expected GDP growth, as Zillow points out – it can put upward pressure on mortgage rates. This happens because investors might see better returns in other areas, like the stock market, and move their money out of bonds, which mortgages are often tied to. It’s a delicate dance between economic strength and borrowing costs.

So, for homebuyers, these rates hovering just above 6% mean affordability is still a challenge, especially in many pricier markets. However, that stability I mentioned? It's a real benefit. You can sit down with your budget and have a much clearer idea of what your monthly payments will look like, month after month, for the life of the loan. This predictability is invaluable when making such a significant financial commitment.

For homeowners looking to refinance, there are certainly opportunities, especially if your current mortgage has a significantly higher rate from a few years back. However, don't expect the dramatic savings of the past. The savings might be more modest now, but for some, it could still mean lowering monthly payments or shortening the loan term.

And then there are the adjustable-rate mortgages (ARMs). Right now, they're generally coming in slightly higher than their fixed-rate counterparts. This usually makes them less attractive unless you have a very specific plan to move or sell the home before the initial fixed period ends. From my experience, most people find the peace of mind of a fixed rate outweighs the potential initial savings of an ARM.

Becoming a Savvy Borrower: Strategies to Lock In a Better Rate

Even in a market like this, your effort can make a real difference. Don't just take the first rate you're offered. Here are some strategies I consistently advise people on:

- Shop Around: This is non-negotiable. Rates can vary significantly between lenders. I always tell people to compare offers from at least three, and ideally more, different lending institutions. You might be surprised by the difference.

- Boost Your Credit Score: A higher credit score directly translates to a lower interest rate. If you have a few months before you plan to apply, focus on paying down credit card balances and ensuring all your bills are paid on time.

- Consider Shorter Loan Terms: As you’ll see in the comparison below, a 15-year mortgage comes with a lower interest rate than a 30-year one. If your budget can handle it, this can lead to massive savings over time.

- Explore VA Loans if Eligible: For those who have served our country, VA loans often come with very competitive rates, even lower than many conventional 30-year fixed options. It's a benefit you've earned, so definitely look into it.

- Time Your Application Wisely: While rates are stable, there can still be minor shifts during the day or week. Discuss with your lender about the best time to lock in your rate.

The Big Decision: 15-Year vs. 30-Year Fixed Mortgage

This is a classic dilemma, and it really comes down to your financial personality and goals.

The 30-Year Fixed Mortgage: This is the workhorse for most borrowers, and for good reason.

- Pros: Lower monthly payments, which frees up cash flow for other investments, emergencies, or simply daily living expenses. It offers more flexibility if your income is less predictable or if you want to have more breathing room in your budget.

- Cons: You'll pay significantly more in interest over the life of the loan. It takes longer to build equity.

The 15-Year Fixed Mortgage: This option is fantastic for those who can manage the higher payments.

- Pros: Much lower interest rates, meaning you’ll save a considerable amount of money (potentially hundreds of thousands of dollars) on interest over the loan's term. You'll build equity much faster and be debt-free sooner.

- Cons: Higher monthly payments that can strain a tighter budget. Less flexibility if unexpected financial setbacks occur.

My Favorite Approach: The “Hybrid” Strategy

Here’s a tip from my own playbook: many homeowners I know have found success with what I call the “hybrid” strategy. You take out the 30-year fixed mortgage for its built-in flexibility and lower mandatory payment. Then, if your finances allow, you voluntarily make extra principal payments. This way, you get the best of both worlds: you have the security of the lower payment if you need it, but you can pay off your home much faster, effectively acting like you have a 15-year mortgage. It’s a smart way to control your destiny without locking yourself into an unmanageable payment.

Key Takeaway for Today

In summary, mortgage and refinance rates are holding steady, just above 6%. While we're not seeing the bargain-basement rates of the past, this period of stability offers predictability, which is a valuable asset for anyone looking to buy or refinance. My advice remains unchanged: do your homework, compare lenders diligently, and choose the loan option that best aligns with your personal financial situation and long-term goals.

VS

Two solid options: Alabama’s affordable new build with steady returns vs Tennessee’s larger home with higher cash flow. Which fits YOUR investment strategy?

📈 Choose Your Winner & Contact Us Today!

Talk to a Norada investment counselor (No Obligation):

(800) 611-3060

Invest in Fully Managed Rentals for Smarter Wealth Building

With mortgage rates dipping to their lowest levels in months, savvy investors are seizing the opportunity to lock in financing.

By securing favorable terms now, you can also maximize immediate cash flow while positioning yourself for stronger long‑term returns.

Norada Real Estate helps you seize this rare opportunity with turnkey rental properties in strong markets—so you can build passive income while borrowing costs remain historically low.

🔥 HOT NEW LISTINGS JUST ADDED! 🔥

Talk to a Norada investment counselor today (No Obligation):

(800) 611-3060

Also Read:

- Mortgage Rates Predictions Backed by 7 Leading Experts: 2025–2026

- Mortgage Rate Predictions for the Next 3 Years: 2026, 2027, 2028

- 30-Year Fixed Mortgage Rate Forecast for the Next 5 Years

- 15-Year Fixed Mortgage Rate Predictions for Next 5 Years: 2025-2029

- Will Mortgage Rates Ever Be 3% Again in the Future?

- Mortgage Rates Predictions for Next 2 Years

- Mortgage Rate Predictions for Next 5 Years

- Mortgage Rate Predictions: Why 2% and 3% Rates are Out of Reach

- How Lower Mortgage Rates Can Save You Thousands?

- How to Get a Low Mortgage Interest Rate?

- Will Mortgage Rates Ever Be 4% Again?